- Opinion by Padhraic Garvey, CFA

One more cut from Brazil and the Selic is ‘neutral’

- 29 January 2024

- Rates Brazil

One more cut from Banco Central do Brasil and the Selic is at what we term a neutral valuation, in fact slightly through it. It does not mean the cutting is over, but it does require positive dynamics to justify future cuts, else risks elevate. Brazilian market spreads to the US look rich versus history. Mexican spreads are more attractive

How much room does BCB have to manoeuvre the policy rate lower? Not much

Recently we sent out a short report showing that Banco de México (Banxico) had the capacity to cut is key rate by 2.7% based off a simple a steady state analysis. It’s here. We now ask the same question of Banco Central do Brasil (BCB).

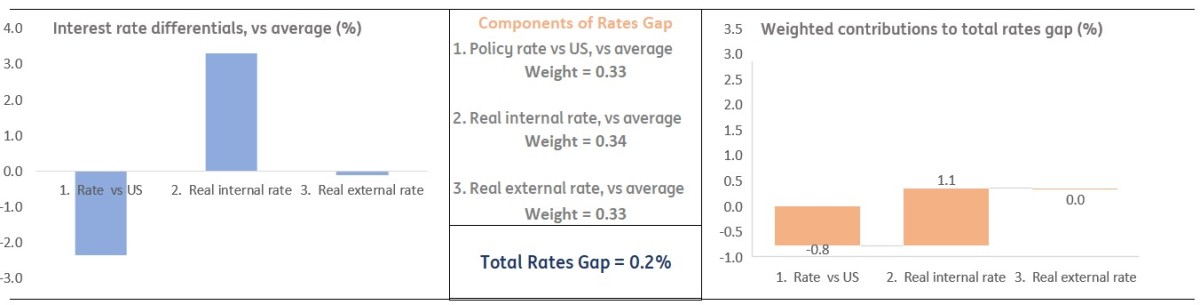

Inputs to the calculation process for the official rate and market rates

We use the same three ingredients to help identify room for policy rate manoeuvre:

- The external nominal official rate differential is the spread that the markets focus on, and it’s the one that directs FX forwards.

- The internal real rate is the domestic policy rate less inflation – the real policy rate. It’s the one the affects domestic circumstances.

- The external real rate differential is the domestic real policy rate versus the real Fed funds rate. It’s the link to control of the currency, and feedback to domestic inflation.

For Brazil:

- The moninal external rate differential is 6.4%, versus an 8.8% average. The delta is -2.4%.

- The internal rate is 7.1%, versus a 3.8% average. The delta is 3.3%.

- The external real rate differential is 5.2%, versus a 5.3% average. The delta is -0.1%.

Applying an equal weighting gives us 0.2%. This means that BCB has room to cut, but not by much. Or more succinctly, if they do, they will begin to pressure relative to averages.

Context is important here. The Selic has been cut four times since mid-2023, from 13.75% to 11.75% currently, and another 50bp cut is expected from the 31 January meeting. A move to 11.25% takes the Selic to a level we deem moderately rich to our neutral valuation.

Here’s how we calculate rate cut potential for BCB based off a steady state

The issue here is the policy rate differential versus the US. While it is comfortable at 6.4%, that’s some 2.4% below the 15yr average (graph above). It is offset by a wide real internal rate. That’s the push and pull – the elevated internal rate calls for cuts while the external rate is 'tight' when contextualised by its historical average.

There are two counters to this. First, deviating below the historical average need not be catastrophic. One standard deviation below the average is within statistical norms. The standard deviation is 3.5%. That suggests the spread could get into 5.3% without a material stretch. Second, the historical average itself could be questioned as being overly elevated.

These historical averages are a reflection of Brazil’s track record over the past decade and a half. To push through these we’d need to assume structural improvement. A key element here is the fiscal reform framework, and specifically whether enough is in the pipeline to stabilise debt dynamics. The jury remains out on this, but lower rates would help, and a weakening in domestic activity is calling for even lower rates. The issue, however, is a potential elevation in external facing risks as the Selic gets cut further through our neutral valuation.

