Russia bracing for oil shock: initial thoughts

- 10 March 2020

- Russia

The Russian market is facing volatility, with large fiscal reserves and high real rates coming back into investors' focus, but only after the oil- and corona-related dust settles. With oil at US$35/bbl we expect USD/RUB at 70-75 and a pause in rate cuts. Emergency FX interventions or rate hikes are less likely unless USD/RUB is at 80-85 or weaker

Oil shock incoming

The Russian market is exiting the long weekend (9 March was a day-off related to a public holiday) with the Brent oil price at US$35/bbl, which is US$10-15/bbl lower than last Thursday-Friday, due to the collapse of the OPEC+ deal, which had been limiting global oil supply since 2018. The breakup of the deal was a surprise: even though Russia's reluctance to support OPEC's call to deepen production cuts by 1.5 MMbpd had been consistently articulated since the beginning of Coronavirus oubreak, a number of market participants have still be hoping for an eleventh hour agreement.

The breakup of the OPEC+ deal was a surprise

Moreover, OPEC's reaction to completely abandon the earlier agreements and threaten a ramp-up of production were unexpected. The only possible rationale for the reversal in the OPEC+ approach is to avoid losing market share to the shale oil producers. Based on the OPEC+ outcome, ING has slashed average quarterly Brent forecasts from US$56-65/bbl for 2-4Q20 to US$33-45/bbl.

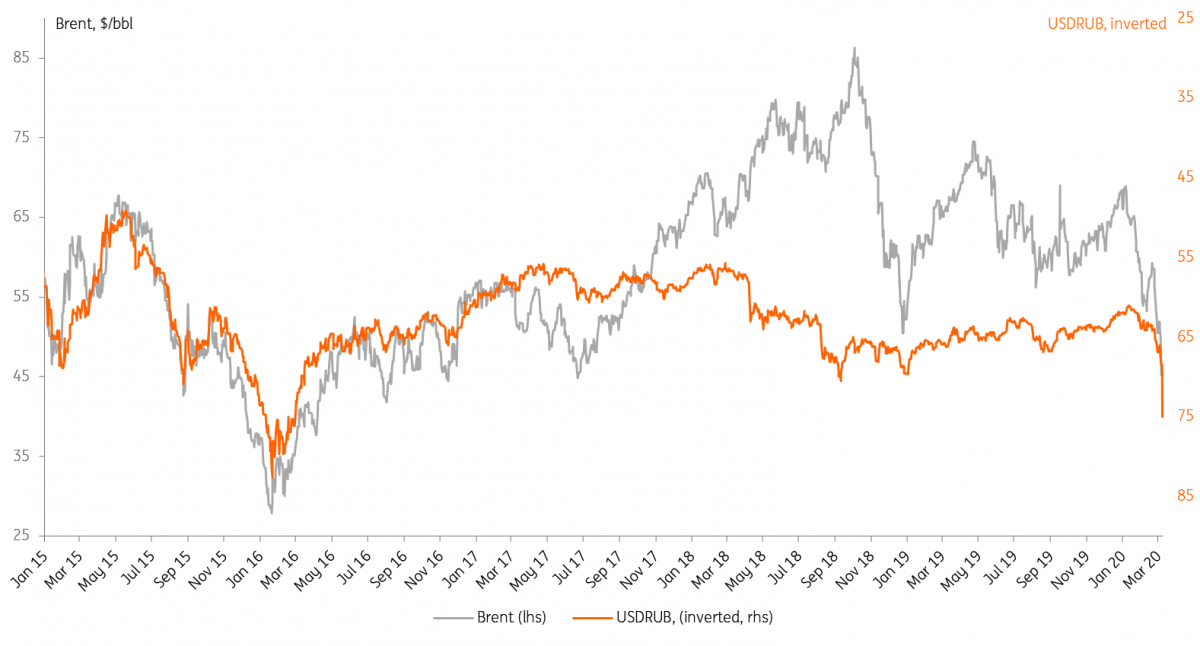

The market has yet to react to the drop in the oil price, however the preliminary OTC trading indicates USD/RUB depreciated to 75.0 (see Figure 1), suggesting an almost 9% depreciation over the weekend and 17% year to date. The Central Bank reacted on Monday by announcing that it will suspend all fiscal-rule related FX purchases for at least 30 days (initially it was supposed to purchase around US$3 bn in March), while the Finance Ministry reminded that at Urals below US$42.4/bbl the fiscal rule dictates FX sales from the sovereign wealth fund. If the oil price settles close to current levels, the Finance Ministry can announce FX sales in the beginning of April, however we would not exclude that the Central Bank could front run the FX sales on the market if conditions deteriorate.

