Monitoring Hungary: Shaken and stirred

- 13 May 2022

- Hungary

In our latest update, we reassess our Hungarian economic and market forecasts which have been shaken by the impact of incoming data showing stronger inflation and higher GDP growth. The central bank's recent change in approach has also stirred our views

Hungary: At a glance

- We are upgrading our 2022 economic outlook as Hungary showed significant economic resilience in March.

- The pro-inflationary impact of the Ukraine war is finally filtering through into the data and we move our inflation forecast higher.

- The National Bank of Hungary (NBH) has switched aggressiveness to graduality, changing our view of the rate path.

- Growing external imbalances will remain with us even if Hungary is exempt from the Russian oil embargo.

- The new government is being formed, but until that is done we don't see a shift in fiscal policy.

- Even without a full-blown, all-in austerity package, we see the chance for a negative rating action as limited.

- Sliding external balance puts systemic pressure on the Hungarian forint (HUF), but we still like HUF beyond short-term risks.

- With inflation expectations rising further and NBH being less aggressive, we see bear flattening in the local yield curve.

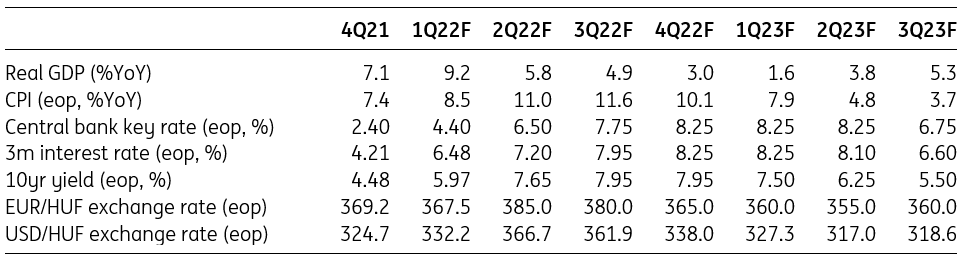

Quarterly forecasts

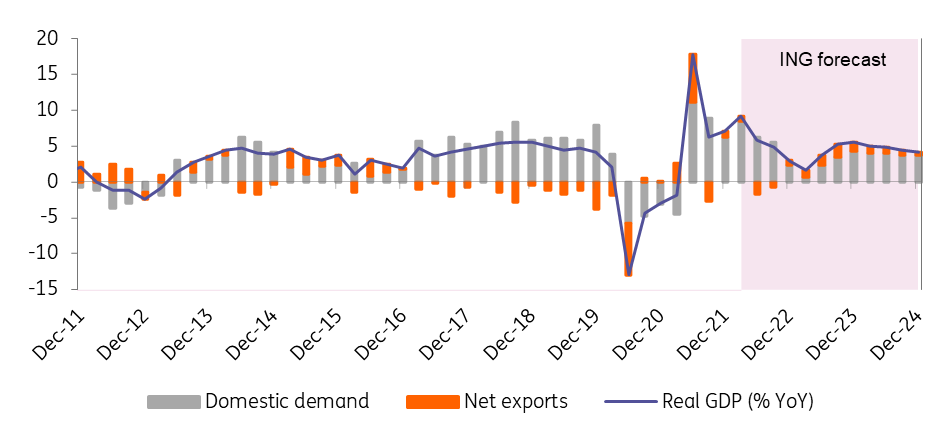

Resiliency leads us to an upgraded GDP outlook

The Hungarian economy showed resilience against the first shock of the war in Ukraine. The latest incoming high-frequency data from the industry, retail and construction sectors suggest a significant pick-up in economic activity both on a quarterly and a yearly basis. Other proxies suggesting strong GDP growth include the higher-than-expected consumption-related budget revenues (both in nominal and real terms) and the developments of various government subsidies (e.g. housing subsidies). Thus, we see an above 9% year-on-year GDP growth in the first quarter. Such a strong start with a significant positive carry-over effect means that even with the challenges ahead, the 2022 economic performance will be sound. We upgrade our outlook for this year to 5.7%.

