- Quick take

- 17 June

- Sweden

Riksbank’s unconvincing hawkish attempt

Sweden’s central bank tried to sound more hawkish as it held rates today, but new inflation and rate projections are at odds with market bets on a 2026 hike. Inflation is low and expected to remain below target until 2027, and we therefore stick to our call of no hikes by the Riksbank this year. Still, we aren’t turning negative on the krona

The Riksbank decision today was fully in line with our expectations. A hold at 1.75% was accompanied by policymakers trying to sound hawkish, likely hoping to preserve tightening expectations as an inflation-expectation hedge. Markets were unconvinced, though, as – predictably – the updated projections sat uneasily with the statement’s claim that the probability of a hike in 2026 has increased.

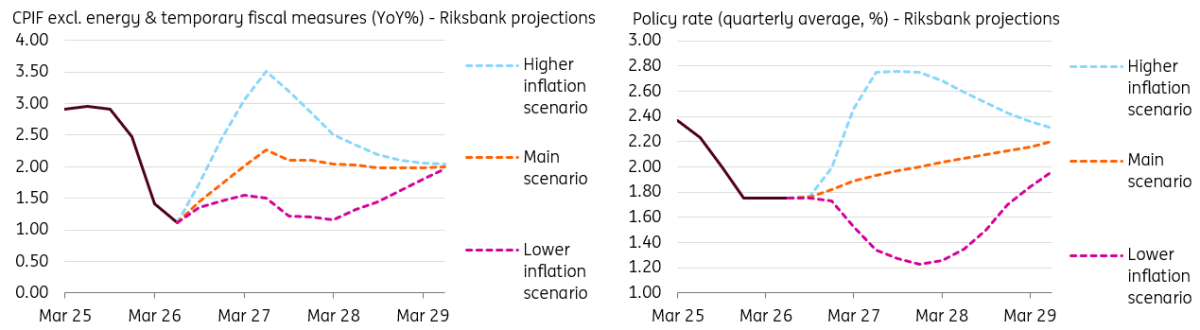

The Riksbank shifted focus from the headline CPIF – which has been heavily dampened by a food VAT cut – to a more core measure, which strips out energy and temporary fiscal measures. That is likely to prevent markets from reading the headline CPIF forecast as too dovish, given it’s expected to remain below 1.0% between July and December.

The central bank published estimates for this new measure under three scenarios: main, high inflation, low inflation. As shown below, the new core CPIF measure shows a smoother upward trend projection in the main scenario, but is still expected to remain below the 2.0% target until 1Q27: simply too low to hike. And that is mirrored by rate projections, which have been moderately revised higher but don’t fully discount a rate hike until mid-2027. A 4Q26 rate hike priced in by the market before the meeting is only included in the high inflation alternative scenario, which probably requires a return to high energy prices.

New Riksbank's inflation and rate projections

The reaction was therefore understandably dovish-leaning by the market, with front-end swap rates and the krona edging lower. From a rates perspective, we still see downside potential at the front-end of the SEK curve, as markets still have plenty of room to price out a rate hike by year-end that we don’t think will materialise.

We are instead neutral on EUR/SEK short-term as we see the wider rate differential being offset by lower energy prices and a stronger growth outlook for Sweden relative to the eurozone. In 2H, we still expect EUR/SEK to fall to 10.70.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more