Key events in EMEA and Latam next week

- 13 March 2020

- Key Events

A barrage of central bank meetings take place this week and we expect a dovish tone to cushion the Covid-19 impact - though the Russian central bank may go against the tide

Russia's central bank to stand still for now

The main local event for the Russian market will be the central bank’s key rate decision on 20 March. While some market participants are expecting a hike from the current rate of 6.0%, we believe that holding rates steady, rather than hiking by 25 basis points, would be tightening enough. The current turmoil on the local market has been triggered primarily by the oil price shock, channelled through a contraction in the current account, while the capital account doesn’t seem to require additional protection, as:

- Outflows so far have been seen only on behalf of foreign portfolio investors into local state bonds (OFZ), while local participants, including corporates and private individuals have been selling FX assets at USD/RUB levels of around 70-75.

- The Bank of Russia currently has very limited involvement in the FX market, selling around US$50 million per day, suggesting a low risk of strong pressure from speculative capital flows.

- This episode of market volatility has not generated any speculation of capital controls, pressure on the central bank to make certain monetary policy decisions, or any other factors which in the worst case could have increased pressure on the Russian capital account.

- Global central banks are on a downward rate cycle, and Russia’s real rates are already at relatively high levels.

- USD/RUB depreciation seen so far could potentially add 0.5-0.7 percentage points to the year-end CPI, which would still mean 4.2-4.5%, fairly close to the 4.0% target.

As a result, we consider a flat key rate as a base-case scenario, however in the event of further USD/RUB depreciation (regardless of the reason) toward a much less comfortable 80-85 range, the potential inflationary impact could potentially require the Bank of Russia to respond with emergency measures, the list of which includes a higher key rate, more intense FX sales and purchases of OFZ.

The set of economic activity data, also to be released next week, is likely to show some weakness in Russian industry (largely on statistical and weather-related effects) and among consumers (mostly as a result of suspended inward tourism), but this is unlikely to have any material impact on market sentiment.

Turkey: Central Bank of Turkey set to ease some more

Better-than-expected February inflation signals relatively contained underlying price pressures, and a significant decline in oil prices should be supportive for the inflation outlook, which would be a relief for the Central Bank of Turkey. Accordingly, the bank is likely to maintain a dovish bias and announce additional easing, though unease in financial markets, elevated inflation levels and low real rate buffer will keep it cautious. We expect a 25 basis point cut this month.

Poland: Coronavirus impact isn't in the data yet

We think February activity releases (industrial production, retail sales) will not be relevant for the market. The impact of the coronavirus epidemic should be visible from next month. The overall scale of disruption is likely to surprise analysts – presently there are no reliable gauges that can track consumer purchases in real time.

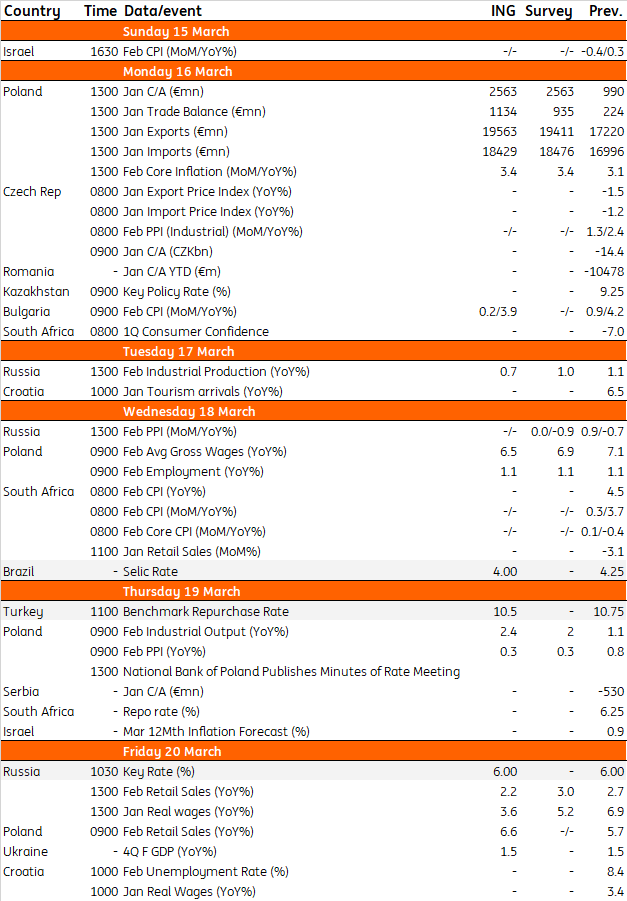

EMEA and Latam Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles