World trade: from boom to bust

Trade growth looks set to almost halve in 2018 to 2.6% and could drop to 1.3% in 2019, the lowest level since the trade collapse of 2009. The current trade conflict is one of the reasons, but there’s more going on

Fig 1: Growth of world trade in goods 2006- 2018 and 3 scenarios for 2019, (%)

2018: Protectionism kicks in slowly

The global economy is flourishing. ING expects 3.9% GDP growth for 2018, significantly higher than 2017. But this positive development has failed to translate into an acceleration of trade growth. On the contrary, the average monthly growth rate for world trade in the first half of this year has been just 0.07%, a fifth of the average monthly rate in 2017.

Trade war

Given all the attention on President Trump's stance on trade, you could be forgiven for thinking that US protectionist measures and the retaliation of the country's trade partners are the main reason for the setback in the global trade in goods but these measures apply to no more than 0.4% of world trade and were only imposed from the end of March; around half came into effect in June.

Of course, there are spillover effects from rising tariffs due to cross-border supply chains. Based on external research and ING’s calculations, we estimate that the total effect of these elevated tariffs, including spillover effects, is two to three times higher than the direct impact on trade. This brings the impact of the tariff hikes for the first six months of this year to around -0.1%, which is rather small.

Slowdown of manufacturing

If the direct effect of trade protectionism explains only a small part of the total decline in trade growth during the first half of 2018, what else is going on? Well, industrial production growth, which is much more correlated with trade than GDP, has been slowing down. In 2017, industrial production grew 0.3% per month, on average. During the first half of 2018, this growth rate was cut in half.

It is possible that the trade conflict partially explains the lower growth for industry. In the eurozone, indicators of business confidence have deteriorated since the start of the trade tensions in 1Q. Returns on investment in traded goods have become less certain as tariffs lead to higher prices, which reduce demand. Alternatively, if exporting companies compensate for tariffs by lowering prices, it affects profit margins. Companies with plans to start exporting to the US might have put these plans on hold until there is more certainty about the outcome of the trade dispute.

The slowdown in industry, especially manufacturing, weighs on trade growth because industrial goods make up almost 70% of world trade. The slowdown is mainly driven by advanced economies that are, on average, more trade intensive than emerging economies; the decline of industrial production in the EU, in particular, hurts trade. The EU is the largest trader in the world, not only because of the size of its economy but also because EU economies are relatively trade-intensive. Japan also saw industrial production decline in 1H2018.

What to expect for 2H 2018?

Although the preliminary trade figure for July was upbeat (1.1% month-on-month growth), we don’t consider this to be a sign of recovery because we don’t expect much support from the manufacturing cycle in the last five months of the year. Global manufacturing PMI scores have become less positive since the start of the year (fig. 2). We assume that industrial production will deliver the same growth rate as during the first six months of this year, suggesting a 2.7% rate for 2018 overall. Since 2012, yearly world trade growth (measured by world imports) has grown 1.1 times faster than industrial production, on average, implying that global trade will grow by 3% in 2018.

Fig 2: Global PMI Manufacturing

While the growth of industrial production is pushing up trade in 2H 2018, spillover effects from the trade conflict are at play as well. And they will increase during the second half of this year.

The US administration has imposed a 10% higher tariff on $200 billion of imports from China on top of the $34 and $16 billion that were already subject to higher tariffs since the beginning of July. China has taken retaliatory measures.

The recent escalation of the trade conflict between the US and China means that 2 to 2.5% of world goods' trade are now subject to higher duties. We calculate a negative effect on world trade of 0.4%, both from the direct effects of higher tariffs and spillover effects to other products because of global value chains.

The positive effect of growth in industrial production together with the negative effect of higher tariffs suggests world trade will grow by 2.6% this year. This is significantly lower than the 4.5% trade growth for 2017 and is at odds with the acceleration of world GDP growth since 2017.

Outlook for 2019: Trump will step up trade war with China

We forecast a weak year for trade in 2019. Global GDP growth is expected to have peaked. We forecast a slowdown from 3.9% this year to 3.6% next.

