- Quick take

- 17 February 2020

- Russia

Russian industrial production pressured by weather and statistical rebasing

Russian industrial output growth underperformed expectations in January, mainly due to revision in historical data. The latter also showed Russia's dependency on budget spending and commodity exports. As a result, the key question for the Russian industry this year is whether coronavirus can be cured with public spending

| 1.1% |

January industrial production, % YoYDown from 1.7% YoY in December 2019 |

| Worse than expected | |

Don't read too much into the January slowdown

Russian industrial production reported 1.1% year on year growth in January 2020, showing a slowdown versus the previous month and underperforming market expectations of 1.6% and our forecast of 1.7%. Neither of the two are a cause for concern. Here's why:

- The slowdown was widely expected, as the abnormally warm weather in January 2020 (the average temperature in Russia was more than 5 degrees higher YoY) led to reduced demand for heating. Indeed, the heat and electricity distribution sector (10% of the total industrial output) posted a 4.7% YoY drop, being the main drag on the overall figure.

- The manufacturing sector, accounting for 49% of the overall industrial production, continued posting healthy 3.9% YoY growth in January, in line with 4Q19 dynamics. Subsectors showing strong growth include food processing, industrial chemicals, and construction materials. Subsectors lagging behind include textiles, oil downstream, engineering equipment, consumer electronics, light vehicles;

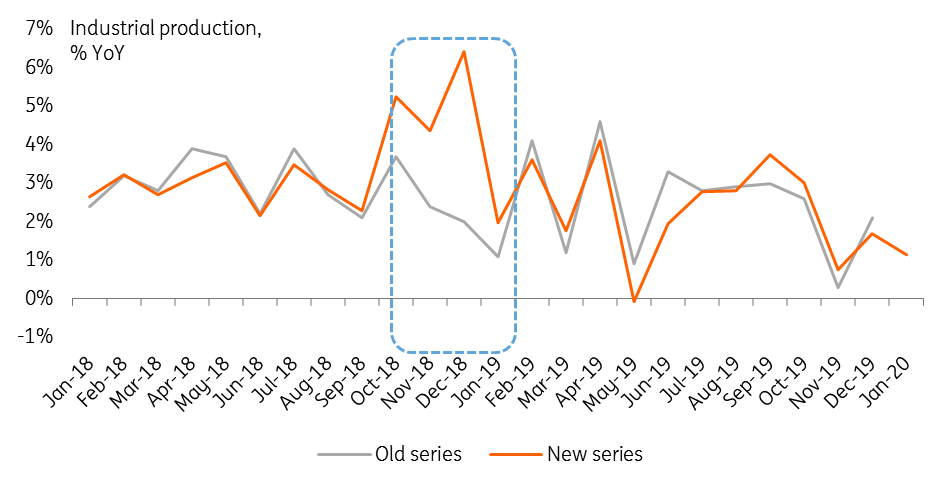

- The reason why January 2020 industrial output underperformed expectations is that those expectations were made before the massive revision in the historical data (see Figure 1), which occurred today. Having accounted for some changes in the structure of industrial output over 2010-18 and having addressed some cases of errors in companies' self-reporting forms, the Russian state statistics service, Rosstat provided the new time series for 2018-19, showing significant upgrade in 4Q18 (thanks to revision in manufacturing from 0.9% YoY to 4.1% YoY) and in January 2019 (thanks to revisions in other sectors, mainly commodity extraction from 4.8% YoY to 5.4% YoY). The latter led to the higher statistical base for January 2020, explaining the below-expected result.

Figure 1. Statistical base for January 2020 increased due to backward revision

Looking ahead: budget spending vs. coronavirus

Our unenthusiastic attitude towards January industrial data should not, however, be extrapolated for the rest of the year. There are two main observations from the backward revision in the industrial output data, that may have long-term consequences for industrial trends this year.

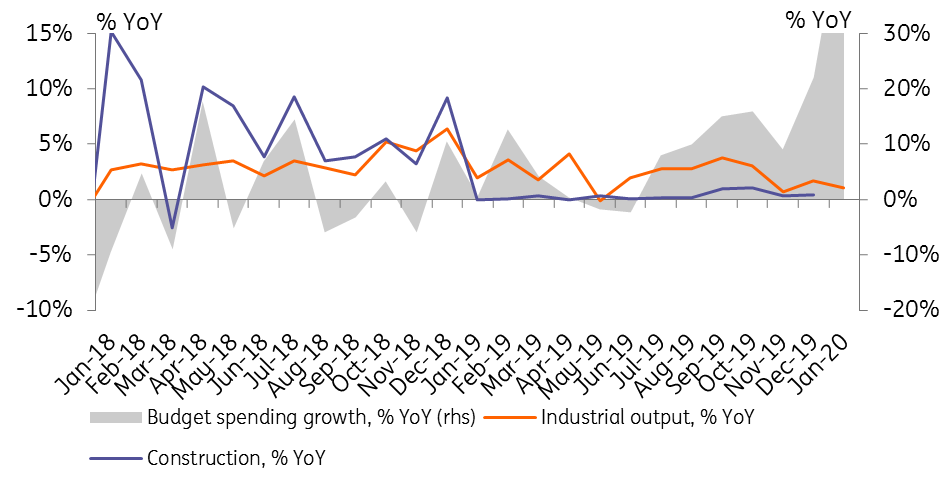

- The new time series (so far only 2018-onwards is available) for industrial production show better correlation with construction growth and budget spending. This is not coincidental: earlier Rosstat upgraded 2018 construction numbers incorporating projects previously unaccounted for, including infrastructure for the Football World Cup-2018 and oil downstream projects on the Yamal peninsula. The subsequent upgrade in industrial output seems logical, as construction drives industry directly through finished construction materials and indirectly through commodities (mostly metals) and machinery&equipment production. The construction sector, in general, shows a high correlation with budget spending (see Figure 2), reflecting the overall dependence of the real sector on the government support.

- Rosstat reported an increase in the share of commodity extraction sector in 2010-2018 from 34% to 39% at the expense of other sectors. It appears that commodity extraction, which is driven primarily by the external demand remained defensive in the last 5 years, while the domestically-oriented parts of the economy were under pressure of geopolitical tensions and economic policies aimed at macro stability. Indeed, the recently released GDP data suggests that Russia's exports kept growing in real terms for the entire 2010-18 period, while local consumption and investments were seen in red in 2014-16.

So, the first observation is potentially good news for 2020.

With the Russian government willing to unwind fiscal policy, public spending may show around 10% increase this year, and this expenditure may become more focused on infrastructure as well as social support - being positive for both heavy industries and even consumer-driven stories. The second observation, is a cause for concern, as the recent coronavirus outbreak is a risk factor to Russia's exports of oil and metals.

As a result, while previously the question was to what extent the easing in the fiscal policy and acceleration in the National Projects will accelerate the GDP growth, now the question is whether the local fiscal stimulus will be able to offset the negative effect from potential deterioration in the global demand.

Figure 2. Budget plays important role for construction and industrial output

We do not take the January disappointment as indicative of the full-year trend in industrial production. Overall, we remain optimistic, as the expected inflow of public spending should support industries focused on infrastructure and potentially even consumer-driven stories. Meanwhile, coronavirus is the new risk factor for industrial output, which over the last eight years became more dependent on commodity extraction.

In the near term, we are looking for the full set of activity data for January (to be released between 19-20 February) as a broader indicator of the near-term economic trends. In the meantime, banking statistics (20 February) should also be worth following.

While government policies and market discussion is currently centred around fiscal stimulus, we believe structural/institutional measures would have a bigger economic response - potentially through decline in the savings rate among the wealthy one-third of households (seen through slower deposit growth) and higher investment demand in sectors not directly dependent on the public spending (seen through higher corporate loan growth).

None of that is our base case scenario for now but it is definitely a factor to watch.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more