- Quick take

- Yesterday, 11:50

- Hungary

Hungarian inflation hits 10-year low

July saw record-low inflation as we expected. The strength of the forint and favourable food price developments pulled inflation lower. This makes a rate cut in August a done deal, and an extension to the cutting cycle looks highly likely

| 1.2% |

Headline inflation (YoY)ING estimate 1.2% / Previous 1.7% |

Inflation hits rock bottom just as we expected

Consumer prices fell slightly in July compared with the previous month, according to the latest data from the Hungarian Central Statistical Office (HCSO). Annual inflation eased further to 1.2%, its lowest level since late 2016.

This was a major surprise compared to market expectations, as price pressure fell well below consensus forecasts. However, the figure exactly matched our forecast, which had been the most optimistic projection in the market.

The extent of the surprise is highlighted by the fact that inflation fell below the uncertainty range projected in the National Bank of Hungary’s June Inflation Report for July. As a result, despite the energy price shock and drought conditions, inflation has not only avoided accelerating but has also slowed for three consecutive months.

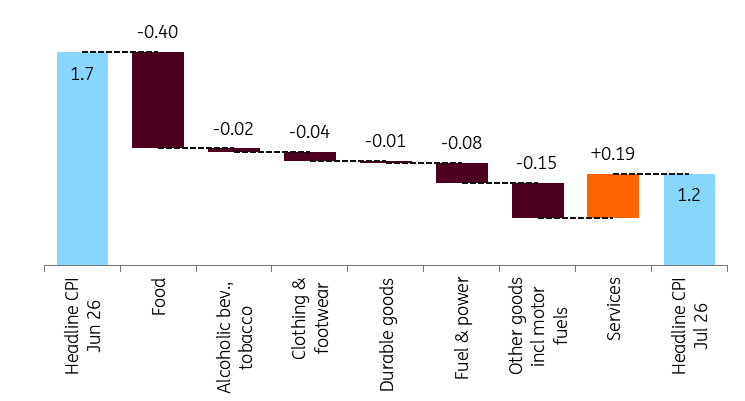

Main drivers of the change in headline CPI (%)

The details

- The negative monthly headline inflation rate is mainly due to a 1% monthly fall in food prices. This may be partly due to the strengthening of the forint, and partly due to broader international disinflationary trends.

- This time, the price of household energy fell by almost 1% compared to last month, due to the warmer weather at the end of spring. For methodological reasons, the Statistical Office uses a delayed dataset.

- As a significant price drop in fuels was observed immediately after the end of price controls, followed by an increase from mid-month onwards, the average price level for the data collection period was lower, hence fuel prices dragged down the inflation rate as well.

- In the case of services, the 1.6% monthly price increase can be considered strikingly high, though this was partly attributable to known factors. Airfares rose by more than 4% MoM. The impact of the previously announced price increases for telephone, internet, and TV subscriptions was reflected, too. Unsurprisingly, the substantial rise in the cost of holiday services also continued, with a monthly increase of nearly 8%.

The composition of headline inflation (ppt)

Core inflation moves favorably

Annual service inflation jumped to 4.7%, the second-highest figure in this category so far this year behind January. Therefore, service inflation remains the main contributor to overall price pressure. The main driver of this is the double-digit nominal wage growth on top of the release of price shield measures.

The core inflation rate, which is adjusted for price changes in volatile items such as energy and fuel, stands at 1.9% year-on-year in July. This is higher than the headline figure, mainly due to high service inflation. However, favourable local and global effects are keeping core inflation in check, with no evidence of second-round effects yet from the global energy price shock. The only reason we can’t say that the July inflation map was a complete rosy surprise is because of sticky price inflation, which increased in July for the first time since autumn 2025.

Headline and underlying inflation measures (% YoY)

The door opens for more rate cuts

Looking ahead to the coming months, service inflation is likely to remain high due to seasonal factors and previously announced price rises. The strength of the forint is expected to continue to limit imported inflation, thereby controlling price changes for durable goods and food and probably fuel. However, the potential price-increasing effects of the drought and the current energy crisis may become apparent in 2027.

According to our latest flash estimate, inflation may remain below 3% until the end of the year. We are projecting an average inflation rate of just 1.9% for 2026. The average rate of price increases is expected to be around 3.0% in 2027. July’s inflation data and our latest forecast suggest that the rate cut in August will be merely a formality. Unless we see another wave of global energy price shocks, the rate-cutting cycle will almost certainly continue through autumn. We expect the base rate to reach 4.75% by the end of the year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more