Russian 2020 GDP: better economic activity does not guarantee better market returns

- 3 February 2020

- Russia

2019 GDP performance was driven by the budget policy, suggesting that the upcoming fiscal easing may lead to stronger economic activity in 2020. Meanwhile, the associated import recovery may become a drag on the ruble, while the still strong growth in consumption, evident even in 2019, may limit the downside for local rates

| 1.3% |

Russian GDP growth in 2019down from 2.5% in 2018 |

| Higher than expected | |

Russian GDP slowed in 2019 but the year-end performance was stronger

According to the first estimate of the Russia's official statistics service (Rosstat), the country's GDP slowed from the recently upgraded 2.5% in 2018 to 1.3% in 2019, which is slightly higher than our conservative forecast of 1.0% and consensus of 1.2%. The slowdown vs. 2018 was no surprise, given the negative effect of the VAT rate hike and a pause in the state investment cycle. Meanwhile, the released figure and growth composition still allows us to make new observations and conclusions.

1. Although the official quarterly breakdown of the GDP growth has yet to be released (4Q19 data is not available yet), it appears that 4Q19 economic activity has been better than the annual average. Given the earlier released 9M19 numbers (which however can be revised later), 4Q19 GDP growth could have totaled 1.9-2.2% year on year, exceeding both the 0.7% YoY in 1H19 and 1.7% in 3Q19.

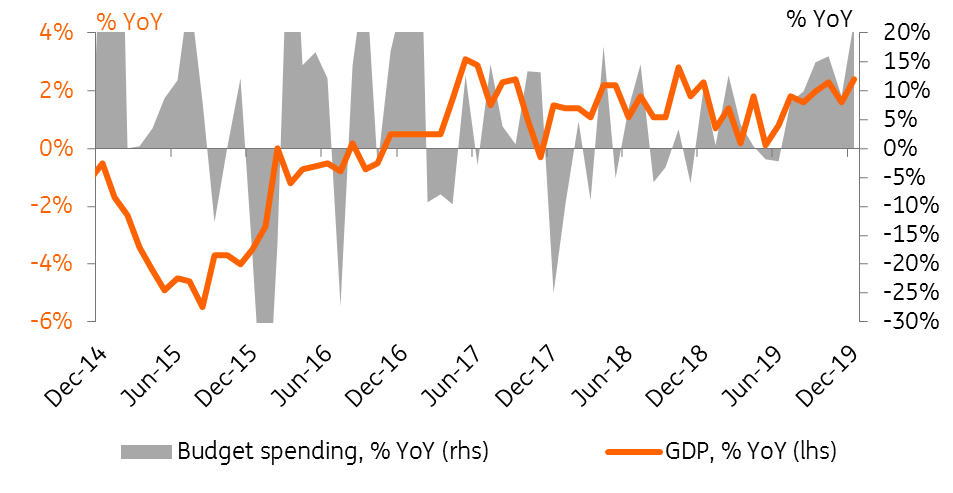

2. Budget policy seems to be the primary driver of economic activity. While the 1H19 performance was constrained by the VAT rate hike and significant undeperformance in state spending vs. the annual plan (federal spending growth was 2% YoY in 1H19), the 2H19 growth was supported by the catching up on the budget spending to 11% YoY in 3Q19 and 17% YoY in 4Q19 (see Figure 1).

