Russia: RUB downgraded on oil, but capital account may bring positive surprises

- 13 March 2020

- Russia

We downgrade our year-end ruble expectations from USD/RUB 66.0 to 70.0 on the drop in the oil price. However, some improvement in other balance of payments items, such as non-fuel current account, private capital flows, and FX sales by the central bank on the Sberbank handover may result in RUB outperformance. Near-term volatility to remain high

Downgrading 2020 USD/RUB from 64-68 to 70-72 on revised oil price forecast

Our previous USD/RUB forecast, that suggested a 64-68 range in 2020 with 66.0 at year-end was made under the assumption of Brent staying around US$65/bbl, some pressure on the current account from accelerated imports, and some modest risk-off on the global markets following an extremely successful 2019. Those assumptions are no longer valid. The recent coronavirus outbreak has resulted in a significant deterioration of global risk sentiment, which combined with the breakup in the OPEC+ deal and the resulting drop in the oil price forced the Russian market into the new reality.

ING has downgraded its 2020 average Brent forecast to US$43/bbl, suggesting a drop from US$53/bbl in 1Q20 to US$33/bbl in 2Q20, with some gradual recovery to US$40/bbl in 3Q20 and US$45/bbl in 4Q20.

Even though the fiscal rule has lowered RUB's sensitivity to the oil price fluctuations (as the Ural price dropped below US$42.4, Bank of Russia (CBR) started to conduct sales of FX on the market in the amount of around US$50m per day currently), it did not completely remove the link. The US$22/bbl drop in the oil price assumption for the year requires a downgrade in USDRUB expectations by 4.0 – to 70.0 at year-end. We see 2Q20 as the weakest quarter, with USDRUB bottoming somewhere in the 70-75 range on the likely negative current account surplus amid low oil prices – followed by some recovery.

Lower oil price could be somewhat mitigated by non-oil current account

At the same time, there are several non-oil factors, which may partially mitigate the negative impact of the oil price drop – suggesting some potential for a stronger-than-expected USDRUB.

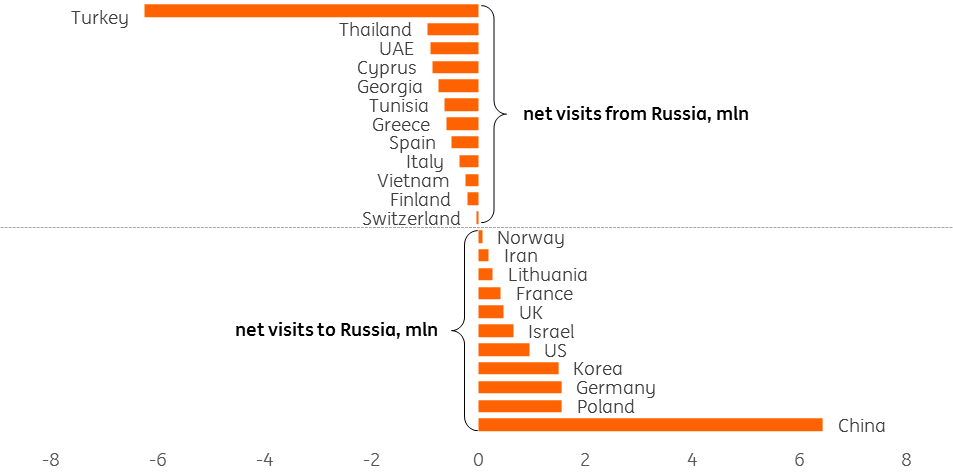

1. The non-oil current account should benefit from the likely lowering in the merchandise imports trajectory, and by improvement in the services balance, as the lack of net visitor inflows from countries blocked by local authorities (they accounted for 12 million net visits in 2019, ie, visits of their citizens into Russia exceeded the number of visits Russian citizens made to those countries) will be offset by a potential reduction in the outward tourism this year on the general coronavirus fear: in 2019, net Russian visits to popular tourist destinations, including Turkey, Thailand, and others totalled also around 12 million last year (see Figure 1).

Figure 1: Foreign travel to shrink both ways

...improvement in the capital account...

