- Opinion by Padhraic Garvey, CFA

Mexico: Plenty of room for rates to go lower

- 22 January 2024

- Rates Mexico

Banxico can cut rates as soon as it's comfortable, and we think there's plenty of room. We identify a path to sub-7% through 2024/25, with the only constraint being a lack of willingness to kick things off. Once this gets going, even though there's a lot priced in, we identify room for a 180bp convergence to the US in the 2yr and 80bp in the 10yr. It could be more

How much room does Banxico have to manoeuvre the policy rate lower? Lots

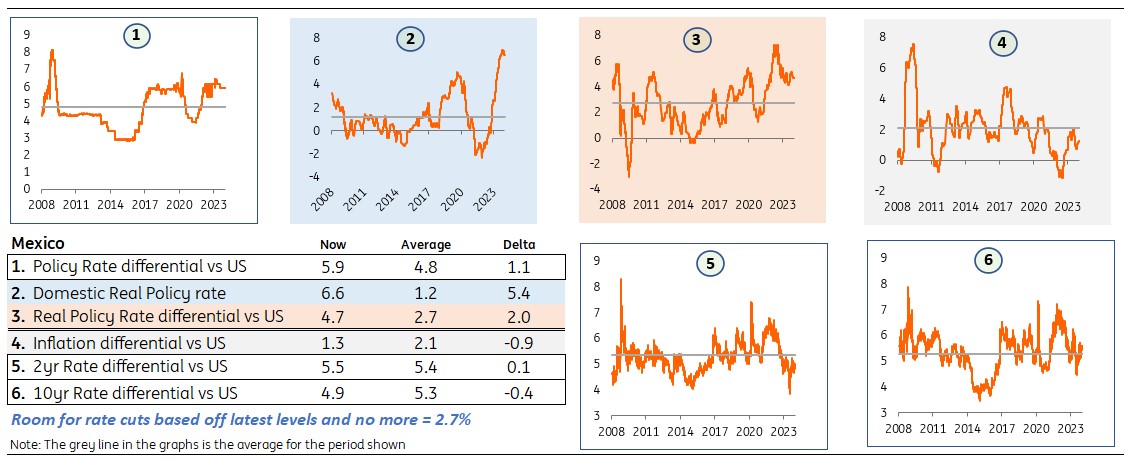

Let’s start with a simple question – how much room does Mexico's central bank (Banxico) have for policy rate cuts? We answer this question in two phases. First, we assess what room Banxico has based purely off where we are now. So, no forecasting; simply a purely technical and steady state analysis.

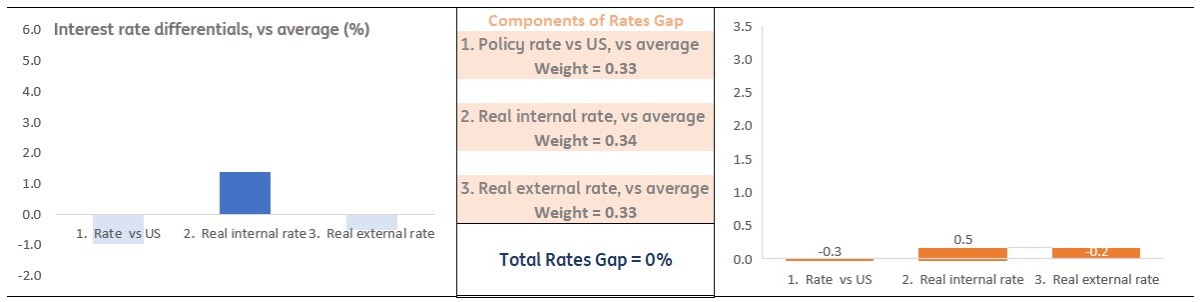

We use three ingredients to help identify room for a policy rate manoeuvre:

- The classic nominal official rate differential versus the Federal Reserve is always important. It’s the spread that the markets focus on, and it’s the one that directs FX forwards.

- The internal real rate is the domestic policy rate less inflation – the real policy rate. It’s the one that affects domestic circumstances.

- The external real rate differential is the domestic real policy rate versus the real Fed funds rate. It’s the link to the currency, control of it, and feedback to domestic inflation.

Inputs to the calculation process for the official rate and market rates

- The classic rate differential is 5.9%, versus a 4.8% average. The delta is 1.1%.

- The internal rate is 6.6%, versus a 1.2% average. The delta is 5.4%.

