- Quick take

- 29 April

- Uzbekistan

Uzbekistan policy rate on hold, with cuts possible but distant

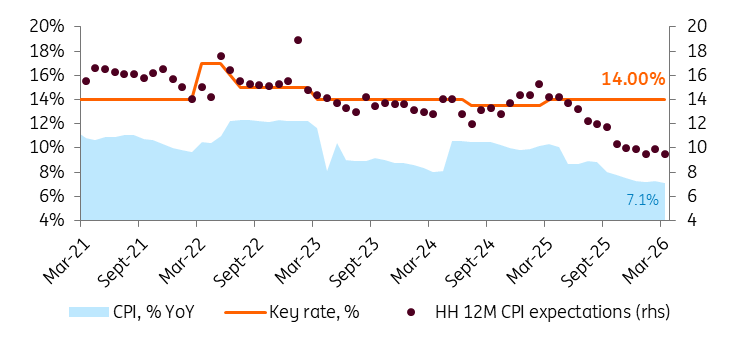

CBRU held the policy rate at 14.00%, in line with expectations. The April statement was less hawkish than in March, as slowing inflation allowed the bank to drop its hike guidance. Still, strong domestic growth and external risks challenge CBRU's CPI forecast, making near-term easing unlikely. A cut in 2H26 looks like an optimistic scenario to us

| 14.00 |

CBRU policy rateunchanged |

| As expected | |

The Central Bank of Uzbekistan (CBRU) kept the policy rate unchanged at 14.00%, in line with our expectations. This follows the recent example of Kazakhstan, which also opted for a hold, reflecting a more cautious mood in the region amid continued tensions in the Middle East.

The tone of CBRU's April statement was less hawkish than in March. We see this as signalling a reduced risk of further tightening, rather than guidance toward a near-term rate cut, as caution remains warranted.

Dovish shift compared to March

- Inflation assessment improved: headline CPI slowed to 7.1% YoY in March, moving toward the CBRU’s 6.5% YE26 forecast; core CPI stopped accelerating and fell to 5.7% YoY; households’ inflation expectations continued to decline.

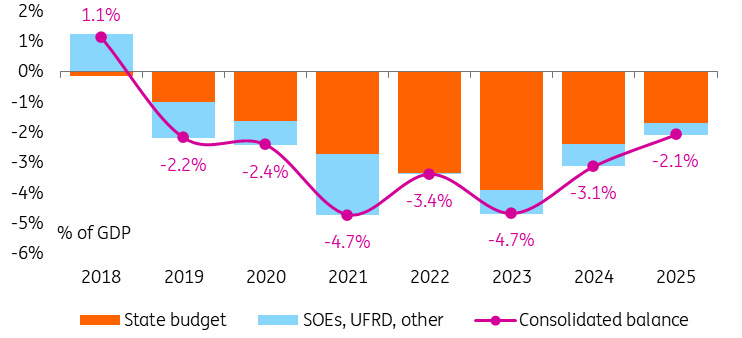

- Fiscal impulse played down: budget expenditures are no longer cited as a growth-supportive factor, consistent with fiscal consolidation. According to recent reports, the consolidated budget deficit shrank to 2.1% of GDP in 2025, by 1pp vs 2024 and 2.6pp vs 2023.

- Tightening guidance removed: April forward guidance refers to ensuring “sufficient restrictiveness” if pro-inflationary risks materialise, replacing March’s explicit signal that policy may be tightened further.

CBRU holds the policy rate despite improved CPI and households' inflation expectations

Reiterated restrictive messages

- Inflation remains above the 5% medium-term target, and inflation expectations are still not fully anchored.

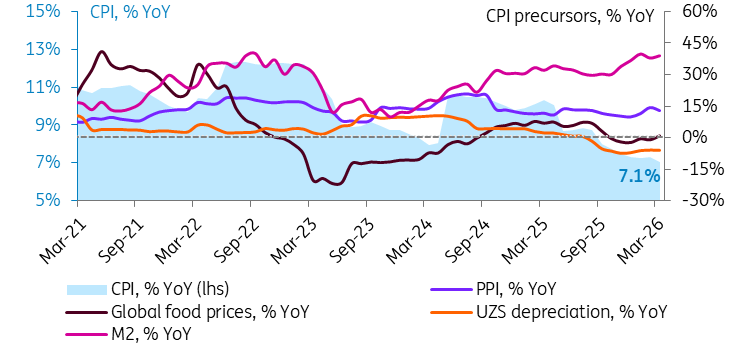

- External risks (geopolitics, oil and food prices, logistics costs) continue to skew toward higher imported inflation pressures for Uzbekistan, despite the recent moderation in PPI growth to 13.0% YoY.

New hawkish signals

- Domestic demand stronger than expected: GDP growth surprised on the upside at 8.7% YoY in 1Q26, prompting an upward revision of the official 2026 growth outlook to 7.0-7.5%.

- Disinflation seen as fragile: part of the recent CPI slowdown is attributed to base effects, signalling limited confidence in a durable disinflation trend.

CPI precursors call for caution

Implications for rates and FX

With global commodity price assumptions edging higher and domestic demand in Uzbekistan continuing to outperform despite fiscal consolidation, our base case is for YE26 CPI to reach 8.0% and exceed the official forecast by around 1.5pp, implying an extended hold on the policy rate. That said, scope for a modest cut could open in 2H26 as an optimistic scenario, if inflation continues to drift toward the CBRU’s 6.5% YE26 projection.

High positive real rates, reduced fiscal risks, potential to ramp up physical gold exports, and portfolio inflows amid debt and equity placements (sovereign Eurobonds, UzNIF IPO) reinforce our constructive view on the soum, which has gained 1.5% vs USD since the outbreak of the Iran war despite a 13% correction in gold prices.

Fiscal consolidation of 2024-25 contributed to disinflation, remains a factor to watch

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more