Figure 1. Russian GDP growth accelerated in 2H19 on higher budget spending

State-driven sectors may perform better in 2020 on fiscal easing

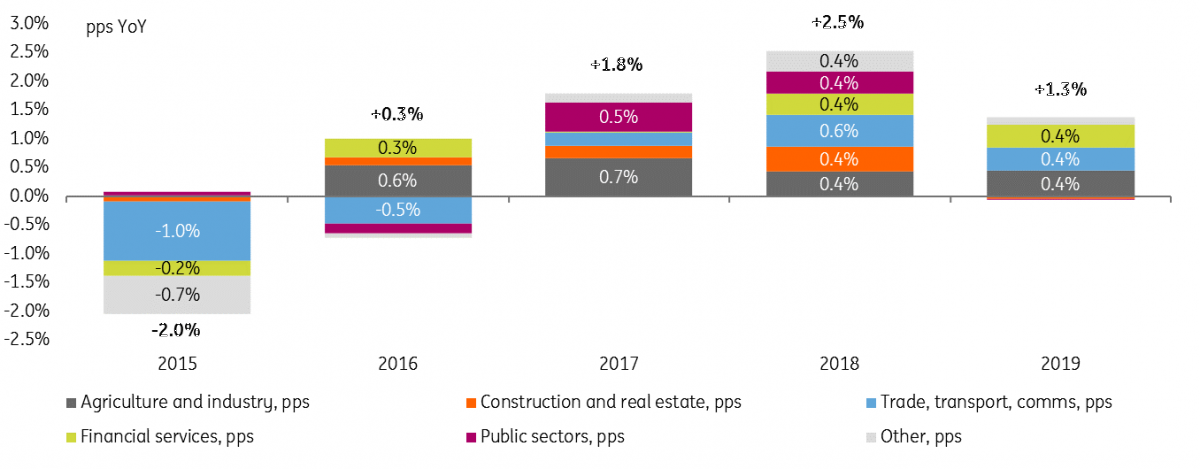

3. The output-based GDP breakdown (see Figure 2) generally confirms that budget policy has been the most important variable in 2019. The sectors that contributed to the GDP slowdown in 2019 include public sectors (state administration, military&security, education, healthcare, scientific research), as well as construction and real&estate. Together those sectors account for 0.9 pp out of a total 1.2 pp GDP slowdown in 2019. Meanwhile, industrial sectors, agriculture, trade, transport, and financial services did not see a material deterioration.

4. As we mentioned earlier, the recent government reshuffle is a sign of a potential relaxation in the budget policy, which could include an unwinding of the accumulated spending backlog of around 1% of GDP, repositioning it in favour of social payments, investments into human capital and infrastructure, and delivery on the promises to make local investments from the National Wealth Fund of around 0.3% GDP per annum. This should benefit all the sectors that underperformed in 2019. The upcoming update of the budget draft (to be released by 11 February) should shed more light on the scale of upcoming fiscal stimulus and the potential impact on GDP growth.

5. While initially we were planning to upgrade our conservative 1.5% GDP growth forecast for 2020 as a result of the fiscal easing, the recent news on Coronavirus creates additional uncertainties. Over the last ten years China has gained importance as Russia's trade partner (share of China in exports increased from 6% to 13%, in imports - from 14% to 22%). According to a recent ING research report, China accounts for 70% of world's iron ore imports, which leaves the Russian metals sector exposed. In addition, the apparent 20% drop in oil demand in China is another test, as oil is the primary Russian export commodity to China. Finally, with 1.5-2.0 million Chinese tourists visiting Russia annually and spending US$5-7k per trip, the recent restrictions on travel can negatively affect the local retail trade and services sectors, including transport, hospitality, and restaurants at least in 1Q20.

Figure 2. State-driven sectors disappointed in 2019, may recover in 2020

Import growth will be a challenge for 2020

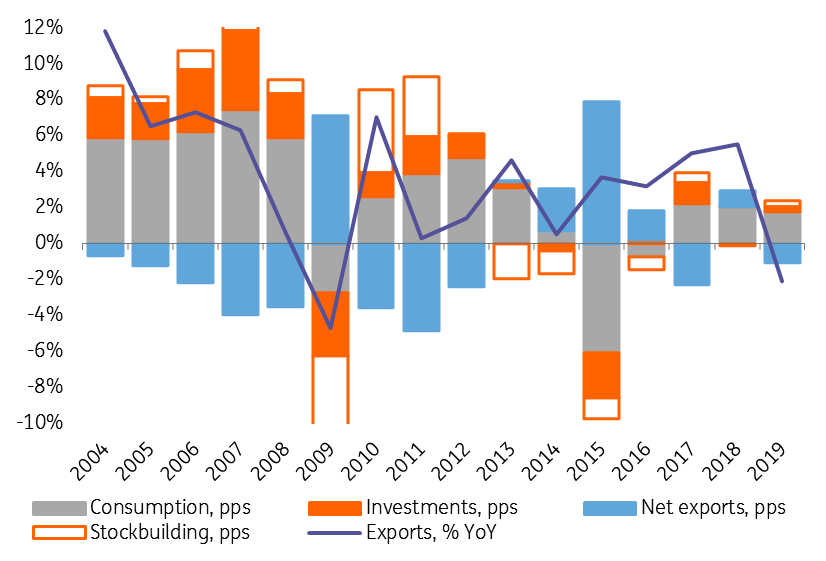

6. The usage-based GDP breakdown (see Figure 3) suggests that net exports was a major drag on 2019 GDP growth, with exports dropping 2.1% YoY, the first drop since 2009, which may have been caused by Russia's OPEC+ commitments. Meanwhile, the upcoming OPEC+ meeting this week is a watch factor for additional export cuts as a response to the drop in global demand.