Since 2012, industrial production has grown by a little less than 60% of world GDP growth, on average. So normally, industrial growth should be 2.1%. This implies 2.3% growth of world trade in 2019.

But, just as in 2018, next year will not be a normal one for trade. The effects of the trade conflict are increasingly kicking in and a further escalation seems to be ahead. The severity of the dispute depends on the approach of the US administration. As long as US Congress doesn’t interfere, we expect President Trump to continue putting pressure on US trading partners by raising tariffs. Nevertheless, the result of the mid-term elections could influence the president's approach. We see three scenarios.

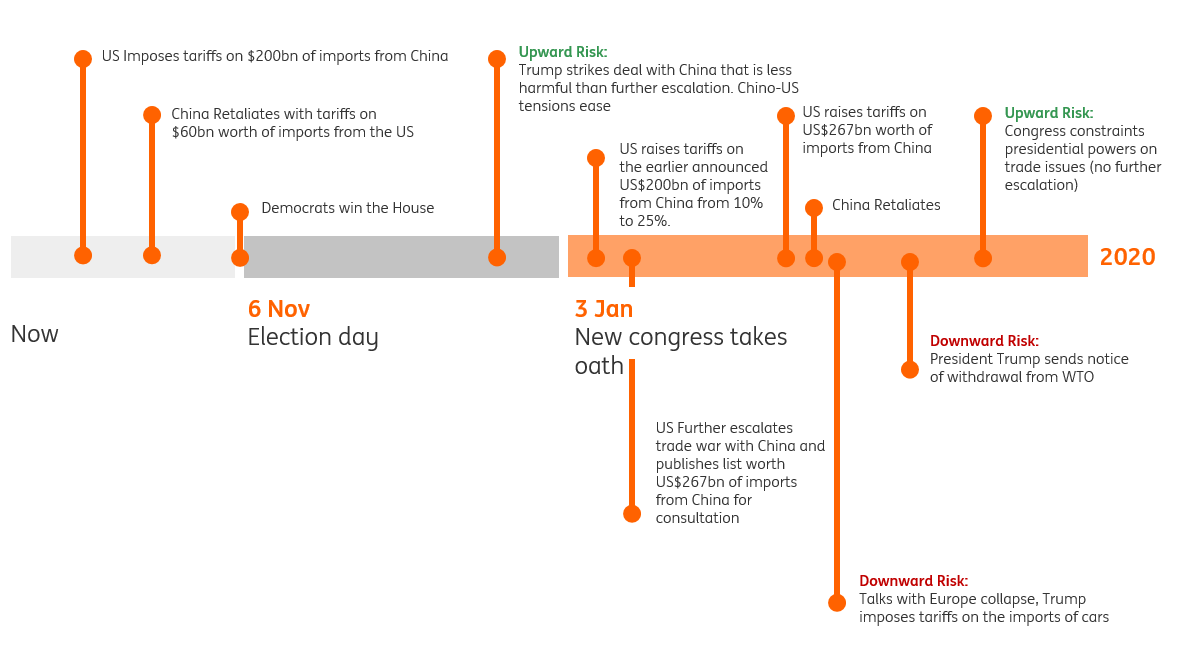

Fig 3: Timeline (click to enlarge)

Base case scenario

In our base scenario, we assume that after the mid-term elections, independent of the result, the president wants to show the electorate that he continues to work on his election promise to change the terms of trade for the US, but he will focus his attacks mainly on China.

We think the Republicans will lose the majority in the House of Representatives. In this scenario, we assume the Democrats will not support a trade war with traditional allies such as the EU and that a withdrawal from the WTO is not likely to get a lot of support from Democrats either. Trump could encounter more resistance from Congress to his trade policy than he has up until now but we do expect that Congress will agree to the overhaul of Nafta.