Real GDP (% YoY) and contributions (ppt)

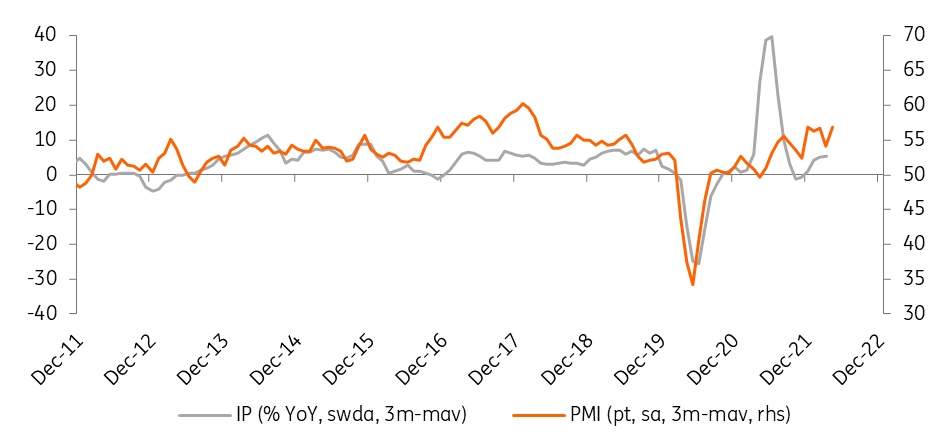

Industry does well despite a plethora of challenges

Industry's dynamic growth seen during the first two months of 2022 has been broken – but it could have been worse. Production dropped by only 0.1% month-on-month, translating into 4.2% year-on-year growth in March. After the outbreak of the war, automotive companies cut production hours and shifts due to a shortage of spare parts and logistic woes. Traces of this can be seen in the weaker performance of the industry. While car manufacturing saw production drop considerably, the other two major sub-sectors (electronics and food) showed above-average growth rates alongside good performances from smaller sectors. If companies are able to reshuffle their supply channels, keep their workers despite rising salary demands on labour shortage, and adapt to rising financial constraints due to the higher interest rate environment, there will be better days ahead. The reason is simple: based on the stock of orders which is 26% higher on a yearly basis, the demand is clearly there to jumpstart production if limitations are easing.

Industrial production (IP) and Purchasing Manager Index (PMI)

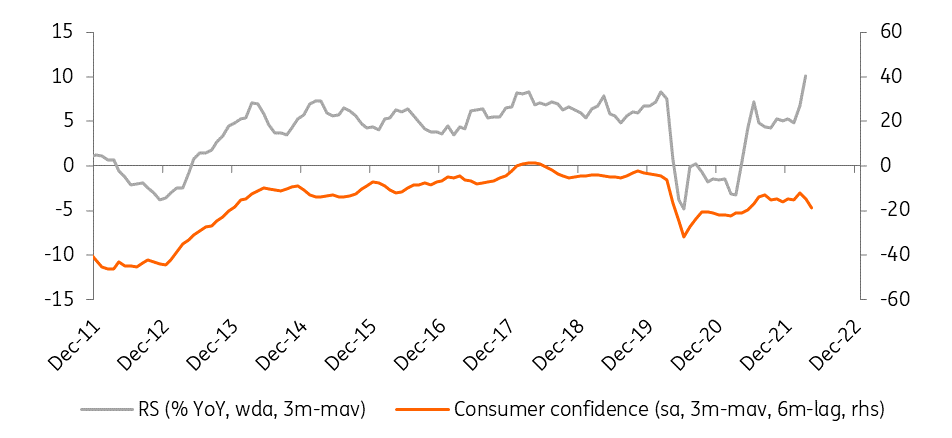

Retail sales soar in March

Hungarian retail sales rose by 16.2% year-on-year in March. The 7.3% increase on a monthly basis indicates that this is more than just a base effect. The non-food sector registered a 5% monthly increase, culminating in an almost 30% higher volume of sales on a yearly basis. We see two drivers here. Hungarian households provided significant support to Ukrainian refugees, while rising inflation may have motivated shoppers to bring forward their planned consumption, which was made possible by a significant jump in disposable income (as a result of wage growth, government transfers, etc). Fuel retailing was up by 51.4% in March with a 27% month-on-month increase. This is a result of the fuel price cap boosting fuel tourism in border cities, plus the movement of refugees has generated more traffic, increasing the demand for fuel. Furthermore, fears of fuel shortages and restrictions led to panic buying at fuel stations during the middle of March. Such a pace of growth is undoubtedly unsustainable, but it is also certain that it will push GDP growth tremendously during the first quarter of 2022 via the surge in consumption.

