Central banks: Our latest calls

- 13 May 2022

Our team outline their forecasts for central banks, as policymakers continue to make changes in interest rates amid global inflation concerns

Developed markets: Our calls at a glance

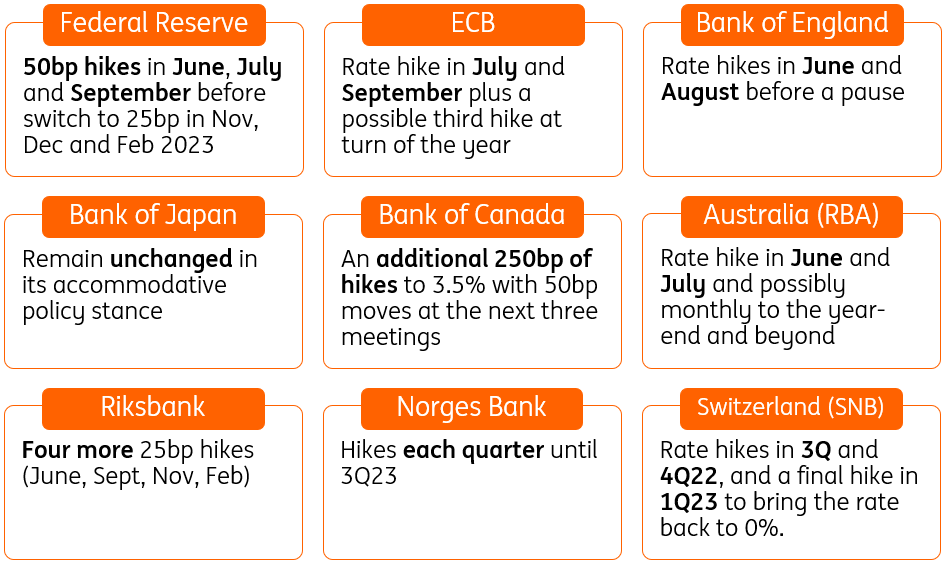

Federal Reserve

Our call: 50bp rate hikes in June, July and September before switching to 25bp in November, December, and February 2023 as quantitative tightening (QT) is felt. Rate cuts in 2H 2023.

Rationale: Domestic demand remains strong and in this environment businesses are able to pass higher energy, commodity, labour and supply chain-related costs onto their customers. The Fed is seeking to bring demand into better balance with the supply capacity of the economy. But moving into restrictive territory means slower growth and the risk of an adverse reaction and we expect the Fed to move to a more neutral position in late 2023.

Risk to our call: Domestic demand is resilient with wage rises accelerating amid ongoing labour shortages, risking higher, more prolonged, inflation. Conversely, the economy reacts badly to rate hikes (the housing market is vulnerable) and recession prompts a more rapid reversal in Fed policy.

James Knightley

European Central Bank

Our call: Rate hike in July and September plus a possible third hike at the turn of the year before pausing.

Rationale: Uncertainty surrounding the economic outlook remains high but higher inflation for longer, additional inflationary pressure still in the pipeline, and fears that the window to act could be closing rather soon pushes the ECB to act earlier. Official comments since the late April ECB meeting suggest that there is growing consensus to normalise monetary policy, i.e. ending net asset purchases and the era of negative deposit rates. Only the timing is still under discussion. Looking beyond normalisation, however, high government debt, the need for investments, a potential loss in competitiveness, and prospects of easier monetary policy elsewhere argue against a series of rate hikes.

Risk to our call: A strong economic rebound after any end to the war in Ukraine and wage pressures building on the back of reshoring and labour shortages could keep the hawks at the ECB in the lead and push for further rate hikes in 2023.

Carsten Brzeski

Bank of England

Our call: Rate hike in June and August before a pause.

Rationale: With four rate rises under its belt, the committee has become more cautious and has hinted that markets are overestimating future hikes. Its latest forecasts showed that, if it hiked roughly six further times, inflation would be well below target in two to three years' time. While markets have been assuming the BoE’s hike profile will look similar to the Fed’s, the UK’s more ‘European’ growth outlook in the near term suggests a less imminent need for aggressive tightening.

