How northern Europe quietly lost its labour competitiveness

The end of wage moderation and deteriorating productivity growth in northern European countries, along with structural reforms in southern ones, have allowed competitiveness convergence in the eurozone. This healthy rebalancing perspective adds to questions about export-led growth models

Labour cost competitiveness continues to converge within the eurozone

Competitiveness has been a regular topic since the start of Europe's monetary union. In the early 2000s, the infamous Lisbon strategy aimed to make the European Union the most competitive region of the global economy. Almost ten years later, Southern European economies, in particular, had significantly lost competitiveness, while Northern European economies led by Germany had seen a sharp improvement. This divergence in (cost and price) competitiveness saw its sad climax with the European sovereign debt crisis, a crisis that Europe tried to cure with austerity measures and reforms to improve competitiveness. While the former led to questionable results, the latter has started to bear fruit, and the overall result has been one of regained internal competitiveness.

Of course, there is much more to European competitiveness than just price and cost competitiveness. Think of energy prices, geopolitical uncertainty, red tape, tax regimes, infrastructure, education, the share of industry or services in the economy or simply put, the economic business model of a country, just to name a few. However, relative unit labour costs have proven to be an important indicator of a country’s cost competitiveness. Over the last couple of years, the inflation peak and continuing labour shortages have caused wage growth to take flight while productivity stumbled. We see that this plays more in northern than southern eurozone markets, as you can see below.

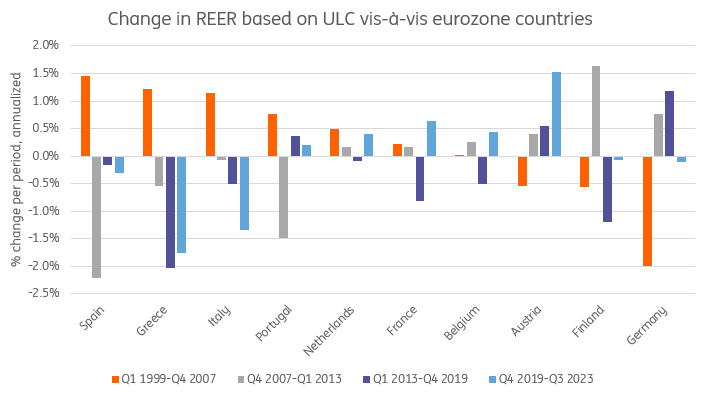

Relative competitiveness rebalancing within the eurozone since the start of the pandemic

To assess labour cost competitiveness, we look at the European Commission’s real effective exchange rates (REER) based on unit labour costs vis-à-vis other eurozone economies. This shows relative competitiveness within the eurozone. In the past four years, Austria, France, Belgium and the Netherlands have seen labour competitiveness deteriorate on average, while Germany’s performance was almost stable. The countries that have seen improvements were Italy, Spain, Greece and Ireland[1].

The gaps in relative unit labour costs before the euro crisis have closed

This is no surprise and the continuation of a longer trend that started with or slightly after the euro crisis. In the years leading up to that crisis, unit labour costs had worsened quickly in the ‘periphery’, which resulted in a structurally weak competitive position. During the crisis, southern eurozone countries embarked on a forced, painful process of internal devaluation. For most countries, this resulted in prolonged recessions and high unemployment. While we wouldn’t argue that this is a preferable remedy for structurally problematic countries, the result was there in the end. The big gaps that had opened up in relative unit labour costs before the euro crisis have been closed.

To zoom in, we also use our own calculations of unit labour costs based on labour compensation per hour and value-added per hour. This way, we can break down the developments in labour cost competitiveness to see what has driven the internal adjustments in the eurozone.

[1] For Ireland, the strong performance since 2015 also has to do with multinational accounting activity, which distorts productivity figures. In this note, we therefore do not focus too much on the Irish performance.

How northern Europe has started to lose its competitive edge

The first decade of the common currency was marked by large capital inflows to the ‘periphery’, which resulted in relatively unproductive investments. Productivity growth was practically non-existent in Italy and Spain, while wages grew as fast or faster than in most northern European countries. Greece saw significant productivity growth but actually experienced such high wage growth that productivity gains were nullified. This caused sizeable gaps in unit labour cost development with other eurozone economies.