We assume that a majority in Congress will not seek new legislation to take away the president's discretionary powers as long as Trump focuses on trade with China. We currently don’t see any sign of a compromise between the US and China and expect the dispute to escalate well into 2019. In our base case, the US-administration will raise tariffs on $200 billion of goods from China from the current 10% to 25% in 1Q 2019. And, because we think China is not going to give in (enough) to Trump's demands, we foresee the president following up on his threat to hike tariffs on the remaining $267 billion of US imports of Chinese goods that have not yet been hit by tariff rises (implementation in 2Q). We assume a tariff hike of 10%.

China will retaliate by putting a 10% tariff on the $20 billion of imports from the US that have not been hit by higher duties. It's possible that China will increase non-tariff barriers to come closer to equalising the US policy step. But unfortunately, we cannot quantify non-tariff barriers in value, meaning that we cannot calculate the effect of these kinds of steps on world trade.

The conflict between the US and the EU is on hold and given the fact that President Trump could use some support from the EU in his fight with China, and in his attempt to reform the WTO, he has a motive to take a step back in his fight with Europe. An escalation of the conflict with the EU is a risk but not part of our base case.

In this base case, the trade dispute will affect approximately 4% to 5% of world trade by the end of 2019. The downward effect of the tariffs on world trade will be a little over 0.4 percentage points, twice the direct effect of tariffs in 2018. Including the indirect effect through global value chains and the continuation of the negative structural trend at the pace of 2018, the trade conflict has a downward effect on trade growth of -1 percentage point. Taking into account the positive impulse from the growth of industrial production, trade growth in 2019 will be 1.3%, the lowest growth since the collapse of world trade in 2009.

Downward scenario

In the downward scenario, the trade dispute escalates more acutely. Not only does the conflict with China escalate, but talks with the EU yield no results. This would mean that in the third quarter, the president imposes a 25% tariff on automobile imports from the EU and the rest of the world worth $265 billion. Most trade partners would retaliate in kind; we assume up to a level of 75% ($200 billion).

In this scenario, Congress does not or cannot restrain Trump from raising tariffs on foreign cars. These developments would bring the negative effect of tariffs to -1.8 percentage points. If we take the positive influence of the cycle into account, growth of world trade slows to just 0.5% in 2019.

In this downside risk scenario, the percentage of world trade that is directly affected by the trade conflict is 8%, though ultimately, a quarter of world trade is affected. And this potentially increases if the US were to step out of the WTO. However, we think the US administration is likely to give WTO reform a chance for at least half a year. Given the six months notice period, the potential effects on tariffs from a WTO withdrawal would not kick in before 2020.

Upward scenario

We see two possible upward risks for world trade. The first is that we assume that Congress passes legislation that makes it possible to undo the tariff measures taken by the president. But it could take quite some time for such a law to be drawn up and be put into practice. We assume that undoing the tariff hikes by Trump could only become effective in 2020 meaning that they will stay in place in 2019.

The other upward risk is a deal between China and the US, which cannot be ruled out. Since President Trump decided earlier this year that reducing the trade deficit by a fifth was not enough (China offered to import an additional $70 billion of American goods and commodities), a potential deal has to be more advantageous for the US to get the president to agree. Trump has demanded that the trade deficit be cut in half by 2020, implying a reduction of $190 billion.

In this upward scenario, we assume that the US and China meet each other halfway, reducing the US trade deficit with China by $130 billion. This would be made up of $65 billion in Chinese imports of US goods and a voluntary export restraint by China of $65 billion and we think a deal could be agreed before the end of 2018. In that case, the net effect on world trade is zero, but undoing the damage of the earlier imposed tariffs for US-China trade would be an impulse for trade in 2019 of +0.1%. We assume that the US steel and aluminium tariffs continue (just as in the deal with Mexico) along with retaliatory effects.

Taking into account the (in this case positive) spillover through value chains and the negative carry over from 2018 of the tariffs on US imports from other countries, the net effect of these two things is a positive for world trade of 0.25%. Together with the positive impulse on trade from the cycle, trade growth in 2019 would be 2.6% in this scenario.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Trade warsDownload

Download article

8 October 2018

In case you missed it: A war of words This bundle contains 9 Articles