It is obvious that the Russian market is facing a great deal of uncertainty related to future oil prices (the range of market forecasts is wide and includes numbers like US$20/bbl in the worst case) and EM risk volatility related to the still ongoing coronavirus outbreak (virus is spreading globally, EM assets are under continued pressure).

The Russian market is facing a great deal of uncertainty

The spreading of Covid-19, however, seems to be slowing down in China, and fiscal and monetary stimulus worldwide combined with lower oil prices could somewhat mitigate the negative impact on the economy - all of which is clouding our forecasts. In this report we present our intial considerations relevant to the Russian FX and rates market in the near- and medium-term.

Figure 1. USDRUB of 75 under Brent of US$35/bbl is a 4-year low

FX: watch out for interventions and OFZ flows

It remains unclear at this point whether the drop of USDRUB to 75.0 is justified under a Brent price of US$35/bbl. The last time that combination occured was 4 years ago, in February 2016, and since then:

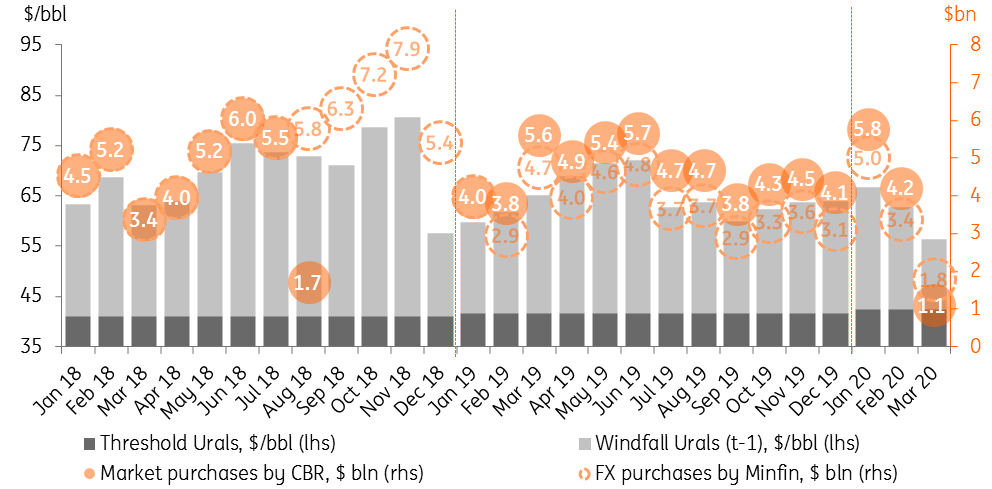

- Russia introduced the fiscal rule, which was supposed to lower RUB's sensitivity to oil price fluctuations through FX purchases/sales under Urals exceeding/underperforming US$40/bbl (2017) and US$42.4 (2020) (see Figure 2).