Relative competitiveness has shown a longer trend of rebalancing

As the chart below shows, northern European countries experienced above-average productivity growth and wage moderation to various degrees. Successful export nations like Germany and the Netherlands drew criticism for running high trade surpluses while limiting domestic demand because of this, making it harder for southern eurozone economies to adjust.

Weak productivity growth in the past decade has worsened unit labour cost developments

In the 2010s, wage growth dropped markedly in Spain, Portugal and Italy and was even negative in Greece. Productivity growth slowed in most of the eurozone during this period of weak investment, but Spain and Portugal managed to have stronger productivity growth than the eurozone average for this period. The painful adjustment was paying off. Also, northern economies experienced faster wage growth while productivity growth weakened materially. The faster wage growth helped domestic demand, but thanks to the drop in productivity growth, this also had a material impact on unit labour costs, which started to rise. Indeed, this helped a rebalancing within the eurozone when it comes to labour competitiveness as northern eurozone economies allowed southern eurozone markets to catch up.

The post-pandemic period accelerated the process of increasing unit labour costs

The post-pandemic period even accelerated the process of increasing unit labour costs for northern eurozone economies. Then again, this also happened in southern eurozone countries though as most countries have seen wage growth shoot up thanks to high inflation rates and tight labour markets, while productivity growth has become negative for most large eurozone economies. The negative productivity developments have been another step down from the already very weak growth seen on average in the pre-pandemic period. Overall, here we also note that competitiveness in northern eurozone countries still deteriorated on average.

That process has been so significant that the Netherlands and Austria are now the countries which have seen their labour cost competitiveness deteriorate the most since the beginning of the eurozone in 1999 out of the original 12 euro countries (without Luxembourg, with its over-sized financial sector an odd one out). Ireland and Greece, having seen their real effective exchange rate deteriorate most of all countries around 2010 are now the countries with the lowest reading.

Export growth in northern eurozone markets has been outpaced by the south

The loss of northern eurozone competitiveness has not only occurred vis-a-vis southern eurozone markets in the post-pandemic period. Using a real effective exchange rate based on unit labour costs vis-à-vis a broader group of 37 trading partners as opposed to just the eurozone countries, we find that the northern eurozone economies have recently lost labour competitiveness at a slightly faster pace against external partners.

The loss of northern labour cost competitiveness is not just within the eurozone

Because of this, it is sensible that businesses in the manufacturing sector are downbeat in northern eurozone countries. When looking at which manufacturing companies are more positive about their competitive position in the EU, Germany, Austria, Belgium, and Finland trail the rest of the eurozone. This is not strange, given the fact that the broader weakness in competitiveness is accompanied by weaker export growth.

The export powerhouses of the north have been outpaced in recent years by other countries playing catch up. Not in absolute terms, but the pace of export growth in Germany and the Netherlands has been slower than that of Spain, Portugal, Greece and Italy. Industrial companies in the south are more upbeat about their competitive position and have seen export growth improve.

Actual export performance has been better in southern eurozone in recent years

Investments since the start of the pandemic follow a similar pattern. Investments in capital can boost productivity performances, which is vital given the dire developments in productivity in recent years. Also here, massive investment growth is seen in some of the original periphery countries. Spain is the exception and Italy is distorted by the ‘superbonus’, a government incentive scheme which has boosted housing investment.

Still, with the EU recovery and resilience fund on track to see investment flow into southern economies at a fast pace in 2024-26, capital investments are favouring southern eurozone countries at the moment. At the same time, northern countries are still better equipped to absorb digital and technological innovations.

Investment growth since the start of the pandemic has been massive in most periphery markets

Healthy for the eurozone, but worries about northern growth models emerge

Most of this is good news from the perspective of imbalances in the eurozone. These developments address some of the macro imbalances that the European Commission worries about, likely leading to a more even performance between countries. At the same time, it would have been better had productivity performance in the north held up, and the adjustment would have come mostly from faster wage growth in the north and faster productivity growth in the south. At this point, it feels more like a race to the bottom in terms of structural performance, which doesn’t help European competitiveness on a global scale.

Germany is already dubbed 'the sick man of Europe' again. Worries about labour cost competitiveness are added to a list of concerns about its growth model. For other northern countries, lost labour cost competitiveness serves more as a wakeup call: some rebalancing towards a more domestic demand-driven economy is probably healthy, but watch your productivity performance while wage growth increases.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more