- Quick take

- 18 February 2020

- Commodities daily

The Commodities Feed: LNG pressure

Your daily roundup of commodity news and ING views

Energy

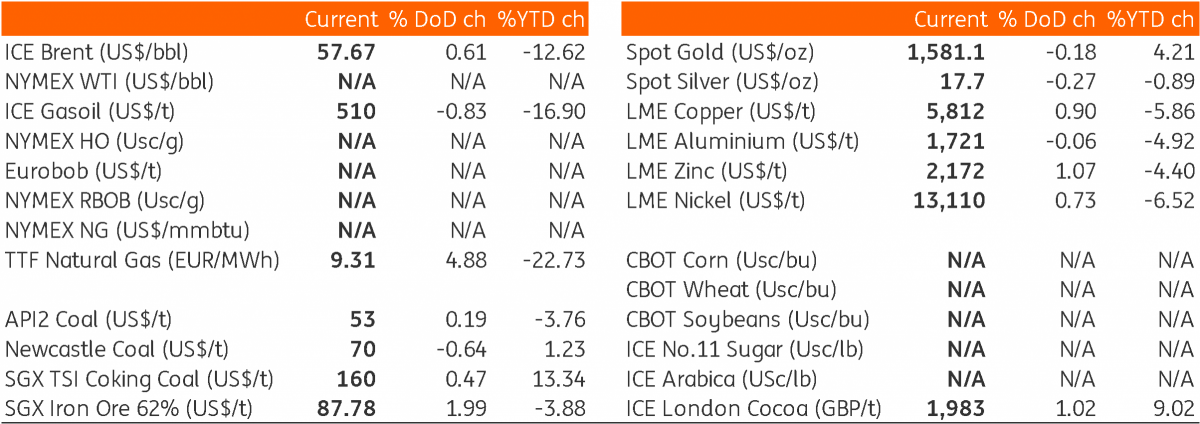

ICE Brent closed higher for a fifth consecutive day on Monday, taking the market to levels last seen back in late January. It has been a fairly quiet start to the week, possibly owing to the fact that it was President’s Day in the US yesterday. The strength in the market was not isolated to the flat price, with the prompt ICE Brent time spread continuing to strengthen, trading to a backwardation of US$0.18/bbl. Opportunistic buying at lower levels appears to have provided a floor to the market for now. Meanwhile, Libya’s National Oil Corporation has said that oil production in the country has fallen to 135.7Mbbls/d, as a result of the export blockade that continues in the country. For now, this lower supply is helping the rest of OPEC+ out and allowing them to delay a decision on further cuts. However, if this supply were to return to the market fairly quickly, this would likely require a timely response from OPEC+ given the current demand picture. Finally for oil, given it was a public holiday in the US yesterday, weekly oil numbers will be delayed by a day. Therefore API numbers will be out tomorrow, whilst EIA inventory numbers will be released on Thursday.

Finally, moving to LNG and spot prices in Asia continue to come under pressure, with the market trading below US$3/MMBtu now. The surplus environment expected in the market this year meant that prices were always going to be under pressure for much of the year. However Chinese demand concerns and the risk of Force Majeure declarations have only weighed further on the market. This pressure in the Asian market continues to have repercussions on other regional markets, with European hub prices continuing to trade at depressed levels, with the threat of additional spot cargoes making their way into the region.

Metals

Copper along with other base metals made a positive start on Monday supported by China’s move to reduce its interest rates on medium-term loans to the lowest since 2017. LME copper edged above the US$5800/t mark (the highest level in three weeks), with further stimulus measures expected from the Chinese government. Meanwhile, LME data shows that copper cancelled warrants jumped by 8.5kt (the highest since last November), bringing the total to 36kt yesterday. Total LME copper inventories stood at 161kt as of 17th February- largely unchanged. However, a weaker property market is a concern for metals demand in the near-term, with the latest data from NBS showing that China’s new home prices expanded by just 0.27% MoM in January; the slowest growth since February 2018.

Turning to spreads, and there is a clear divergence between sister metals, lead and zinc. The LME lead cash-3m backwardation has grown to US$30/t, while the Feb/Mar spread jumped to US$37/t yesterday, compared to just US$7 a week ago. Meanwhile, the contango at the front end of the curve for zinc continues to steepen, with the cash-3m spread climbing to US$15.25/t.

Turning to precious metals, and following Johnson Matthey last week releasing its expectations for a deeper supply deficit in 2020 for palladium, Anglo American, estimates the deficit for palladium to widen to 1.9mOz in 2020, compared to a 1.2mOz deficit last year. However, this outlook will depend on how the auto industry performs this year, and at the moment it is not looking that constructive. Last week China Passenger Car Association (CPCA) estimated that car sales could drop by more than 30% MoM in February, after posting its biggest decline of 22% MoM in January.

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more