Retail sales and consumer confidence

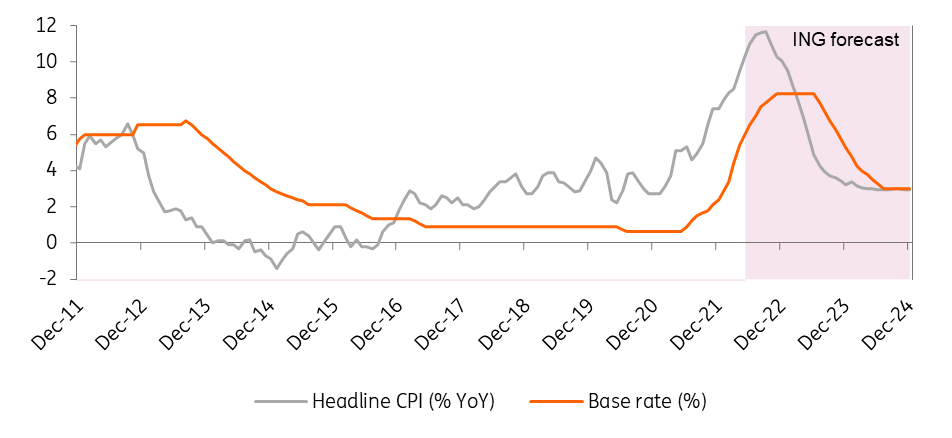

We move our inflation forecast higher

There was a sharp rise in prices in April: on a monthly basis, it reached a 1.6% rate. Roughly 50% of the consumer basket items showed double-digit, year-on-year inflation. Against this backdrop, the 9.5% year-on-year headline inflation print is hardly surprising. The main reasons behind the acceleration in price growth were food and other goods including motor fuels and durables. With tobacco – not part of core inflation – being the only major drag on headline inflation due to base effects, core inflation accelerated even more, reaching 10.3% year-on-year. Inflation in Hungary is expected to rise further in the coming months, as the economy continues to show a significant demand-supply mismatch. Labour shortages, rising wages and other supply-side shocks are increasingly spilling over into consumer prices, with companies enduring significant pricing power. In light of April’s upside surprise, headline inflation will soon reach double-digits as well. The extent and timing of the peak in price pressure highly depend on the fate of price caps, but as of now, we see the peak well above 11% in the third quarter. On average, we now forecast a 10.1% headline reading in 2022.

Inflation and policy rate

Central bank changes approach, we change our rate path

At its April meeting, the National Bank of Hungary moved the 1-week deposit rate up by 30bp to 6.45% and raised the base rate by 100bp to 5.40%. While our upgraded forecasts for GDP and inflation would create the need for a shift in higher gear in monetary tightening, the central bank seems to have a different view. The latest hint from the National Bank of Hungary (on 12 May) prepares markets for a switch in strategy, giving up on the aggressive period of rate hikes in exchange for a gradual approach, probably already from May. Such a move would fit with the April pledge of the central bank to be more flexible going forward. Moreover, we see a chance that the NBH is trying to make a preemptive move as we are waiting for the new government to be formed and a fiscal rebalancing announced, which might be stronger than we envision.

As a result of the combination of the shift in the central bank's view and our upgraded forecasts, we maintain our 8.25% terminal rate call with a twist. Instead of reaching this in the third quarter via bigger steps, we now forecast a more gradual path, reaching this level only by end-2022. The upcoming rate-setting meeting (31 May) will give us a much clearer road map regarding what to expect. We see the central bank reducing the pace of the hikes in the base rate and in the interest rate corridor, while the HUF remains under pressure, it might maintain the 30bp step size in the 1-week deposit rate, when it comes to effective tightening.

