UK at risk of falling behind on climate goals after Autumn Statement

- 23 November 2022

- Energy Sustainability United Kingdom

In an era of looming public spending restraint, the UK risks lagging behind in key areas of its net-zero strategy. We look at what the recent Autumn Statement means for the electric vehicle transition, energy efficiency and investment in green electricity

UK budget leaves net-zero plans at risk of slipping behind

There was plenty to chew on in last week's UK Budget, not least that much of the anticipated fiscal pain has been pushed back until after the next election. Chancellor Jeremy Hunt had calculated that calmer financial markets and the announcement of certain tax rises means he can push back some tough spending decisions.

But the Budget also raised interesting questions about the UK’s transition to net zero and sustainability. Climate change received several mentions in the Chancellor’s statement, which came against the backdrop of the COP27 conference.

However, in an era of ever-increasing spending restraint, the UK risks lagging behind in several areas of its net-zero strategy, outlined last year. The government’s independent net-zero advisor, the Climate Change Committee (CCC), found earlier this year that the majority of the government’s carbon reductions carry at least some risks – and in many cases they are significant. Here, we delve into three areas where the Autumn Statement was relevant to Britain's net-zero ambitions.

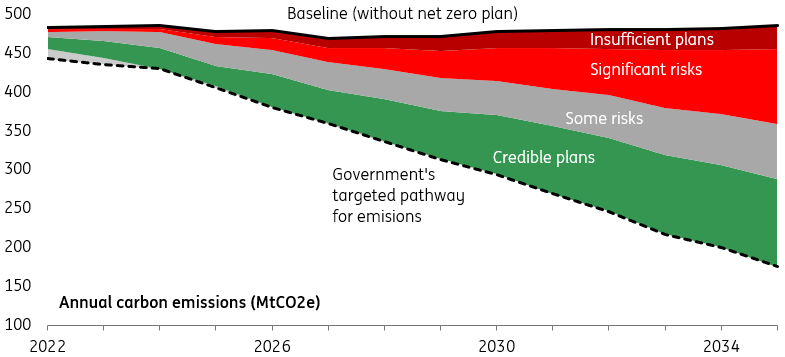

How the Climate Change Committee grades the UK's progress on its net-zero strategy

Buildings and manufacturing/construction are areas where plans are most lacking

Electricity generation

- The existing energy profits levy (windfall tax) covering oil and gas companies will increase from 25% to 35% and is being extended by three years to 2028. It will be expanded to cover renewables generators, who will see a 45% tax on profits when wholesale electricity prices are above £75/MWh.

- Household energy support will be made less generous, with the average household set to pay £3,000 a year from April. That's slightly below what's implied by current market prices over a 12 mo12-monthzon. Previously, the average household – not on means-tested benefits – was set to pay £2,500 a year until the third quarter of 2024, with a £400 discount between October and April.

- The government reaffirmed its commitment to nuclear and reiterated plans to go ahead with the Sizewell C project.

Since the summer, we've argued that a broader windfall tax, especially one covering renewables, looked inevitable. Amid concerns about public finances, this measure had the rare attribute of both being politically popular and a decent revenue generator. The latter is less true now given the recent collapse in gas prices. But remember the UK has – in effect – an open-ended liability to gas prices via its household/business energy cap. These latest tax measures, to some extent, provide a natural hedge against future spikes in prices (our house view is that European gas prices could end up higher next winter than in the current one).

But how will this affect the UK's transition to greener energy? Our team wrote in detail about some of the risks associated with a similar scheme mooted by the EU earlier this year.

The UK has been a relative success story in recent years, in that emissions associated with electricity generation have already fallen by half of what is needed by 2050 to be consistent with net zero, according to the CCC. Offshore wind is still favoured over onshore by the government, and most development is now achieved via Contract for Difference (CFD) auctions. These set a pre-agreed "strike" price for future energy produced and consequently mean producers are obliged to return excess revenues when wholesale prices are higher. As you'd expect, the new tax won't apply to electricity producers with CFD agreements.

Given that this is now the primary means of allocating new wind investment, the new tax decisions should have a less obvious adverse effect on the ability to attract new capital.

Transport

For the first time, fully electric vehicles (EVs) will be subject to Vehicle Excise Duty (VED) from 2025. Existing EV road users will pay the standard rate, currently £165 a year. Battery-electric vehicles (BEV) are currently exempt, and plugin-hybrids (PHEV) pay a lower rate.

Away from energy support, the landmark decision to begin taxing electric vehicles was perhaps the most interesting sustainability-linked decision taken in the Autumn Statement.

The incentive for change is obvious. Fuel duty makes up roughly 3% of government receipts (or £30bn annually), and that proportion will gradually fall as the prevalence of EVs increases. Still, that makes the UK among the first in Europe to start tackling the issue of how EVs should be taxed. And it shines a spotlight on whether the government needs to do more to keep the pace of EV adoption on track.