- The external real rate differential is 4.7%, versus a 2.7% average. The delta is 2.0%.

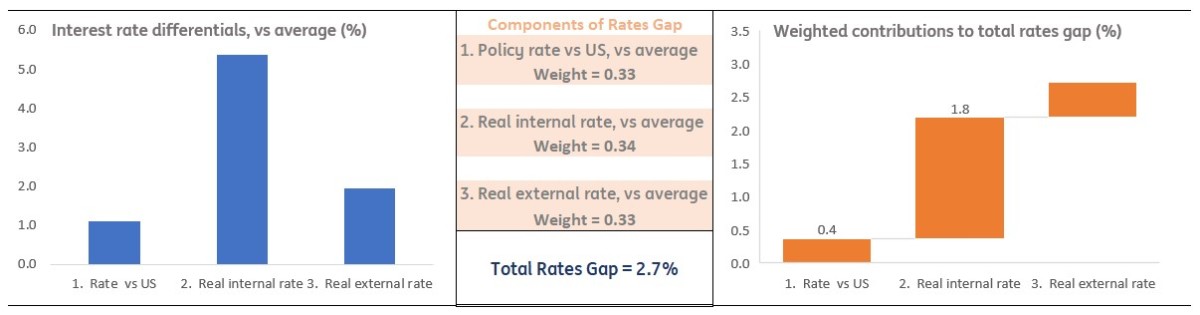

Applying an equal weighting gives us 2.7%. So, Banxico can cut its official rate to 8.5% from the current 11.25%. Remember, this is a steady state analysis based off where we’ve been and where we are now, and no more.

Here’s how we calculate rate-cut potential for Banxico based off a steady state

(no forecasts of the future, purposely)

One issue here is the policy rate differential vs the US would now be 1.7pp (percentage points) below average, and the real external rate is 0.8pp below average. It’s a stretch, but doable for two reasons. First, the absolute policy rate differential is still 3.1% and the absolute real external rate is 1.9%. It’s just the deltas versus average that are negative. Second, they are being cushioned by the real internal rate being at 2.6pp above average.

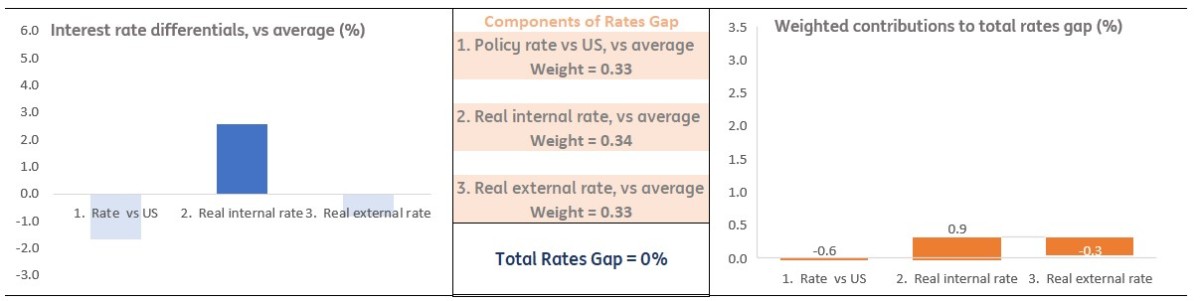

As can be seen in the graph below – with Banxico at 8.5% and no other changes – the rates gap is now zero, and thus any further cuts would be an overshoot to the downside.

Let’s pause here to comment on the upcoming policy meetings.

Banxico has been cautious, as is typical. One issue they've been grappling with is the size of the fiscal deficit. And there has been a degree of inertia to their thinking, supported by a lack of huge macro pressure to cut and rewarded with a firm MXN. But macro pressures can build, especially as domestic demand comes off highs hit in 2023.

Our analysis shows there is no material constraint to delivering a cut at the next policy meeting set for 8 February – apart from the Banxico conservatism. If there is a skip there (as seems likely), a 25bp cut from the 26 March meeting is highly probable in our view.

If we have to wait till the 9 May meeting for a first cut, it might as well be a 50bp cut at that juncture. Once Banxico gets going, rate cuts can become the norm from most subsequent policy meetings.

Imagine a world where Banxico is at 8.5%, and we add some future dynamics. What then?