Risk to our call: Wage pressures continue to build, so if the growth story turns out to be less lacklustre than feared, the hawks on the committee may well push for a higher terminal rate by early 2023. Like our Fed call, that would also inevitably bring forward the date of the first rate cut.

James Smith

Bank of Japan

Our call: Bank of Japan will maintain an accommodative policy stance.

Rationale: CPI will rise up and stay above 2% for a while, but BoJ will downplay it as cost-push driven inflation that will prove temporary. Market expectations on a possible policy change were killed after last month’s BoJ meeting, and no action change before year-end is expected.

Risk to our call: If a weak Japanese yen hurts the economy, then the bank may revisit its monetary policy stance, but that's more likely once Governor Haruhiko Kuroda retires next April.

Min Joo Kang

Bank of Canada

Our call: An additional 250bp of rate hikes to 3.5% with 50bp moves at the next three meetings.

Rationale: The Canadian economy looks set to be among the top performers in 2022 and 2023 thanks to a strong jobs market and an important commodity production focus. Inflation is at 30-year highs and is still rising while the housing market remains vibrant. The BoC is worried about inflation expectations becoming unanchored and is implementing a swift run down in its balance sheet in combination with rapid interest rate increases.

Risks to our call: Predominantly to the upside given the positive economic outlook, especially if labour shortages become more of a problem and wage growth accelerates. It is worth noting that the BoC tends to be more interventionist/reactionary than the Federal Reserve. The BoC has embarked on six separate interest rate hike cycles since 2000 versus only four from the Federal Reserve.

James Knightley

Reserve Bank of Australia

Our call: Rate hike in June and July and possibly monthly to the year-end and beyond.

Rationale: Having just hiked rates by 25bp in May, and escaping from the dovish shackles it had created for itself, there is now little to stop the RBA from responding to the much higher inflation backdrop than the one it had bargained on seeing. The next big data release will be the wage price index on 18 May. This should ensure a further June hike of 25bp, and possibly set the scene for rate hikes in July and August too. Even so, markets have priced in an unrealistically aggressive path for tightening from the RBA over the course of the year, even if inflation remains high and growth remains robust.

Risk to our call: Higher wages growth and higher inflation coupled with still robust growth could see the RBA accelerate its tightening to 50bp in coming meetings.

Rob Carnell

Riksbank

Our call: Four more 25bp hikes (June, September, November, February).

Rationale: Inflation has come in much higher than the Riksbank had expected earlier this year, prompting a monumental turnaround in thinking. Having signalled no hike before 2024 at its February meeting, the central bank hiked in April and its forecast indicates several more to come. Policymakers are focussed on wage talks that conclude next spring, and a tight jobs market combined with higher inflation expectations look set to usher in a higher pay settlement.

Risk to our call: Inflation came in higher than expected again and the central bank’s own scenarios from its last report suggest that could prompt a 50bp hike in June, despite the governor ruling it out for now.

James Smith

Norges Bank

Our call: Hikes each quarter until 3Q23.

Rationale: Norway was among the first to tighten amid the higher energy price environment, a boon for the domestic economy. Norges Bank is more mechanical than most in the way it sets policy and seems comfortable with its one-hike-a-quarter pace set so far.

Risk to our call: Inflation was well above Norges Bank forecasts in April and policymakers have hinted that this could prompt a 50bp hike in June, something we think is becoming increasingly likely.

James Smith

Swiss National Bank

Our call: Rate hikes in Q3 and Q4 2022, and a final hike in Q1 2023 to bring the policy rate back to 0%.

Rationale: With Swiss inflation at 2.5%, above the SNB's target, and the ECB in the process of raising rates, we believe the SNB will seize the window of opportunity to also normalise its monetary policy by exiting negative rates and bringing its rate back towards 0%.