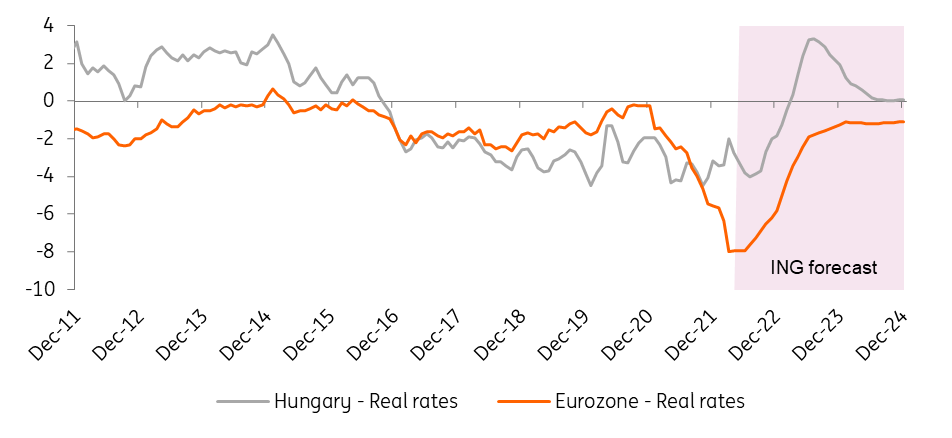

Real rates (%)

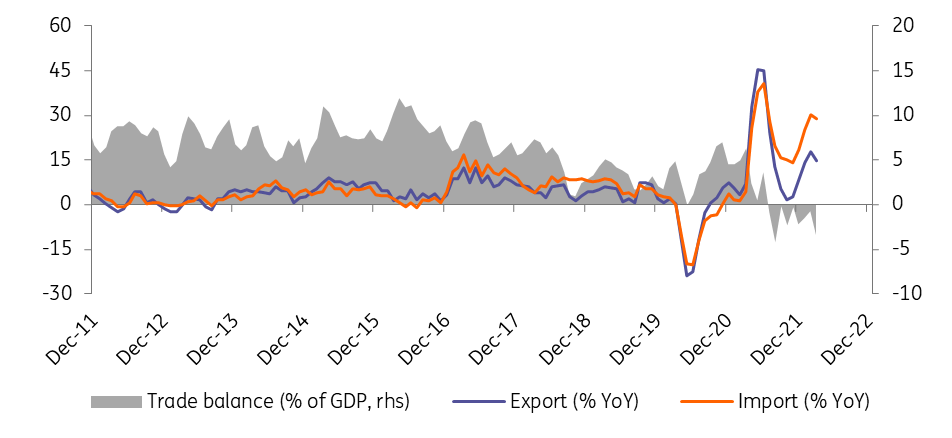

Trade balance remains under pressure

The monthly trade balance has remained in deficit for the ninth month in a row with a shortfall of €503m in March. The value of imports grew by 23% year-on-year mainly due to the rising energy bill of the country. Exports rose by only 8.7% year-on-year as the war impacted the performance of the most important export sector, car manufacturing. The year-to-date trade deficit came in at €0.86bn during the first quarter of 2022, showing a €3.45bn deterioration over the same period of 2021.

Even if Hungary is given an exemption from the Russian oil embargo until 2024, the trade and current account balances could show further deterioration during 2022. With energy prices remaining elevated for the foreseeable future and export capacities remaining constrained, this seems to be the most probable direction. The risks are tilted to the downside as in our base case scenario we expect the government to carry out some fiscal tightening and reach a compromise with the European Commission in the rule-of-law procedure in late 2022. But even with that, we see a roughly 8% of GDP current account deficit accumulated this year.

Trade balance (3-month moving average)