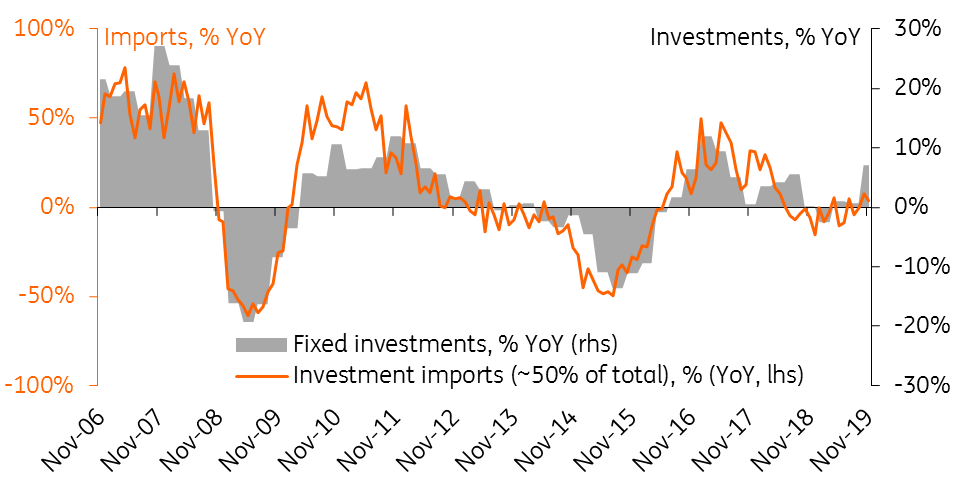

7. Import growth posted a modest 2.2% recovery in 2019, however this figure masks a material acceleration in 4Q19, as the preliminary 9M19 figure was negative. This acceleration coincides with a material acceleration in the budget spending on the national economy (mostly infrastructure spending) from 4% YoY in 9M19 to 35% YoY in 4Q19, which led to the apparent acceleration in fixed investments from flat 9M19 to 1.4% YoY in 2019 and the pick-up in investment imports (machinery, equipment, transport) accounting for around 50% of Russia's total merchandise imports (see Figure 4).

8. With expected fiscal easing and catch up on both infrastructure and social spending, we expect 2020 fixed investments and consumption to accelerate from the 1.4% and 2.4%, respectively seen in 2019. Meanwhile, we believe this acceleration will trigger higher imports as well: looking at the historical performance of GDP at constant prices (in real terms), increase in annual local demand by RUB 1 triggers an increase in annual imports by around RUB 0.3-0.4. This is the basis for our expectations of a noticeable shrinking of the Russian current account in 2020, which should contribute to a weakening of ruble fundamentals. As a result, for now we keep our initial expectations of USDRUB weakening to 66.0 by year-end, while acknowledging that the Coronavirus outbreak is an ongoing event, which can result in significant intra-year volatility.

Figure 3. Net exports suffered on weak exports in 2019...

Figure 4. ...and may be challenged by higher imports in 2020

Consumption not as weak as it seems

9. The most surprising revelation from the 2019 GDP growth structure was that despite the increase in VAT rate, and generally weak income trend for most of 2019, overall consumption growth decelerated only modestly - from 2.8% in 2018 to 2.4% YoY in 2019. While partially this reflects an increase in state procurement, household consumption also posted a 2.3% YoY growth in 2019, exceeding the 1.6% retail trade figure. The difference between the two indicators may reflect the growing importance of e-commerce, including cross-border (AliExpress, etc).

