THINK Ahead: From ‘loads of money’ to no cash to splash

Harry Enfield’s ‘Loadsamoney’ mocked 80s yuppie excess; his catchphrase rang out across the UK. Today, there’s no cash to splash, and not just in Britain… high household savings ratios will struggle to spare Europe from an energy-led slowdown.

Plus, the confirmation hearing of Fed Chair nominee Kevin Warsh. All to look forward to next week

No cash to splash

Plenty of ink has been spilt on how this crisis differs from the 2022 energy shock. And mostly, not in a good way.Cooler job markets, less government stimulus, and tighter monetary policy all make the economy more vulnerable. And that means inflation is less likely to take hold in the long term.

But there’s one area that looks more positive: European savings.

The savings ratio - the proportion of income not spent on goods and services – has been consistently above its pre-Covid average. Admittedly, not in the US. But in the eurozone, where this energy shock will be felt more acutely, it’s comparable to levels in February 2022. And in the UK, it is considerably higher (or is it? More on that later…).

Household savings ratios are above-average in Europe

That matters because, at face value, it offers households a cushion against higher energy prices. Real incomes are set to fall as inflation heads to 4% and wage growth languishes at 2.5% in the eurozone and 3.5% in the UK. Even if you’re an optimist and think wages will rise with prices (we don’t!), this will take time. Continental Europe’s system of collective bargaining means pay responds with a lag while new settlements are negotiated.

So, if disposable incomes are down, then that savings ratio is going to have to fall if a consumer-led recession is to be prevented. The fact that the savings ratio comes from a higher starting point should offer more scope for that to happen.

And we do indeed expect it to fall, at least temporarily. It’s what we saw back in 2022 as households engage in what we economists call “consumption smoothing”. Cut savings in the bad times, rebuild them in the good. That might help explain that savings ratio trend over the past few years.

However, I think there are a number of holes in this story:

For starters, are households really going to be willing to part with their cash at a time of such uncertainty, to the extent that saving is a choice? It feels unlikely. My colleague Peter Vanden Houte points to the March uptick in eurozone unemployment expectations as one reason for caution.

And is the savings ratio really a reliable measure in the first place? I’ve always been a bit sceptical because frankly, it isn’t actually measured at all.

Put simply, it’s the gap between a broad definition of income after taxes and household consumption. That sounds sensible enough, until you remember both of those numbers are calculated independently of one another, using different data sources and in complex methods. And because “savings” here is simply a residual between two very large numbers, it is subject to often huge revisions if one or both of those figures are updated.

Case in point: when the data first came out, it showed Britain’s savings ratio at 9% as of Q3 2022. Data for that very same period has since been revised down to 5%. Pretty different, wouldn’t you say?

The good news is we have a much better way of measuring all this. Central banks provide data on actual money in actual real-life bank accounts. The bad news? No big war chest of cash waiting to be splashed…

Adjusted for inflation, the stock of savings sat in European banks is below the pre-Covid trend on both sides of the channel. Likewise, if you look at deposits as a ratio of household disposable incomes. That’s a stark contrast with early 2022, where economies were still lavishing in huge pools of “excess savings” – money squirrelled away when there was nothing to spend it on during the pandemic.

Nominal vs. real household deposits

Then there’s the impact of higher interest rates. The textbooks tell us that they should incentivise saving. Sure enough, eurozone data shows flows into deposit accounts with a fixed maturity nearly perfectly offset outflows from those paying overnight rates back in 2022.

But the textbook has also changed over the past two decades. Savers benefit quickly from higher deposit rates, while mortgage rates, typically fixed well into the future, take much longer to respond. That blunts the negative cash flow impact of tighter monetary policy, at least initially. And let’s face it, the ECB rate hike we’re now forecasting isn’t going to move the needle much anyway.

Finally, we have to remember that the bulk of savings is held by the wealthiest and, therefore, least affected by the cost-of-living crunch. James Knightley points to Fed data, indicating the top 20% of earners hold 70% of savings (or specifically “other assets”, most of which are deposits). Our own European survey shows almost a quarter of households have no savings at all.

All of this matters for the central banks. If the data is right that households don’t have a big wadge of cash under the proverbial mattress – and those that do will be reluctant to spend it – then that’s hardly good news for growth. And it's yet another reason to tread carefully when it comes to hiking interest rates.

