Warning signs for Europe’s north

Labour cost competitiveness has been shifting within the eurozone as the south has gained and the north has lost competitiveness. A strong feat for southern economies, but this does raise questions about the north’s export-led growth model

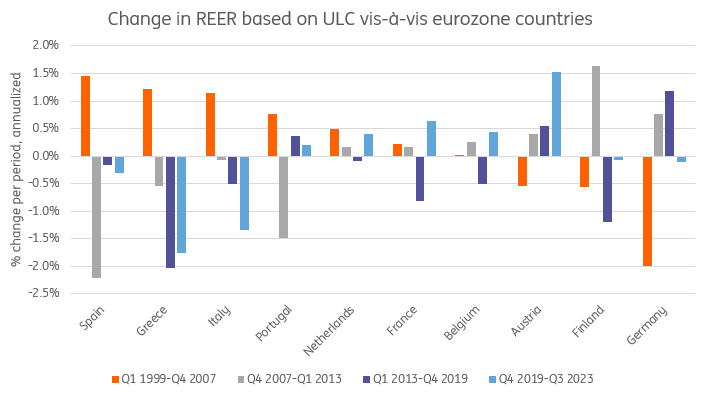

Labour cost competitiveness continues to converge within the eurozone

As the euro celebrates its 25-year anniversary, labour cost competitiveness has gone through significant swings. In the first ten years, southern European economies in particular lost competitiveness, while northern European economies led by Germany saw a sharp improvement. This divergence in (cost and price) competitiveness saw its sad climax with the European sovereign debt crisis – a crisis that Europe tried to cure with austerity measures and reforms to improve competitiveness. While the former led to questionable results, the latter has started to bear fruit, and the overall result has been one of regained internal competitiveness.

To assess labour cost competitiveness, we look at the European Commission’s real effective exchange rates (REER) based on unit labour costs vis-à-vis other eurozone economies. This shows relative competitiveness within the eurozone. In the past four years, Austria, France, Belgium and the Netherlands have seen labour competitiveness deteriorate on average, while Germany’s performance was almost stable. The countries that have seen improvements were Italy, Spain, Greece and Ireland [1].

This is no surprise, and is the continuation of a longer trend that started with – or slightly after – the euro crisis. In the years leading up to the euro crisis, unit labour costs had worsened quickly in the ‘periphery’, which resulted in a structurally weak competitive position. During the euro crisis, southern eurozone countries embarked on a forced, painful process of internal devaluation. For most countries, this resulted in prolonged recessions and long-standing high unemployment. While we wouldn’t argue that this is a preferable remedy for structurally problematic countries, the result was there in the end. The big gaps that had opened up in relative unit labour costs before the euro crisis have been closed.

Northern economies also experienced faster wage growth, while productivity growth weakened materially. The faster wage growth helped domestic demand – but thanks to the drop in productivity growth, this also had a material impact on unit labour costs which started to rise. Sure enough, this helped foster a rebalancing within the eurozone when it came to labour competitiveness, as northern eurozone economies allowed southern eurozone markets to catch up.

[1] For Ireland, the strong performance since 2015 also has to do with multinational accounting activity, which distorts productivity figures. In this note, we therefore do not focus too much on the Irish performance.

Relative competitiveness has shown a longer trend of rebalancing

Healthy for the eurozone, but worries about northern growth models emerge

From the perspective of imbalances in the eurozone, most of this is good news. The export powerhouses of the north have been outpaced in recent years by other countries playing catch up. Not in absolute terms, but the pace of export growth in Germany and Netherlands has been slower than that of Spain, Portugal, Greece and Italy. Industrial companies in the south are more upbeat about their competitive position and have seen export growth improve.

Some of the macro imbalances that the European Commission worries about are addressed by these developments, likely leading to a more even performance between countries. At the same time, it would have been better had productivity performance in the north held up – the adjustment would have come mostly from faster wage growth in the north, as well as faster productivity growth in the south. At this point, it feels more like a race to the bottom in terms of structural performance, which doesn’t help European competitiveness at a global scale.

Germany is already dubbed the sick man of Europe again. Worries about labour cost competitiveness add to a list of concerns about its growth model. For other northern countries, lost labour cost competitiveness serves more as a wakeup call: some rebalancing towards a more domestic demand driven economy is probably healthy, but watch your productivity performance while wage growth increases.

To read the longer original report, click here

Download

Download article

11 April 2024

ING Monthly: Hello, hello, hello, how low? This bundle contains {bundle_entries}{/bundle_entries} articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more