Sitting, waiting, wishing… for energy flows to resume

- 15 May 2026

- Commodities, Food & Agri Energy

Energy markets remain extremely sensitive to developments in the Middle East, showing the significance of the supply disruptions we are witnessing. However, there have been several factors that have helped to take some pressure off prices

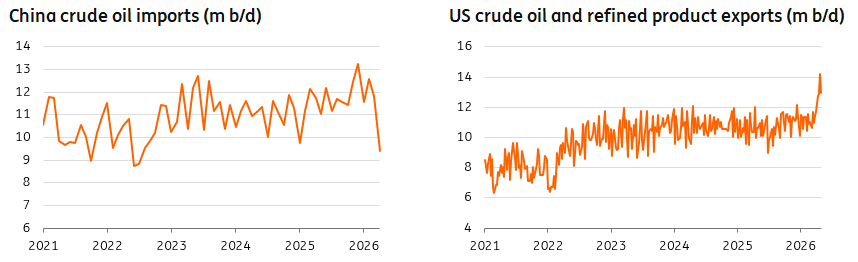

Falling Chinese imports and rising US exports offer relief to oil markets

It has been another volatile month in energy markets, with oil prices being whipsawed by Iran-related headlines. Cold water has been thrown over optimism for an imminent peace deal, after President Trump rejected Iran’s counterproposal peace plan. And as a result, any hopes for a quick resumption in energy flows through the Strait of Hormuz have also faded, which has seen Brent trade convincingly back above $100/bbl.

However, with the oil market facing a supply disruption of around 13m b/d, one may be surprised that we are not seeing much higher prices. There is an element of the market still clinging to some optimism that energy flows may start picking up. However, there are some fundamental factors that have also helped. Chinese oil imports have fallen significantly, while US oil exports hit record levels consistently in April, which has helped to take some of the upward pressure off the market. But these are temporary solutions. China will be relying on inventory as imports fall, while similarly the growth in US exports is fed by inventory rather than supply growth.

Another element which has contained the market is that we have already started to see demand destruction in the oil market. Crude oil prices have not had to go as high as many would imagine to drive this decline in demand. This can be largely attributed to the relative strength seen in refined product prices (gasoline, diesel, jet fuel), reflected by the widening in refined product margins. The significant strength in refined product prices has meant that crude oil prices have not had to go as high to ensure demand destruction.

While there is still plenty of uncertainty over how the situation plays out, we are assuming some recovery in oil flows in the remainder of the second quarter, allowing for nearer to normal flows in the third quarter. Under this scenario, Brent averages $104/bbl in 2Q26 and US$92/bbl in 4Q26. Clearly, though, every day that goes by without a resolution pushes the market towards a much more aggressive scenario.

Chinese oil imports fall while US oil exports surge amid Persian Gulf supply disruptions

Demand destruction keeps the gas market in check… for now

While European gas prices are trading above pre-Iran war levels, they have come off significantly from their peak following the start of the war. We believe that gas markets are underpricing the scale of the supply disruption. The gas market has less of a buffer to weather supply shocks, while there is little in the way of alternative routes for Persian Gulf LNG to move to its destination, other than going through the Strait of Hormuz. While ship tracking data shows that Qatar has shipped its first two LNG cargoes since the start of the war, this falls far short of normal flows.

There is not enough slack in the LNG market to offset these supply losses, so the market will have to rely on inventory and demand destruction to try to balance, which is what we have been seeing. In Asia, gas-to-coal switching is occurring within the power sector, while industrial demand is also coming under pressure. Meanwhile, relying on inventories means that buyers will have to come back to the market at a later stage to restock. The big upside risk for the market is if this restocking has to happen before energy flows through the Strait of Hormuz resume.

If we see Asian buyers coming into the spot LNG market to refill inventory/offset disrupted contracted volumes, this will increase competition between Europe and Asia for cargoes, which would push prices higher.

Gas storage in the EU is relatively tight, at 35% full compared to a five-year average of 48%. This will make the job of refilling storage tougher, especially as the TTF forward curve – currently in backwardation – does not incentivise storage. More flexibility in EU storage targets helps to take some pressure off the market heading into the 2026/27 winter. However, going into the winter with 75% full storage (which is the minimum allowed under extreme conditions) would leave the European market more vulnerable through the winter and risk higher prices.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Two anniversaries, one uncomfortable mirror

- This bundle contains 13 Articles

Included in the following ING Monthly

Two anniversaries, one uncomfortable mirror