James Smith

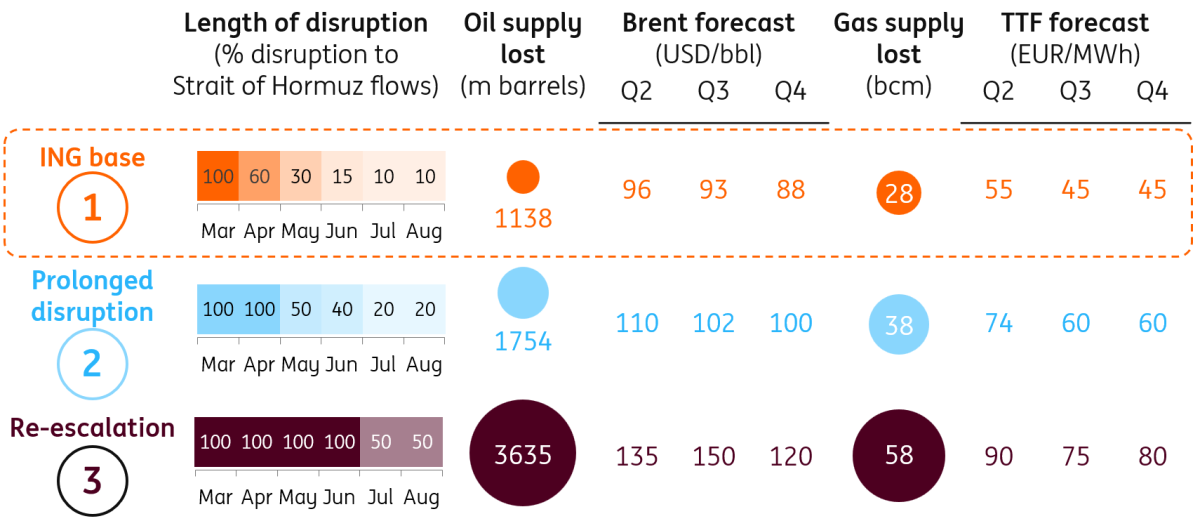

Three scenarios for energy markets

We've refreshed our three scenarios for the Iran crisis and energy markets as part of the ING Monthly published this week. Check out this article for more on what these scenarios mean for the economy and markets.

THINK Ahead in developed markets

United States (James Knightley)

- In a relatively quiet week for data, the focus will remain on US-Iran talks in the hope a deal can be reached that leads to a de-escalation and a re-opening of the Straits of Hormuz. Failure will undoubtedly hit risk assets and prompt a rebound in the dollar as markets price the prospect of higher for longer inflation, weaker growth and the Federal Reserve constrained from cutting interest rates.

- Outside of the data, the Fed has already entered its quiet period ahead of the April 29 FOMC meeting, but it will still be drawing headlines given Kevin Warsh's confirmation hearing to become Federal Reserve Chair is being held on April 21st. Once viewed as a hawk when he previously served as a Fed Governor, he has been nominated by President Trump who has demanded much lower interest rates from current incumbent, Jerome Powell. He will inevitably be questioned on how closely aligned he is with the President's thinking. We imagine he will indicate a belief that, over time, lower interest rates make sense. However, preserving market credibility is of paramount importance and there has to be justification.

- He clearly buys into the idea that tech/AI investment will boost productivity and allow the US to grow faster without generating inflation, and, to be fair, there appears to be support for this view within the broader Fed given at the March forecast update they revised higher their long-run GDP forecast to 2% from 1.8%, without altering the long-term inflation prediction. Whether he will be approved quickly is another matter, given the Department of Justice's probe into Fed construction work overspends. The Senate Banking Committee is comprised of 13 Republicans and 11 Democrats, but Republican Thom Tillis has vowed to block the confirmation until the "vindictive prosecution" of Chair Powell is ended. Until Thom Tillis is satisfied, it will be a 12-12 vote, and it can't proceed to a formal Senate vote.

- In terms of the numbers to watch, March retail sales will be the highlight. We saw a decent increase in unit auto sales in March following weather depressed activity in the first two months of the year, but it will be the higher gasoline price that will really lift the value of sales. Given this situation, we should focus on the core “control” measure that strips out autos, gasoline, building materials and eating out. This tends to better reflect underlying spending trends and a 0.2%MoM gain would fail to keep pace with inflation. This will mean a third consecutive month of weakness in consumer demand in an environment of depressed sentiment and squeezed spending power.

