Riksbank preview: Low inflation limits hawkish scope

- Yesterday, 13:08

- FX Sweden

Sweden’s central bank will struggle to replicate the ECB’s hawkishness given stubbornly low inflation. We expect a hold on 17 June. While policymakers may try to keep markets leaning hawkish, inflation and rate projections could fall short of tightening expectations. We expect no hikes from the Riksbank this year, but EUR/SEK could still fall in 2H

Markets are fully expecting a hold by the Riksbank on 17 June, and consensus is also unanimous. The question is whether policymakers will give any hints that justify the 23bp of tightening priced into the SEK curve by year-end. The determinants will be the tone of the statement, new rate projections and new inflation forecasts.

We see a greater risk that projections will fail to match hawkish pricing this week rather than exceed it. Still, policymakers should make sure to highlight inflation risks and their readiness to act in the statement; this could help limit any negative impact on the SEK on decision day.

Inflation too low to consider hikes

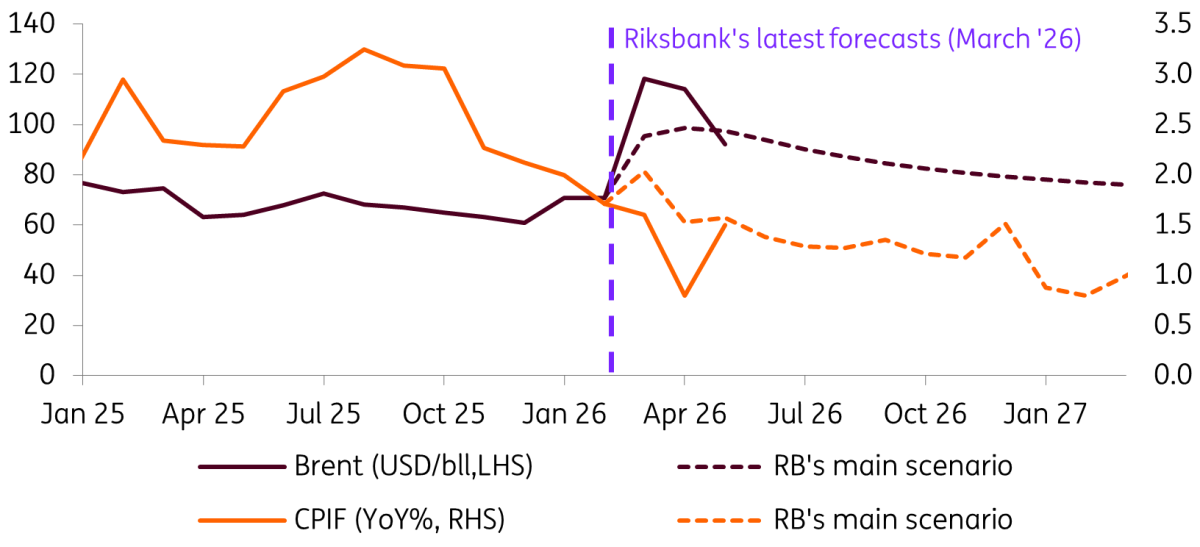

We don’t see much room for the Riksbank to turn hawkish in the statement as both headline (1.5%) and core (0.5%) CPIF inflation have remained very muted. We expect a reiteration of the wait-and-see approach on rates.

At the same time, we don’t think there will be explicit pushback against rate hike expectations, and Governor Eric Thedeen will retain some optionality on a future rate increase. Similar to the European Central Bank, concerns are centred around the de-anchoring of inflation expectations. It therefore has an incentive to keep markets leaning hawkish, particularly given European leaders’ words of caution over the timing of the Strait of Hormuz reopening.

Thedeen could also stress the currency factor again: since the ECB and other central banks are tightening, pressure on the krona may build and generate imported inflation.

Riksbank overestimated CPIF, despite higher oil prices

No upward revisions in projections

We don’t expect upward revisions in the central CPIF inflation forecast. March’s projections overestimated CPIF for March and April despite oil prices being higher than the Riksbank had forecast. Accordingly, we expect roughly unchanged rate projections for 2026, signalling no hike.

We could see a small upward revision in 2027, with the first hike being brought forward to the first half of next year and introducing some probability of another hike in the second half.

Our calls for 2H26: No Riksbank hikes, EUR/SEK slow decline

Our view remains that the Riksbank won’t hike rates this year. Our inflation estimates suggest CPIF will remain well below the 2% target, growth should soften below 2.0% year-on-year in the second half of 2026, and the September election also argues against bold hawkish moves. The trigger for a hike without an inflation jump could be a sharp weakening of the krona, which is not what we expect, especially considering the recent softening in oil prices.

We have revised EUR/SEK numbers slightly higher on policy divergence, but still target some depreciation in the second half, driven by Swedish growth outperformance relative to the eurozone and new flows of capital repatriation to Sweden. Our year-end target is 10.70.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more