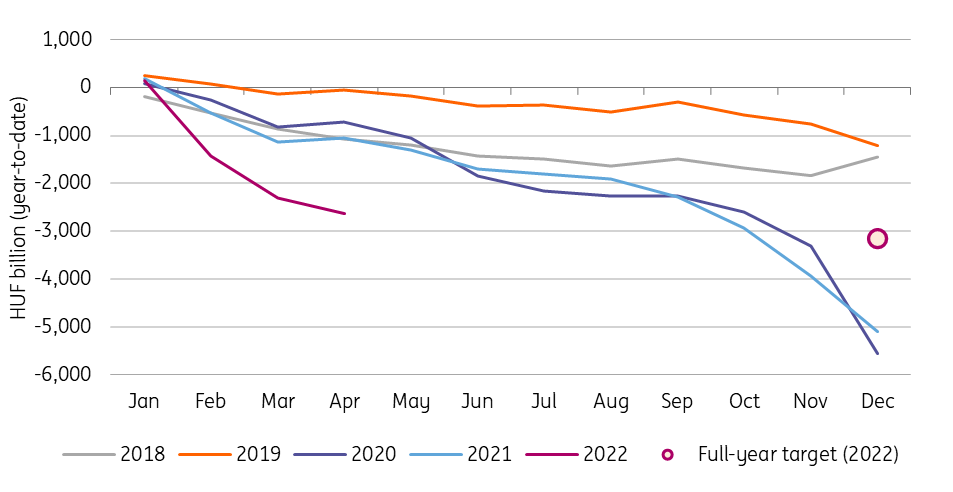

Widening budget deficit

The Hungarian budget posted a HUF 326bn deficit in the month of April. We can say this is something of a mild surprise, at least in the wake of the past three years, when the budget closed with a monthly surplus in the fourth month of the year. The 2022 year-to-date deficit accumulation now sits at HUF 2,636bn, equating to 84% of the full-year cash-flow based deficit target. So, no matter what data we see (monthly, year-to-date or pro-rated deficit), all of it is calling for fiscal adjustment. The Ministry of Finance’s statement highlights the need to improve balance indicators and pledges to preserve Hungary’s stability in the unpredictable global economic environment caused by the Ukraine war. This can be seen as a message to soothe investors' nerves, showing the government is in control. On the other hand, it could mean something much more specific, for example, forward guidance for an upcoming budget adjustment.

The latter explanation is supporting our view that there will be some form of switch in importance between the fiscal and monetary policies during the second half of the year, with fiscal policy providing the bigger tightening impact. The timing, however, remains highly dependent on the formation of the new government, which might only happen by the end of May.

Budget performance (year-to-date, HUFbn)

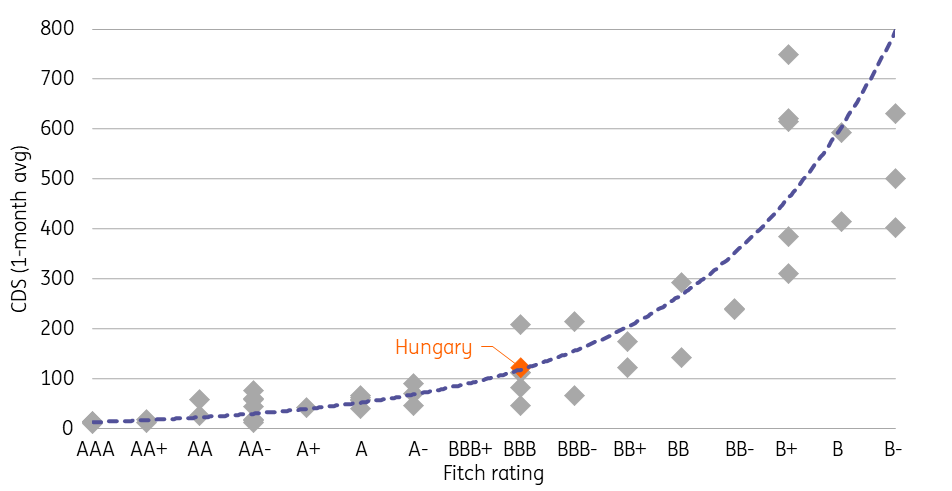

Chance for a negative rating action remains limited

Rating agency Fitch downgraded its outlook for the Czech economy from stable to negative in May. Hungary is facing its next sovereign credit rating review on 22 July from Fitch Ratings. The move regarding our peer makes us wonder about the chances of Hungary receiving a negative rating action, but we think such an outcome remains limited. Although Czech and Hungary are facing similar issues regarding Russian energy dependence, macroeconomic and fiscal indicators are better in Hungary. Inflation will peak well below the reading that we expect in the Czech Republic, while the growth prospect is also significantly better in Hungary, with a much lower risk of stagflation. Moreover, while Fitch expects the Czech fiscal metrics to worsen, Hungary's government seems eager to comply with the pre-war deficit and debt targets, with a further decline in the debt-to-GDP ratio, which will be fuelled by an exceptionally high nominal GDP growth (around 15%).