United Kingdom (James Smith)

- Jobs/wages (Tue): Private-sector wage growth is set to continue falling as a fragile jobs market bears down on pay pressure. This is one of the key arguments against rate hikes from the Bank of England

- Inflation (Wed): Predictably, headline inflation is set to nudge higher as the early impacts of the Iran war shine through. Higher petrol and heating oil prices look set to lift headline CPI to 3.3%. It won't be until July when the full effects are felt via the next update in the household energy price cap.

THINK Ahead in Central and Eastern Europe

Poland (Adam Antoniak)

- Mar industry (Mon): We forecast that industrial activity returned to its subdued normal in March, and posted just a slight annual growth despite favourable calendar effects (one more working day). Purchasing managers report soft external demand (poor export orders) and a spike in input prices, most likely linked to the energy crisis triggered by the Middle East conflict. We are likely to see it in PPI numbers as well, and a decline in producers’ prices was probably much shallower last month as prices in refining products soared.

- Mar labour market (Mon): Wages growth eased visibly at the beginning of 2026 amid a lower increase in the statutory minimum wage and less generous hikes in the public sector. Lack of inflationary pressure (apart from unfolding energy shock) curbs wage demand. We expect wage dynamics to converge towards levels consistent CPI at the target. (4-5%). Employment in enterprises remains in decline as some industries face mounting pressure from cheap Chinese imports, and the structure of industrial production and exports is shifting in response to the fact that Poland has become a hub for Asian imports.

- Mar retail (Mon): Consumer demand remains robust and is the main driver of economic growth. The mid-term trend in rising sales of durable goods remains sustained, but recent deterioration in consumer confidence, linked to elevated geopolitical uncertainty (Middle East conflict), may potentially undermine the propensity to spend over the medium term. Still, we forecast that sales in March were strong, even as purchases of petroleum products probably eased towards the end of the month as the government announced measures targeted at reducing gasoline and diesel prices from the beginning of April (maximum price, reductions in excise duty and VAT rate).

Czech Republic (David Havrlant)

- PPI (Mon): Producer prices reflected the surge in oil prices throughout March yet likely remained in an annual decline. Demand from European main trading partners remains lukewarm and puts pressure on margins, so that businesses maintain their price competitiveness, notably in the environment of dumping imports from China. April’s business and consumer sentiment suffered from the havoc in the Middle East, nevertheless both remained relatively upbeat in levels. An increasing unemployment rate may further weigh on consumer sentiment, while the duration of the conflict will shape business mood in line with the assumed damage to the global economy.

Turkey (Muhammet Mercan)

- Rate decision (Wed): The CBT has reiterated in February its commitment to tightening monetary conditions in the event of a marked deterioration in the inflation outlook. In line with this stance, it suspended one‑week repo auctions and allowed the ON rate to rise toward the upper limit of the interest rate corridor following the escalation of the US‑Iran conflict. The subsequent ceasefire, however, brought temporary relief in early April. Losses in the CBT’s foreign exchange reserves have come to a halt, while preliminary data point to an improvement supported by the Bank’s FX swap operations with domestic banks and some reversal in capital flows.

- Against this backdrop, we expect that the CBT will leave both the policy rate and the corridor framework unchanged at the April MPC meeting. Nonetheless, ongoing geopolitical uncertainty may encourage a more cautious approach, potentially leading to an adjustment of the policy rate from 37% toward the current effective funding rate of approximately 40%.

Kazakhstan (Dmitry Dolgin)

- Rate decision (Fri): We expect the National Bank of Kazakhstan (NBK) to keep the base rate unchanged at its 24 April meeting. Recent trends, including a slowdown in CPI to 11.0% YoY in March and a roughly 5% appreciation of the KZT against the USD since the outbreak of the Iran war, suggest some scope for rate cuts over the medium term. For now, however, elevated uncertainty around a potential global inflation shock and higher risk premia argue for caution. In our view, holding rates steady carries a lower risk of a policy mistake than an early cut.

- We have slightly revised up our CPI outlook for the CIS‑4, effectively flattening the expected path of policy easing across the region. For Kazakhstan, arguments against an immediate cut include risk of additional domestic utility tariff hikes and quasi‑fiscal stimulus, both highlighted in the NBK’s previous communication. Strong economic activity and robust bank lending dynamics also suggest there is no urgency to ease policy at this stage.

Key events in developed markets next week

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article