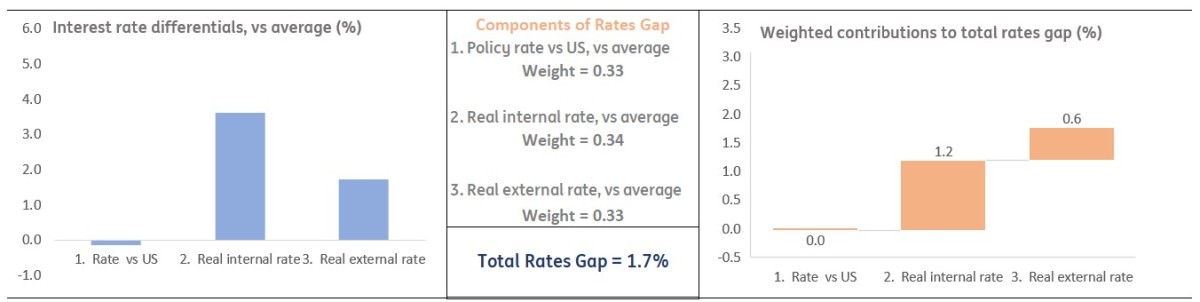

Adding some future dynamics – lower inflation and Fed cuts. What then?

Let’s take things one step forward. Hypothesise the following, 1. Brazilian inflation falls to 4%, 2. The Fed cuts by 2.5%, and US inflation falls by 1%. The chart above summarises this (likely) scenario.

Now we’d have, 1. The classic rate differential at -0.1% below average, 2. The internal rate 3.6% above average, and 3. The external real rate differential 1.7% above average. An interest rate gap has re-opened for BCB. Applying equal weighting gives us 1.7% for that gap.

So, BCB can chop its official rate to 9.75%. That's less than the current market discount for a bottom at around 9.25% on a 1yr horizon. Brazilian inflation would need to fall to 3.5% in order to square that circle (which is entirely feasible).

Market rates are already pricing a lot. There is more value in Mexico

And what does all this mean for market rates? Currently the 10yr spread to the US is 6.9% and the 2yr spread is 5.6%. Optically wide, but not when compared with historical averages. The 2yr spread is 3.3% rich to the average and the 10yr is 2.7% rich to the average. These deviations are already in excess of one standard deviation from their averages. In fact, the 10yr spread is almost two standard deviations rich to its average (just 30bp away). Given that, there is not a whole lot of value in terms of spread convergence versus the US.

Contrast this with the analysis done for Mexico, and we identify far less value in Brazil. The MEX 10yr at 8.7% is at a 200bp give-up to the BRL 10yr at 10.7%, but the value is in the MEX 10yr. Similarly, the MEX 2yr at 9.7% is only just 10bp through the BRL 10yr, and here there is more value in the MEX 2yr. The relative value in the MEX 2yr looks glaring on this measure. Receiving MEX and paying BRL results in give-ups, but the relative value signals point to MEX. This is also the case should the rate-cutting process end prematurely for whatever reason, as there is more room for MEX to perform versus less room for BRL to perform.

And what about the FX angle? USD/BRL is now in the 4.9 area and the forwards see it at 5.2 on an 18-month view. That’s the degree of BRL depreciation that should (theoretically) be tolerated by BCB. The long run averages as identified set floors below which FX vulnerability can arise. Our FX strategists identify BRL resilience as a feature in the coming months. See more here. That helps for cuts, but in fact helps MEX more than it helps BRL.

Brazil can cut, but needs justification to keep going. And lots priced into longer market rates already

On the assumption that BCB cuts the Selic by 50bp bringing it to 11.25%, our analysis shows that the Selic is then moderately rich to its neutral valuation. That does not mean that BCB can’t cut further. But it does mean that cutting further moves the Selic further into a rich valuation (versus history). This can pose risks if not backed up by improving credit circumstances.

There is a better buffer in Mexico, where we identify room to cut the official rate by some 2.7%. A key difference is BCB has already cut by 200bp (plus a likely 50bp from the 31 January meeting), while Banxico has not even started cutting. We also see this in valuations in market rates, where BRL rates look stretched versus MEX ones.

Finally you might be wondering what the steady state rate cut manoeuvre looks like for other centres. For Chile it’s 1.7%. And for Colombia it’s 1.9%. Hence Mexico scores cheapest on a steady state. Brazil scores richest. We’ll cover Colombia in detail next – stay tuned!

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more