CIS‑4 FX buoyed by inflows while CPI risks hit the rates outlook

- 15 May

- Armenia Azerbaijan

Higher commodities prices and strong portfolio inflows are lifting exporters’ external buffers and reinforcing currencies in the region. Meanwhile, mounting inflation pressures are leading to tighter monetary policy outlooks. However, that is unlikely to materially affect economic activity in the region

External buffers improve

The escalation in the Middle East, including persistent tensions and risks around the Strait of Hormuz, has reinforced a higher commodity-price backdrop (see here). Compared with our previous monthly note, the oil price outlook for FY26 has edged up by $4 to $93/bbl. Based on the macro sensitivities, Azerbaijan and Kazakhstan remain the main beneficiaries, while Uzbekistan and Armenia present a more balanced picture.

- In Azerbaijan, under the new oil scenario, the current account is heading towards a 9-10% GDP this year, while the consolidated budget surplus may reach 4% of GDP.

- Kazakhstan is also seeing stronger exports and fiscal revenues, helping to reduce its current account deficit to 2-3% of GDP and balance its consolidated budget.

- Uzbekistan faces higher import costs from rising oil prices, while gold exports, on hold since 4Q25, should restart later in the year and help contain the current account deficit at around 4% of GDP.

- Armenia, as a net energy importer, remains exposed to global price moves and remains in a twin-deficit pattern, but continues to benefit from remittances of 6%+ of GDP, supported by increased tourism amid regional tensions.

Strong portfolio inflows – the key positive surprise and a supportive factor to CIS-4 FX

Contrary to our initial concerns, global and regional risk appetite has remained resilient despite Middle East tensions. Country-specific developments suggest the CIS-4 is using the current environment to attract capital inflows.

- Kazakhstan is progressing towards Euroclear inclusion while preparing sovereign and quasi-sovereign debt issuance. The tenge's 7% appreciation vs. the USD since the outbreak of the Iran War (and the 18% strengthening since the end of 3Q25) reflects stronger capital inflows, as the effect of higher oil prices should be largely offset by dividend outflows and higher imports.

- Uzbekistan is advancing its privatisation programme, with UzNIF IPO and a broader pipeline aimed at foreign investors. We believe stronger capital inflows are currently the primary factor behind the soum's stability in recent months despite the halt in gold exports.

- Armenia is also seeing stronger portfolio inflows, reflecting ongoing normalisation with Azerbaijan and supporting FX resilience: the dram continued its strengthening trend, gaining 2% since late February despite a material spike in oil prices and the likely widening of the current account deficit to 8-9% of GDP this year.

Compared with the previous month, we have a more favourable near to medium-term outlook for CIS-4 floating currencies, while maintaining a cautious longer-term view until a proven track record in structural transformation is established. Higher reliance on portfolio flows could be a mixed blessing, as financial market investors, unlike corporate FDI partners, can be easily spooked.

Inflation risks confirmed, policy stance should tighten

The worsening CPI outlook is materialising in line with our expectations. Alongside imported inflation – through exposure to the EU, China, and other trade partners experiencing direct effects of higher commodity prices – domestic factors are amplifying pressures in most economies, with Azerbaijan an exception.

- Kazakhstan: fiscal and quasi-fiscal stimulus, together with possible utility tariff increases, complicate a return to single-digit CPI despite the recent slowdown to 10.6% year-on-year in April.

- Uzbekistan faces demand-driven pressures from stronger activity, with the recent slowdown in CPI to 7.1% YoY largely driven by base effects, as noted by the central bank.

- Armenia, already sensitive to external costs, has seen CPI rise to 5.3% YoY in April, well above its 3% target. Strong domestic demand (GDP growth of 7.1% YoY in 1Q26) is also highlighted as a risk by the Central Bank of Armenia, while we also see persistent fiscal deficits of around 3.5% of GDP as pro-inflationary.

- Azerbaijan (CPI 5.6% YoY as of March), while exposed to imported inflation risks reflected in the central bank's higher FY26-27 outlook, shows weaker domestic pressures given soft growth. GDP contracted by 0.3% YoY in 1Q26, with overall expected full-year growth in low single digits.

We therefore stand by an upward revision to the CPI trajectory for 2026-27, implying a less steep slowdown in Kazakhstan and Uzbekistan, stabilisation in Azerbaijan, and some acceleration in Armenia. The supply-side nature of these revisions does not require immediate rate hikes but reduces the scope for cuts versus previous expectations.

Meanwhile, despite the more moderate nature of the current global inflationary shock compared to 2022, the balance of risks to global inflation forecasts is still tilted upward, and the second-round effects could trigger more drastic monetary policy action, should our global base case scenario prove too optimistic.

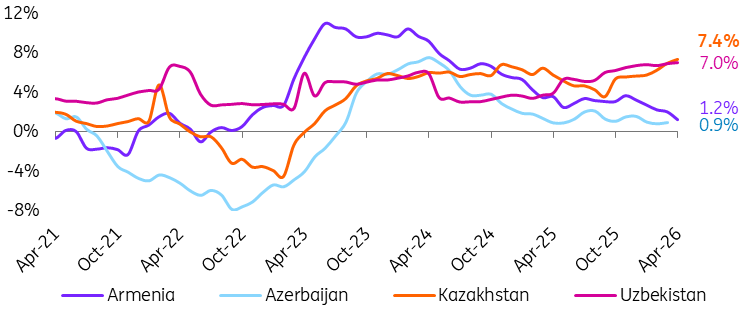

On the positive side, a tighter monetary stance should remain broadly neutral for activity, which remains robust in Kazakhstan, Uzbekistan, and Armenia, and less rate-sensitive in Azerbaijan. Cautious monetary policy should reinforce the CIS-4's competitiveness from the perspective of global investors, and nominal FX rate strength should serve as a disinflationary factor. The current real rate context (see the chart below) suggests that the balance of risks to our policy rate views is tilted upward for Armenia and Azerbaijan, and downward for Kazakhstan and Uzbekistan.

Real policy rates in CIS-4 (%), based on CPI over the past 12 months

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Two anniversaries, one uncomfortable mirror

- This bundle contains 13 Articles