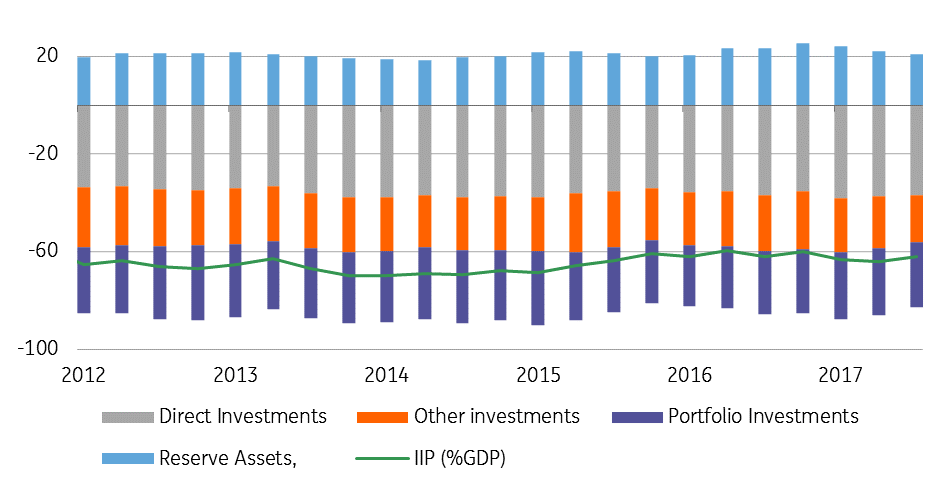

2. The key difference now from the previous crisis episodes (2008 and 2014) is that the Russian capital account is in better shape thanks to higher macro stability indicators, free floating FX regime, more transparent banking system, and higher real rates.

The current market pressure episode has not generated any speculation of capital controls, pressure on the central bank to make certain monetary policy decisions, or any other factors which in the worst case could have increased pressure on the Russian capital account. Outflows so far have been seen only on behalf of foreign portfolio investors into local state bonds (OFZ), which have total holdings of around US$40bn. The outflow is not Russia-specific, and currently ignores the country's macro stability relative to EM peers. Meanwhile local participants, including corporates and private individuals, which had gross foreign assets of US$924bn as of September 2019, have been selling FX at USD/RUB levels of around 70-75. The scope for increased local capital outflow is limited, as foreign liabilities of the real sector have already been reduced vs. 2014, banks are running a net asset position of around US$80bn, while households have accumulated over US$110bn in cash outside Russia (see Figure 2).

If international assets are reduced (out of fear of problems in the EU banking system, other external fears, or as a result of measures by the Russian government/CBR, such as stimulating local lending in FX), that should partially offset the decline in the current account without the need of further USDRUB depreciation.

Figure 2 The risk of higher capital outflow from Russia is now smaller than in 2008 and 2014

...and additional FX sales due to Sberbank handover

3. The upcoming handover of Sberbank from the CBR to the Minfin, which apparently is still on the agenda, will likely result in CBR's FX sales in the amount of US$30bn (lower than the previously expected US$45bn due to the drop in the market price of the 50% equity stake in question), spread over some period of time. Initially this period has been identified at 3-7 years, however we would not exclude a more condensed sale in case of continued turmoil on the local market. This, combined with the aforementioned improvement in the private capital account should lower the importance of current account contraction for the FX market.

As a result, we reiterate our initial call that in case of the oil price stabilizing at around US$35/bbl USDRUB is likely to settle within the 70-75 range in March. We see 1Q20 ending at 70.0, 2Q20 - at 72.0 (assuming Brent averages at US$33/bbl), 3Q20 - at 71.0, and 4Q20 - at 70.0 – reflecting a recovery in oil prices and risk sentiment.

A return to USDRUB65-70 is possible if the capital account shows signs of improvement we mention in this report (optimistic case).

Meanwhile, we remind that with oil prices staying close to the cut-off Urals price of $42.4/bbl, the stabilizing role of the fiscal rule is minimal. This suggests that in the near term the sensitivity of USDRUB to oil price fluctuation will remain close to the pre-fiscal rule period, at USD/RUB 1 move per each US$2-3/bbl move in the oil price.

Volatility on the bond market is also likely to remain high, also reflecting external pressure and the previous heavy positioning in Russian assets. At this point we continue to expect unchanged key rate at the upcoming Bank of Russia meeting on 20 March based on our view on CPI and capital account. However it will take some time before trading on the bond market will return back to fundamentals.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more