Now, let’s take things one step forward. Imagine a world where Banxico does now pitch its policy rate at 8.5%. And in addition, Mexican inflation falls to 4%, the Fed cuts by 2.5%, and US inflation falls by 1%. Then we’d have the following:

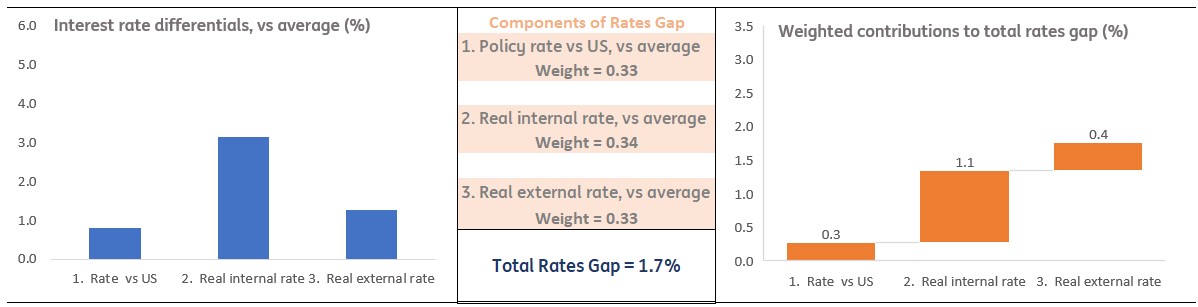

Now, we’d have i) the classic rate differential at 0.8% above average, ii) the internal rate 3.2% above average, and iii) the external real rate differential 1.3% above average. In other words, an interest rate gap has re-opened for Banxico.

Applying equal weighting gives us 1.9% for that gap. So, Banxico can cut its official rate to 6.7%. What does this world look like? Here it is:

The real Banxico policy rate is cushioning the external differentials, neither of which are significantly deviated from historical averages. And here, Banxico is at 6.7%, Mexican inflation is 4%. US inflation is at 2.4%, and the Fed funds rate is at 2.75-3.0%. Nothing is very stretched.

That does not mean Banxico cannot cut further. It just means it would be overshooting to the downside relative to implied constraints set by historical averages (which can change).

And finally on this, we’re not suggesting that Banxico will deliver chunky one-off cuts. Over the course of 18 months starting, say, in March, a mix of 25bp and 50bp cuts would take the policy rate down from 11.25% to 6.70% (the straight average is 35bp per meeting). More 50bp cuts and we catch up and get there quicker.

Market rates are already pricing a lot, but have room to fall, and for the curve to steepen

What does all of this mean for market rates? Currently, the 10yr spread to the US is some 40bp rich to the average, and the 2yr is only 10bp cheap to the average. Both are tight relative to the policy rate spread, indicative of market anticipation of rate cuts.

That said, these 2yr and 10yr spreads are not statistically deviant from averages, nor overstretched. The 10yr standard deviation vs average is some 60bp while the 2yr is 75bp, and current spreads are within those standard deviations. Spreads too have been lower historically, so they don't need to be floored at the average.

If the rate cut potential identified is realised, there should be room for the 2yr and 10yr spreads to achieve spreads that are two standard deviations away from the mean. To the downside, rate cuts are typically sentiment bullish and generate overshoots. That would target a spread to the US of 3.9% for the 2yr and 4.1% for the 10yr. That implies a convergence of 160bp in the 2yr and 80bp in the 10yr without overreaching.

And what about the FX angle? We argue that this is self-contained in the rates differential(s) identified, and especially the external real policy rate differential versus the US. USD/MXN is now in the 17.2 area and the forwards see it at 18.5 on an 18-month view. That’s the degree of MXN depreciation that should (theoretically) be tolerated by Banxico. The long-run averages as identified set floors below which FX vulnerability can arise. Our FX strategists in fact identify MXN strength as a feature in the coming months. See more here. That supports cuts.

If the stars align, Banxico has room for 4.5% of rate cuts through 2024/25

Bottom line, there’s a value trade to be played in Mexico where positioning for lower market rates and a steeper curve have identified alpha worth pursuing. We identify two elements here. First is a steady state where we identify room for Banxico to cut by 2.3%. The second is the realisation of inflation and Fed cut expectations, which paves a path for Banxico to get to 7%. And that’s without stretching from historical averages. So, Banxico could go lower.

Finally, you might be wondering what the steady state rate cut manoeuvre looks like for other centres. For Brazil it’s only 25bp (yes, small). For Chile it’s 1.7%. And for Colombia it’s 1.9%. Hence, Mexico scores best on a steady state. We’ll cover Brazil in detail next – stay tuned!

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more