UK Chancellor delays budget pain amid more stable market backdrop

- 17 November 2022

- United Kingdom

Markets have calmed in recent weeks which has allowed the Chancellor to push back some of the fiscal pain, particularly on public spending. The result is elevated borrowing in the near term, but the impact on UK growth isn't necessarily huge. Still, with energy support becoming less generous, the Bank of England can afford to hike more gradually

Has the government done enough to calm markets?

This is a much less pertinent question than it was a few weeks ago. The change in political management, relentless leaks of possible austerity measures, and an end to the liability-driven investment (LDI) pension crisis have all contributed to calmer markets and a narrower risk premium in UK assets. Investors have also bet that a tighter budget will lessen pressure on the Bank of England to increase rates. That is perhaps an exaggeration, but the combination of these factors helped 10-year government bond yields fall from 4.5% to 3.25% in the run-up to today's Budget.

But this logic was still contingent on Chancellor Jeremy Hunt presenting a plan which saw debt stabilise as a percentage of GDP in the medium-term – and the Office for Budget Responsibility has confirmed this will be the case by the fiscal year 2027/28.

But the story is a little more complex than that, and the reality is the Chancellor faced a trade-off between boosting credibility by presenting immediate plans to reduce borrowing and avoiding amplifying the forthcoming recession. If anything, the Chancellor is leaning more towards the second of those priorities, in that much of the pain – particularly in terms of tighter government spending – won’t kick in for a couple of years. Public sector net investment rises to 3% of GDP next year but then falls back to 2.2% in five years’ time.

The result is that borrowing is still elevated over the next couple of years, to the extent that gilt issuance plans have actually increased for the next fiscal year. Taking the Debt Management Office’s forecast 2023-24 remit of £305bn, and the BoE’s quantitative tightening programme, we estimate that private investors will be required to increase their gilt exposure by at least £268bn in FY2023-24. The previous peak was £107bn in FY2020-21. Gilt markets may be calmer, but there’s still plenty of supply for private investors to absorb – and a lot rests on delayed pain coming through in the public finances later this decade.

For now, though, sterling has taken the Autumn Statement in its stride, barely changing against the euro and slightly softening against today’s modest dollar recovery. The lack of reaction will be down to the well-flagged measures from the new government, although the currency market might once again be keeping one eye on the slight softness in the gilt market today. Our baseline view sees GBP/USD dipping below 1.15 after the current bout of position adjustment has run its course, while we also favour some modest underperformance against the euro. EUR/GBP could be trading back to 0.89 by year-end.

Energy support is becoming less generous

The impact on the economy and inflation

The fact that a fair chunk of the pain has been delayed means that the economic impact of the Autumn Statement on next year’s growth isn’t necessarily huge – or at least not compared to expectations. A lot of the near-term tax rises are also either concentrated on higher-income earners or energy companies – and remember that the national insurance cut implemented under former Prime Minister Liz Truss hasn't been reversed.

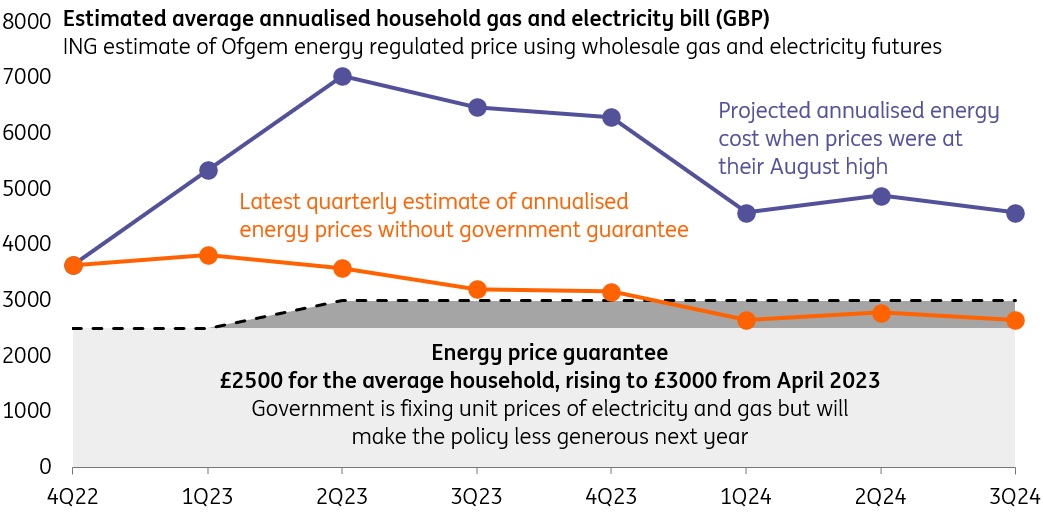

That said, the major change is that the average household will see energy bills fixed at £3,000 a year from April, up from £2,500 previously promised. That’s still slightly more generous than would otherwise be implied by wholesale gas/electricity futures, but not by much. We estimate that, without government intervention, the average energy bill would be £3,200 in FY2023, and that reflects the big fall in prices we’ve seen since August.

Interestingly, even though the Chancellor has committed to supporting households for another 12 months beyond April, we estimate that energy bills will actually fall below £3,000 on an annualised basis by the first quarter of 2024 if wholesale prices stay where they are. Admittedly that's a big "if", and the risk for the Treasury is that they increase once more, particularly for futures covering the winter of 2023/24, pushing up the cost of support – albeit this is somewhat mitigated by a widened windfall tax that will now cover renewable electricity generators.

For the economy, the important point is that households will be paying a little over 8% of disposable incomes for energy in FY2023, from 7% under the original guarantee, by our estimates. However, this is before considering new payments for low-income households, which will help cushion the blow.

We’re forecasting a recession with a cumulative hit to GDP of roughly 2% by the middle of next year, and expect overall 2023 GDP to fall by 1.2%. The decision on energy prices lifts our inflation forecasts by roughly one percentage point from April next year.

UK inflation will be roughly 1pp higher after April

The impact on the Bank of England

The reality is there’s not much in the Autumn Statement to cause any earthshattering changes to the Bank of England’s view that it unveiled at the November meeting. The BoE's forecasts, which envisaged recession with or without further rate hikes, were premised on some withdrawal of energy support. The assumptions it made at the time are not wildly different from what has been announced today.

As a result, we think the November 75bp rate hike will probably prove to be a one-off. Admittedly, some hawkish surprises in this week’s inflation data, and signs of ongoing worker shortages, suggest the Bank’s work isn’t finished yet. But we think the committee will pivot back to a 50bp hike in December and either 25bp or 50bp in February, seeing the Bank Rate peak around 4%.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more