ECB set to signal an ‘insurance’ rate hike

- 16 April

The stagflationary shock induced by the war in the Middle East will slow eurozone growth in the coming months, while inflation will climb towards 4%. Even though the ECB cannot do much to fight a supply shock, an 'insurance' rate hike has become likely to prevent a deterioration in inflation expectations

Slower growth ahead

As the war in the Middle East lingers on and a quick normalisation of energy prices looks unlikely, the stagflationary impact of the crisis is likely to manifest itself in a more pronounced way in the coming months. Before the war, activity data already pointed to a subdued growth profile. Industrial production growth remained subdued in the first two months of the year and eurozone retail sales stagnated. In March, both business and consumer sentiment soured further.

Leading indicators like new orders and hiring intentions in March’s business sentiment indicators foreshadow slower growth in the months ahead. With unemployment expectations rising, we cannot count on a substantial decline in the savings ratio to boost household spending. And while countries like Spain, Italy and Germany have already announced some measures to counter the rise in energy prices, the total stimulus is likely to remain much lower than in 2022-23.

Growth expectations downgraded again

In the ECB’s March staff projections, several scenarios were explored, with the adverse and severe scenarios indicating GDP growth rates of 0.6% and 0.4%, respectively. We are leaning toward the adverse scenario, now forecasting 0.7% growth for 2026, down from 0.9%. Nevertheless, German fiscal stimulus hasn’t vanished and, together with falling energy prices next year, should spark a renewed recovery in 2027. As a result, growth for 2027 is expected to reach 1.3%, slightly less than the prior estimate of 1.4%.

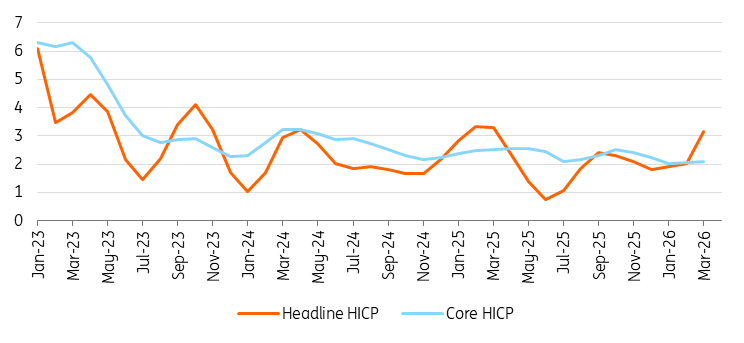

Headline inflation rising, underlying inflation still under control

3M/3M annualised change HICP

Inflation heading towards 4%

HICP inflation climbed to 2.5% in March from 1.9% in February, driven by higher energy costs. Core inflation is still under control for now, with the annualised three-month change in consumer prices excluding energy and food steady at 2%. Still, some secondary inflation effects are likely since businesses are signalling increased selling price expectations in surveys. We anticipate headline inflation rising towards 4% in the coming months, while core inflation is likely to hover between 2.5% and 3.0% in the second half of the year. This should produce an average headline inflation of 3.4% in 2026 and 2.4% in 2027.

An insurance rate hike

Although the ECB currently has limited data to act upon, financial markets expect at least two rate hikes this year. We know that a supply shock is the hardest to tackle for a central bank. As a matter of fact, rate hikes will not boost the crude oil supply.

However, the ECB is unwilling to risk inflation expectations deteriorating as it did in 2022-23. Unlike that period, the deposit rate is now at 2%, compared to -0.5% at the start of 2022. This suggests that a modest rate hike would probably suffice as a signal. Call it an "insurance" rate hike. Could we see two rate increases? It’s possible, but we continue to believe the ECB tightening will fall short of market expectations.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: The world waits for a climbdown

- This bundle contains 13 Articles