CDS and sovereign credit rating (Fitch)

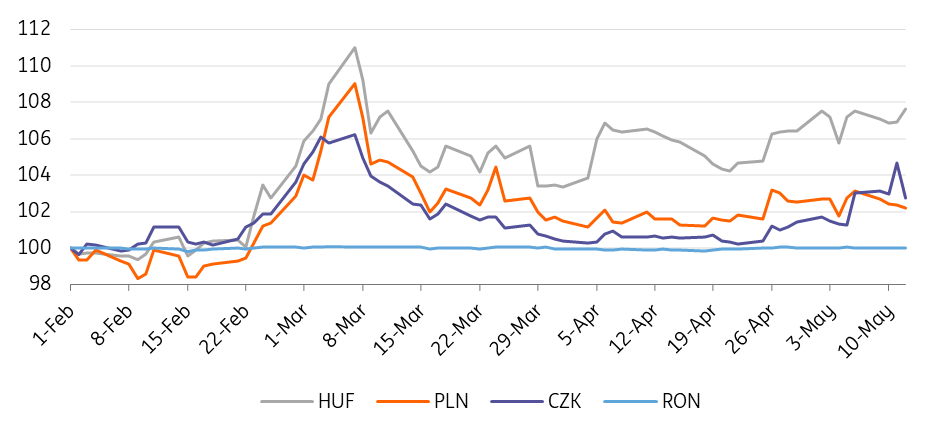

Sliding external balance puts systemic pressure on HUF

EUR/HUF has seen major headwinds since the mid-April bottoming at around 370. Besides the EM FX sell-off, there have been some idiosyncratic shocks, like the ongoing rule-of-law procedure. The key structural factor behind HUF weakness remains the continuous deterioration in the external balance due to the country’s rising energy bill. This puts systemic pressure on the forint, making a structural bet against HUF easier for investors. The National Bank of Hungary’s ongoing tightening could provide some support here. Although the latest shift in tone (signalling a more gradual approach than being aggressive) has not been very welcomed by markets. However, in our view, this shift is more about the base rate and the speed of convergence of the 1-week deposit rate and the base rate than the effective tightening itself. In this respect, we see 380-385 remaining the range for the next three months. As the hoped-for de-escalation ripples through markets, we envision EUR/HUF easing back in the 355-360 range in the longer run.

FX performance vs EUR (1 February = 100%)

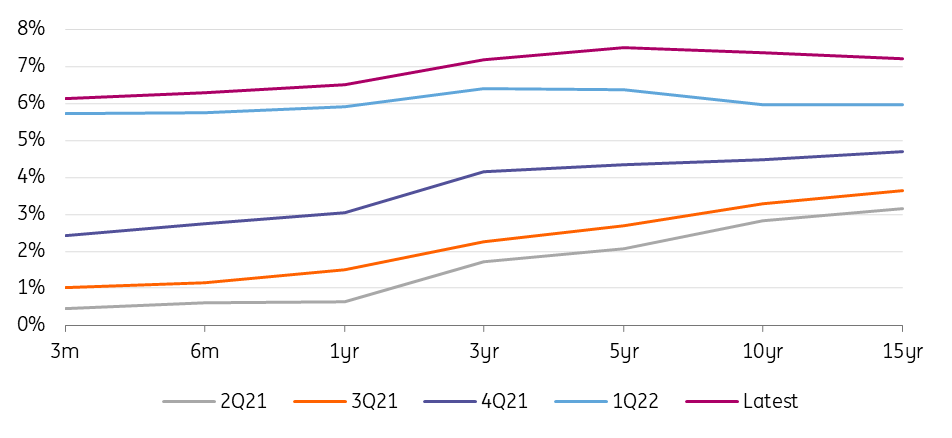

Yield curve to move higher

The domestic debt and rates market remains highly dependent on the mix of moves in core rates and the restructuring in local economic policies. On the former, core rates will remain on an uptrend in the short run. On the latter, we see a more gradual monetary tightening approach (8.25% terminal rate reached only by year-end) resonating with the moderate rebalancing in the budget. This mix may get questioned by markets in the wake of further rising inflation and strong first-quarter economic activity, adding to the already elevated inflation expectations. This could result in a further bear flattening in the yield curve with a possible inversion in the fourth quarter of 2022.

Hungarian sovereign curve

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more