- Quick take

- 29 May

- South Korea

Energy shock dampens Korean activity, but probably only temporarily

South Korea’s all-industry output fell for the first time in three months in April as the energy shock hurt the entire economy—from manufacturing to services to construction to consumption. While some sectors may remain under pressure, we cautiously expect a rebound in May thanks to a recent recovery in sentiment and improved supply conditions

| -0.7% |

Industrial production (%MoM, sa)1.5% YoY |

| Lower than expected | |

Energy shocks dent manufacturing activity in April

As we noted in our earlier research, the South Korean economy is being pulled in opposite directions. Global AI boom-led growth is fueling demand, while energy disruptions are denting the domestic economy. Yet April activity data clearly illustrates the war’s impact on the economy. Industrial production dropped more than expected – by 0.7% month-on-month, seasonally adjusted, in April (vs 0.4% consensus, 0.3% ING), though March was revised upward to 0.6% from 0.3%.

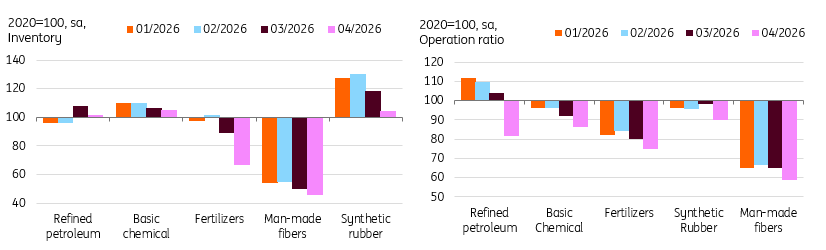

A strong chip cycle led to gains in output (3.1%) and investment. Meanwhile, oil refinery activities were weak. Output dropped sharply by 19.4%. Inventory and operation ratios declined most notably in these industries.

Energy shocks hit oil refinery activities hard

The energy shock extended beyond manufacturing

Service and investment activities contracted. Within services, weak consumption weighed on retail and wholesale activity. Financial services declined alongside the sharp fall in local equities.

Equipment investment dropped 3.6%. As mentioned earlier, chip-making equipment rose, but transportation equipment dropped with a notable decline in aircraft imports. Meanwhile, construction investment declined for a second month. Compared to the last couple of years, construction has clearly bottomed out, even if the recovery is quite modest. The recent surge in material prices and shortages of some construction materials should add to the burden on the already fragile recovery.

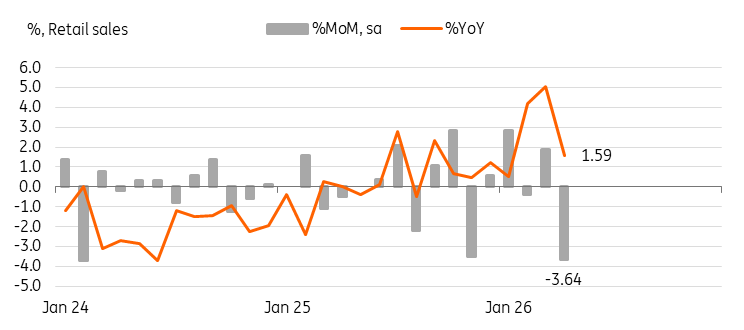

A notable decline in fuel consumption led to overall drop in retail sales

The energy shock weakened consumption. Retail sales dropped 3.4% MoM. Fuel saw the largest drop, down by 8.3%. The government's gasoline price controls helped stabilise fuel prices, but still-high prices should dampen demand. Also, the government imposed some limitations on car operations, another reason for the sharp drop in fuel consumption.

Durable goods consumption also weakened quite meaningfully. Auto (-6.4%), home appliances (-12.8%), and furniture (-4.6%) all dropped. The contraction of telecommunications and computers was notable (-29%), but the volatility is also related to new product launches in March.

Retail sales dropped quite notably in April

We cautiously expect a recovery from May

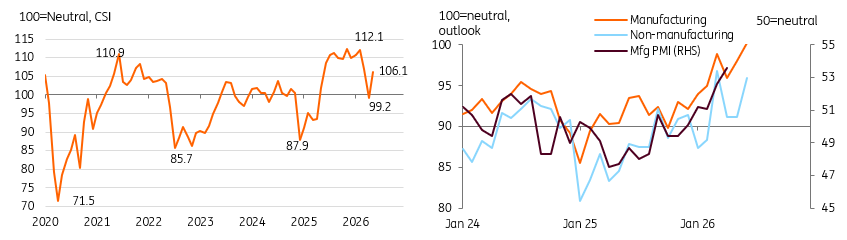

Today’s data show the domestic economy being hit harder by the energy shocks. Semiconductors are doing heavy lifting, but overall activity declined. The situation in the Middle East hasn’t changed much, but we cautiously expect a recovery starting in May. Both consumer and business sentiment are mproving. We believe that the government’s cash payouts should provide some buffer against a decline in consumption. For business sentiment, semiconductor performance remains strong.

Also, we’re hearing from industry and government that energy supply has gradually improved since May. It’s still remarkably low compared to the pre-war level. But export bans on key petrochemical materials and increased imports from non-Middle Eastern countries are at least helping to mitigate the shock.

A major chip maker preemptively reduced its production in late May ahead of a scheduled labour strike. But, the strike did not happen as both parties reached an agreement, so the reduction of output should be limited. We expect manufacturing and construction to remain weak, but consumption and facility investment to rebound in May.

Today’s data suggested a sharp deceleration in growth in the second quarter, down from a 1.7% gain in the first quarter. If we’re right about the recovery in consumption and investment in May and continued strong exports, the economy is likely to avoid a contraction in 2Q26.

Despite prolonged war, consumer and business sentiment improved in May

BoK watch

Today's data was weaker than expected. It wasn't bad enough, however, to prevent the Bank of Korea from delivering a hike in July. The BoK clearly had a positive view on growth but acknowledged the negative near-term impact of the energy shocks. Today's data shouldn't be much different from the BoK's own projection. As we argued in our BoK review note, we believe that the central bank will deliver two hikes in 2026 amid strong growth and higher inflation. The strong chip cycle is expected to continue in 2027. Thus, overall growth should remain firm next year, but the tightening monetary policy environment could place a great burden on highly indebted households, small businesses, services, and construction. Thus, we expect the BoK's rate hikes to peak at 3.25% in 1H27.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more