- Quick take

- 28 May

- Rates South Korea

Bank of Korea signals interest rate hikes are near

The Bank of Korea held its policy rate steady at 2.5%, with two dissenters calling for a 25 bp hike. Higher GDP and CPI forecasts for 2026 and 2027 reinforce our view that BoK hikes could persist into 2027. For now, July is our base case for the next tightening move

| 2.5% |

BoK policy rateTwo dissent votes |

| As expected | |

Clear hawkish shift and higher likelihood of two rate hikes in 2H26

The Bank of Korea left its policy rate unchanged today, but Governor Shin Hyun-Song struck a surprisingly hawkish tone. He said a rate hike could have been justified today, though a majority of board members preferred to wait and monitor how developments in the Middle East affect core-inflation. He also stressed that current macro conditions - inflation, growth, FX and rates - all support hikes in the coming months. We believe that the latest dot-plot, centred around 3.0%, accurately reflects the BoK’s view. Six months out, though, he stuck to the standard response that the BoK will remain data-dependent. Shin did not provide a clear answer on whether the market pricing of four hikes is appropriate.

Higher GDP and CPI forecasts point to further rate hikes after 2026

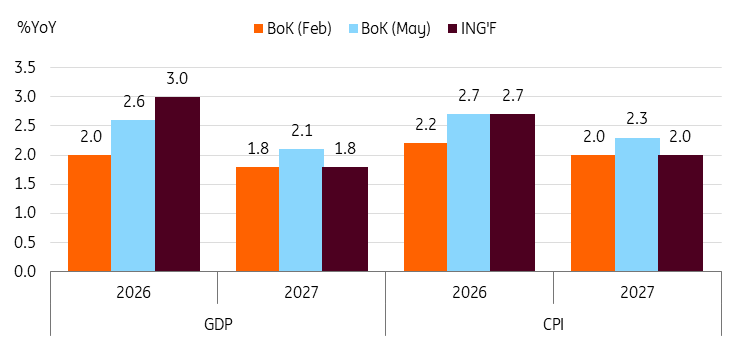

The latest quarterly outlook report showed that GDP is expected to grow 2.6% year-on-year (vs previous 2.0%) in 2026 and 2.1% (vs 1.8%) in 2027. Now, the BoK expects GDP to grow above potential for two consecutive years. Also, Governor Shin said that the GDP output gap would turn positive sometime next year. This is likely to lead to higher inflation in both years. Inflation is expected to rise to 2.7% (vs 2.2%) in 2026 and 2.3% (vs 2.0%) in 2027, suggesting that secondary effects of energy prices remain sticky and that rising asset prices are likely to continue to push up core inflation. We currently pencilled in a 25 bp hike in the first half of 2027. But today’s outlook suggests that the possibility of another 25 bp hike is increasing.

GDP and CPI revised upwardly for 2026 and 2027

Our base case remains a total of 75 bp hikes, with moves likely in July, October and 1H27

As we noted in our Korea macro outlook last Friday, the global AI boom will likely more than offset the energy shock, and improved terms of trade should support strong growth this year. Governor Shin also said the sharper rise in GDI (12.3% YoY) compared to 3.6% gain of GDP was largely driven by better terms of trade and is likely to spill over into broader growth.

The main difference between the BoK’s view and ours is that we expect limited spillovers from semiconductor-driven growth. We expect the energy shock and inflation to weigh more heavily on the domestic economy, particularly on the services and construction sectors. Meanwhile, the BoK expect construction and private consumption to recover quite meaningfully.

Rising equities and bonus payments should support overall growth, but the gains are likely to be concentrated among higher-income households. We believe the BoK should be mindful that excessive rate hikes could deepen the K-shaped recovery and hurt already fragile domestic growth. At the same time, still-high household debt, including mortgages and other private credit, should limit the BoK's rate hikes.

We now see a greater chance that the BoK could turn more hawkish than we expect, raising the risk of additional hikes beyond our base case. But weak domestic demand should keep the tightening cycle gradual, with the terminal rate at 3.25%.

Recent Korean financial market moves were mostly driven by middle east situation and global trend

Governor Shin believes uncertainty in the Middle East is behind current financial market volatility, and that both rates and the KRW should stabilise if tensions ease. But, he made clear that the BoK will respond firmly to any excessive one-sided moves in FX.

We also agree that geopolitical risk is one of the key factors behind the weakness in KTB and KRW. Beyond the geopolitical tensions, we believe that markets will follow the fundamentals of the Korean economy.

For the KRW, we expect it to trade in a quite wide range between 1,450 and 1,550. But it could come down to the 1,475 level upon the easing of tension. BoK policy action ahead of the Federal Reserve should also help to stabilise the KRW further. However, we think that as long as the Fed Fund Rate stays above the BoK's policy rate, the USDKRW appreciation should be limited and likely stay around 1,450 level.

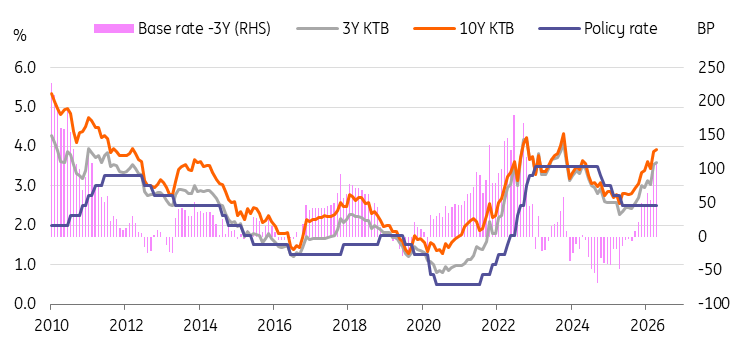

Thanks to quite hawkish comments from the BoK, 10YKTB yields rose again to 4.2% today. If geopolitical risk eases, market rates are likely to level off slightly, but they are likely to remain around 4.0%. We believe market rates tend to move ahead of the monetary policy cycle, and the market is already fully pricing out four rate hikes. Thus, once the BoK begins its rate hikes in July, the 3Y10Y curve is expected to flatten rather than steepen. Also, even if the BoK's rate hikes are expected to continue next year, market yields are likely to trend toward 3.75% starting in the latter part of this year.

Market rates tend to move ahead of the monetary policy cycle

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more