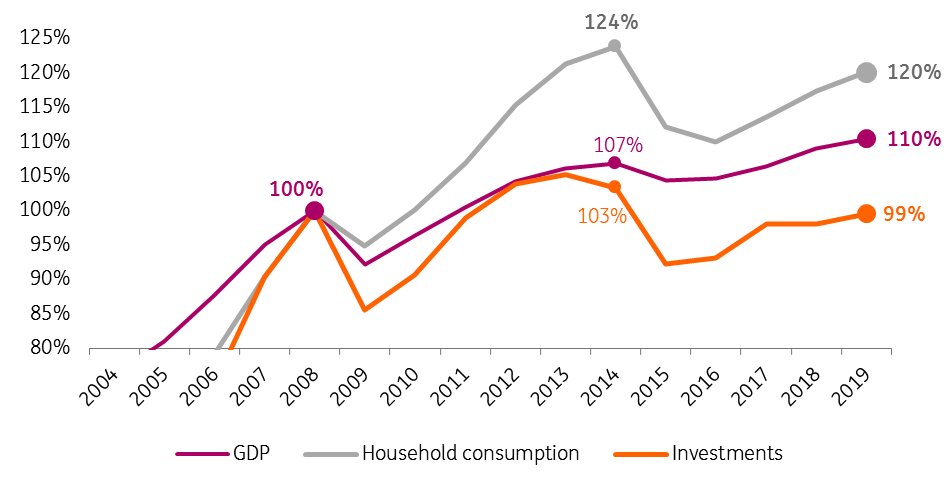

10. Looking at the long-term GDP trends (see Figure 5) it is evident that household consumption remains the strongest component of Russian GDP, being only 3% below its pre-cris 2014 level and 20% higher than the pre-crisis 2008 peak. Compare this with fixed investments, which are still 4% below their 2014 value and 1% below the 2008 level. This breakdown explains why the Central Bank is limiting the unsecured consumer lending growth and why the Russian government is now focusing on the National Projects, which are primarily infrastructure as the key tool of supporting the economy.

11. Another implication from the relatively strong consumption is that it undermines the argument of some observers and state officials, that the slowdown in the CPI seen in 2019 was driven by weak demand. It rather confirms our take that the causes of the CPI slowdown are on the cost side, which can be volatile. Combined with expected fiscal stimulus to both consumption and investments expected in 2020, this strengthens the argument in favour of a cautious monetary policy stance, which we expect to be reiterated at the upcoming Bank of Russia meeting on 7 February. For now, the market seems to continue pricing several cuts in the key rate for this year, which in our view seems optimistic.

12. The recent Coronavirus outbreak may be an additional factor of uncertainty for inflation. So far Russia suspended imports of oranges and fish (16% of Russia's imports) from China, and a large Russian retailer Magnit has suspended imports of Chinese fruit and vegetables, accounting for 3% of the chain's turnover. Lower competition on the local food market may be a factor of upward price pressure, however it seems that Russia's dependence on the Chinese food is rather low, with only a 5-6% share in Russia's total food imports. Meanwhile, on the Russian non-food consumer market (so far no restrictions in place) China's role is more noticeable, as it accounts for around 40% of imported clothes and shoes, as well as 50-60% of consumer electronics. Any news regarding a drop in supply of Chinese durables will also be a watch factor in the coming weeks.

Figure 5. Household consumption strong despite VAT hike, weak income

2019 was a year of strong financial markets and weak economic growth in Russia, and even before the Coronavirus outbreak it seemed that 2020 could bring the opposite result. While the fiscal stimulus of 2020 may assure some improvement in local state-driven consumption and investment demand, the resulting pick-up in imports may erode the ruble's fundamentals and limit the scope for monetary policy easing because of higher inflationary risks.

Meanwhile, the said virus emergency is the new factor of uncertainty for economic and market forecasts, as it may lower Russia's exports of goods and services in both real and nominal terms. We maintain our inital conservative forecasts for 2020 (1.5% GDP growth, year-end USDRUB 66.0, 3.7% CPI and 6.0% key rate) until more clarity comes on the scale of fiscal easing in Russia and the Coronavirus outbreak is contained. Given that the latter is likely to somewhat lower the effect of the Russian fiscal stimulus, the importance of non-fiscal measures (ie, those affecting confidence beyond the state-driven sectors) is gaining importance and is likely to be in focus of the invesment community after the dust settles.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more