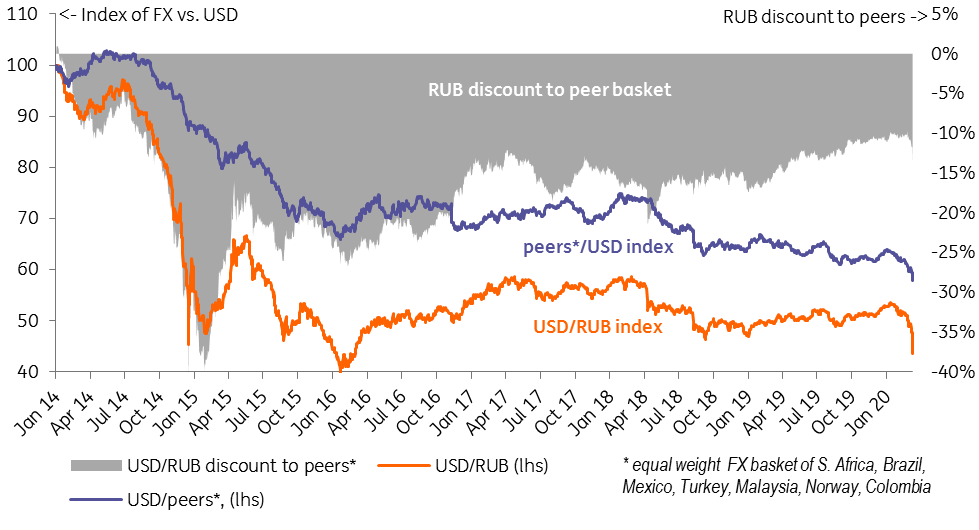

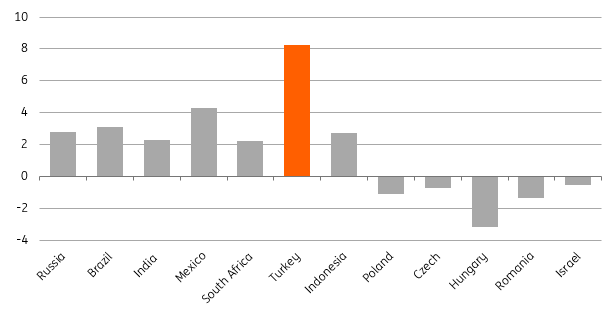

- Foreign policy environment for Russia improved, as sanction risks were lowered, prompting a Russia-specific discount in USD/RUB relative to EM peers shrinking from 25% four years ago to around 10% ahead of the breakup of the OPEC+ deal (see Figure 3). After Monday's RUB collapse this discount recovered to 14%.

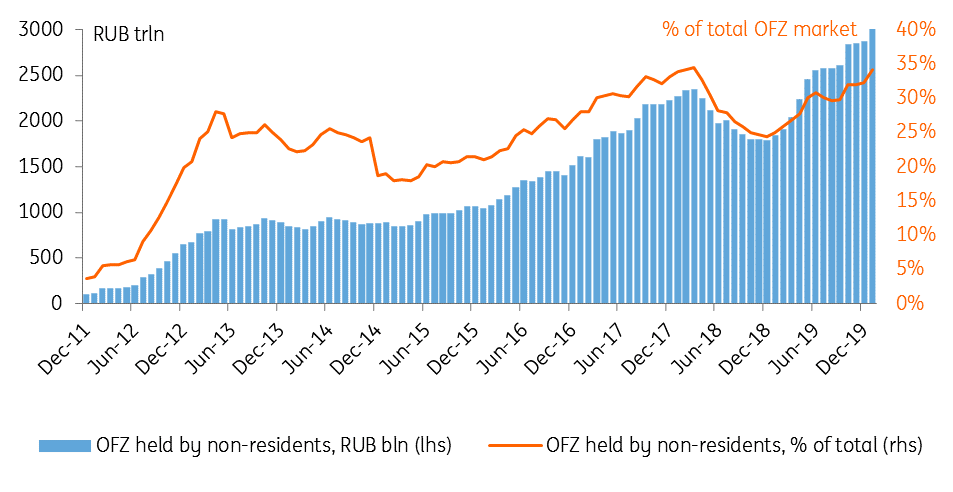

- Lower foreign policy risks combined with a high real rate envoronment made Russia more attractive to portfolio investors, which increased their holdings in local state bonds (OFZ) from RUB1.1 tr (US$14.4 bn under USD/RUB 75.0) in February 2016 to to RUB3.0 tr (US$40.2 bn under USD/RUB 75.0) in the beginning of February 2020, with their share on the total market increasing from 21.5% to 34.1% respectively (see Figure 4).

Meanwhile, in the near-term, this does not protect RUB from volatility or guarantee immediate USD/RUB appreciation from the current weak range of RUB70-75 for the following reasons:

- The Central Bank of Russia's decision to suspend FX purchases seems adequate and resembles the action it took in April-December 2018, however now the effect of that move should be smaller due to the oil price differential: in August-December 2018 the average oil price was around US$70/bbl, and the CBR suspended FX purchases of US$5-8 bn per month (see Figure 2); with the current oil price FX purchases should be zero to slightly negative effective in April. Basically by suspending FX purchases the CBR is front running something that should have happened anyway in a month’s time, unless oil prices recover. Based on the Finance Ministry's statement, if oil prices stabilize at current levels, the fiscal rule would prescribe FX sales of around US$1bn per month (each further US$5/bbl drop would require an extra US$0.7 bn), which is not a large volume.

- The current USD/RUB level is not weak enough to trigger emergency FX interventions by the CBR (unrelated to the fiscal rule), as a) the current oil price is within the CBR's risk scenario assuming average US$25/bbl Urals for 2020, b) the market USDRUB has not deviated materially from the fair value range of 60-70 (historically a deviation of around USDRUB 15 was required), c) attempts to actively prevent USD/RUB depreciation amid the current oil price could result in RUB oil price dropping below RUB2.6k/bbl, which would be the lowest level since 2010 (the 2018-19 level was RUB4.2-4.4k/bbl), being negative for the budget. Under the current oil price, we would not expect emergency FX interventions at levels stronger than USD/RUB 80-85.