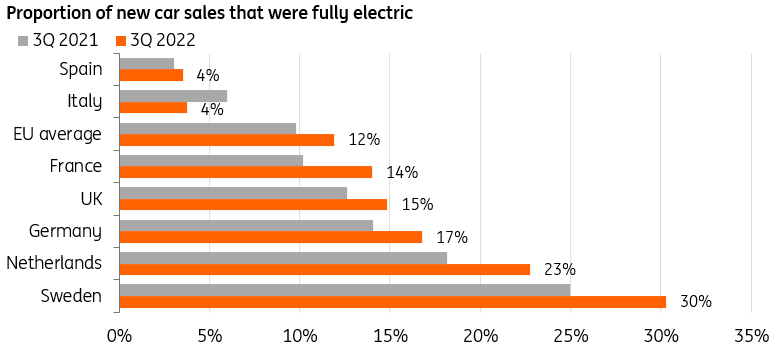

There’s no doubt that government intervention here is less essential than it once was. The proportion of battery EVs relative to overall sales has continually increased and made up 15% of new car purchases in the third quarter. The result is that "surface transport" now looks like one of the easier areas of transition for the UK – the technology is well developed, unlike some other net-zero areas, and consumer appetite appears strong.

Fully electric cars made up 15% of total sales in the third quarter

That said, battery EVs only make up around 1% of the total fleet, and the government’s ambition to end petrol/diesel car sales by 2030 is premised on the assumption that EV costs will continue to tumble. Rising input costs and ongoing supply issues – particularly for batteries/battery metals – are a clear challenge to that logic. So too are higher electricity prices, which have reduced the operational savings versus conventional vehicles (albeit that's partly offset by improvements in mileage).

There’s also a mounting risk that existing demand for EVs will outpace the growth of charging infrastructure. While growth in public chargers is averaging 8% a quarter, more will need to be done for dense residential areas. Half of UK properties are either flats or terraced houses, making it harder for households to charge vehicles without some form of public infrastructure. Public funding here is currently fairly limited.

So should the government be doing more, not less, to incentivise EV adoption? It’s debatable whether the introduction of vehicle duty for EVs materially shifts the incentives to buy. But UK consumers, unlike those in France and Germany, are largely no longer eligible for government EV grant payments. The UK has also opted against German-style support for lowering the cost of public transport in recent months, making car travel less desirable.

The lesson here is that the government’s announcement on EV duty is probably only the first step. Ultimately there’s going to be pressure to increase the tax burden for emissions-generating vehicles, but that’ll be challenging without disproportionately affecting lower-income households. Vehicle taxation may inevitably need to be coupled with a form of road pricing to counter the expected increase in congestion, as well as larger incentives for consumers to switch to public transport.

Buildings

An additional £6bn of funding from 2025 for energy efficiency projects, in addition to £6.6bn in the current parliamentary period. Introducing new 'Energy Efficiency Taskforce' to aid delivery.

This is arguably the area where government intervention is most lacking. Our previous analysis suggests that reducing UK emissions from buildings will require greater public investment by 2025 than transport or electricity generation, where private funds are set to play a larger role. The CCC found earlier this year that ministers’ plans in this area were overwhelmingly insufficient or carry significant risk.

This is undoubtedly a challenging area. The UK’s housing stock is ageing, with more than a third of properties built before 1945, the highest proportion in Europe. Britain also stands out for its reliance on gas as a source of domestic heating. Less than half of homes are rated EPC C or higher (the level generally seen as the minimum acceptable energy efficiency).

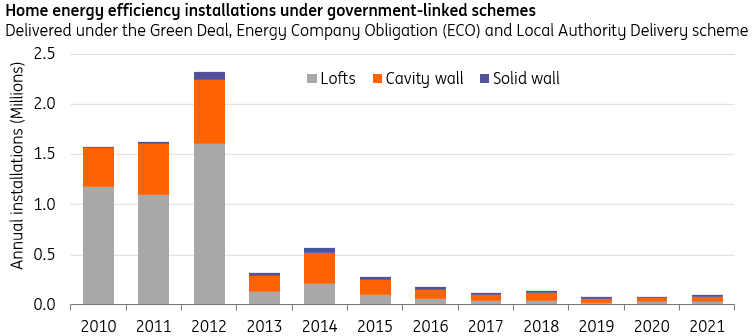

Even so, in some key respects, the UK has gone backwards. Unlike other major European economies, Britain closed its flagship energy efficiency grant scheme and hasn’t yet introduced a replacement. The result was that by 2021, the number of annual home insulation installations delivered under government-linked schemes had fallen by 90% from a peak of more than two million in 2012. While that doesn’t capture renovations outside of official schemes, there’s been little discernible improvement in building energy efficiency ratings over the past decade, suggesting privately-funded measures haven’t adequately filled the gap.

In areas where recent government funding has been available, uptake has been fairly steady. The government introduced a £5,000 grant for heat pump installations earlier this year, but so far has only been redeemed 3200 times (roughly 0.2% of total gas boilers sold in 2019).

UK has gone backwards on publicly-sponsored home insulation installs

Without additional funding commitments, achieving the targeted 15% reduction in buildings/industrial emissions by 2030 will be a challenge. There will also be pressure for ministers to look at other means of incentivising private investment by households. Government-guaranteed loans/mortgages for renovations, with reduced interest rates, is one possible option.

Beyond financing, the other major obstacle to achieving these targets lies in worker shortages. While data is hard to come by, the CCC estimates that 200,000 extra hires will be needed by the mid-2020s to achieve the necessary pace of building improvements. But staff shortages are a key restraint on UK economic activity, and have been exacerbated by poor health and lower inward EU migration. With the exception of additional funding for the health service/education over the next couple of years, there was little in the Autumn Budget that is likely to materially change (an admittedly complex) issue.

Alongside buildings, manufacturing/construction stand-outs as another area where progress was judged to be limited by the CCC. This received little attention in the Autumn Statement, but the government has been making some progress on establishing initial Carbon Capture and Storage "clusters". Our team wrote more on this topic earlier this year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more