- The downgrade of the oil price suggests that our expectations of a US$45bn current account surplus for 2020 (made under a US$65/bbl Urals assumption) is too optimistic: each US$1/bbl of oil price assures around US$3 bn of fuel exports, and the drop in exports will only partially be offset by lower imports, as around 50% of total imports reflect investment imports, and those are likely to be needed in order to assure investment growth the government is targeting. As a result, we would not exclude a zero to negative CA balance at least in 1H20, leaving RUB exposed to capital account volatility.

- With little involvement from the CBR on the FX market, the USDRUB sensitivity to oil price moves should now be higher - closer to values seen before the introduction of the fiscal rule, when a US$2/bbl move in the oil price was enough to ensure a 1.0 change in the USD/RUB exchange rate. Meanwhile, portfolio flows related to OFZ are unlikely to provide support to RUB in the near term: historical analysis of previous risk-off episodes (2014, 2018) suggest a likelihood of 4-9 months of flat to negative flows.

Figure 2. With Urals close to cut-off price, effect of suspended FX purchases is smaller than it was in 2018

Figure 3. RUB has been narrowing its discount to peers since 2016 - till the OPEC+ deal fell apart

Figure 4. Russian market is now under a higher influence of foreign portfolio flows

Rates: key rate on hold (at least), bond market to focus on fundamentals later

While some market participants are now expecting the CBR to hike rates, as it did in 2H18 or at the end of 2014, we do not see the urgency in raising the key rate now.

- The emergency rate hike at the end of 2014 (including the final mid-December hike from 9.5% to 17.0%) was the mark of a transition in the monetary policy regime from managed FX floating to inflation targeting amid a deteriorating foreign policy backdrop, 50% USD/RUB depreciation and rapidly climbing inflationary expectations.

- The episode of two 25 bp hikes in September and December 2018 is a closer analogy, however back then inflationary expectations were facing upward pressure not just because of RUB depreciation, but also amid expecations of an inflationary shock from the VAT rate hike, which materialized only partially, and the CBR had to reverse the move in the following year.

- Russia is entering the current volatility episode with CPI expected by the CBR at year-end 2020 of 3.5-4.0%, below the 4.0% target, with estimated FX pass-through into CPI of 0.3-0.5 percentage point (pp) per each 10% FX depreciation (vs. around 1.0 pp previously). With 17% year-to-date depreciation, CPI expectations could deteriorate by 0.5-0.9 pp, which does not suggest a major overshoot of the CPI target. Meanwhile, further USD/RUB depreciation - to and beyond the aforementioned USD/RUB 80-85 range would mean up to 23-27% year-to-date depreciation or more, potentially creating risks to the CPI target. In that extreme case, an emergency rate hike is possible.

- Another difference of the current episode is that global central banks are facing a downward rate cycle in response to global growth concerns, which suggests that even at an unchanged nominal key rate Russia's real rates are to remain at a high level relative to peers. According to our observations, Russia's real rate is competitive both in terms of current CPI (see Figure 5) and based on expected CPI at year-end 2020.

As result, if USD/RUB stabilizes at the current 75.0 level we expect the CBR to react by keeping the key rate flat at 6.0% in March-April, which will in effect be a tightening in the stance vs. previous expectations of at least two 25 bp cuts. More material RUB depreciation, however, could lead to a higher key rate due to a material worsening in CPI expectations. We are planning to present our detailed considerations on the Russian CPI trend in a separate article.

As for the bond yields, while the Russian market was closed on Monday, its EM/commodity peers saw around a 30 bp spike in 10-year local currency bond yields, and we do not exclude OFZ catching up. Weekly OFZ placement auctions are likely to be cancelled for the second week in a row. In the near term we expect the market performance to be driven by the overall performance of oil prices and EM risk sentiment. Favourable Russia-specific considerations, including one of the lowest break-even oil prices among oil exporters (around US$50/bbl), low state debt (around 13% GDP), liquid fiscal reserves of US$150 bn (each US$1/bbl of oil price below US$50/bbl breakeven suggests a deficit of around US$2 bn per annum), and one of the highest real rates will only return to investors' focus after the oil market and EM risk appetite stabilizes.

Figure 5. Russia's real rates are at the top of peers' range

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In case you missed it: Pandemic pandemonium

- This bundle contains 13 Articles