Risk to our call: Any deterioration in the global economic environment leading to a flight to safety would lead to an excessive appreciation of the Swiss franc and prevent the SNB from raising rates.

Charlotte de Montpellier

Central and Eastern Europe/EMEA: Our calls at a glance

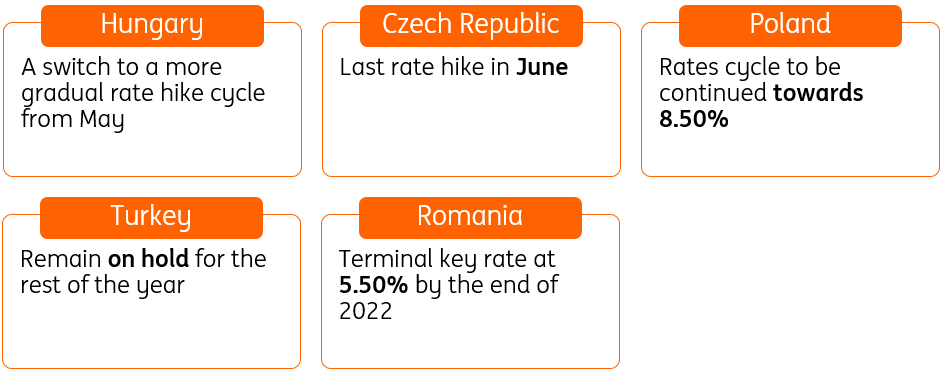

National Bank of Hungary

Our call: A switch to a more gradual rate hike cycle from May.

Rationale: While the Hungarian central bank was among the first to start tightening (in June 2021), the road might be longer than initially thought. Underlying inflation pressures reached double-digit territory in April. Inflation expectations of households are becoming less anchored, while an increasing number of companies (60-80%) are considering further increases in prices. Add in the weak forint, labour shortages, a pre-election fiscal thrust and a more positive output gap to the equation, and we end up with a need for a more lengthy tightening cycle, with a terminal rate of around 8.25% in the fourth quarter.

Risk to our call: A stronger-than-expected fiscal rebalancing/tightening could lift some of the burden from monetary policy, giving an opportunity for the central bank to stop its own tightening cycle at a lower terminal rate (probably at around 7.5%).

Peter Virovacz

Czech National Bank

Our call: Last rate hike in June.

Rationale: The announcement of a new governor is likely to move the CNB from being the biggest hawk in the region to the biggest dove. In the baseline scenario, the current board operating under the current governor will raise interest rates by at least 100bp, following a CNB staff recommendation. However, from 1 July, a new board will take over the leadership, which will shift monetary policy towards a dovish view, which brings rates stability as well as cuts to the outlook.

Risk to our call: The composition of the new board is the biggest risk that could change our call significantly. The question is whether the president will appoint names close to the new governor or whether views on the board will be diversified, which would make it harder to find consensus and likely lead to a longer period of stable rates.

Frantisek Taborsky

National Bank of Poland

Our call: Rates cycle to be continued towards 8.50%.

Rationale: High inflation is the number one economic and political issue, and the Monetary Policy Committee has already lifted the main policy rate from 0.10% to 5.25%. However, the decision to increase it by 75bp in May (compared to 100bp in April) is not a sign that the tightening cycle is drawing to an end. With headline inflation potentially reaching 15% before the end of this year, we still see a lot of room for further tightening and we see a target rate at 8.50%, which could even potentially be reached this year. Given the scale of fiscal stimulus, the policy mix only recently turned contractionary. Markets expect rate cuts in 2023, but our CPI scenario does not warrant such a swing in monetary policy.

Risk to our call: Inflation risks remain to the upside amid second-round effects, a de-anchoring of inflationary expectations, a wage-price spiral, and expansionary fiscal policy. With real rates remaining so negative, the MPC is unlikely to stop tightening unless it sees a turnaround in inflation.

Adam Antoniak

National Bank of Romania

Our call: Terminal key rate at 5.50% by the end of 2022.

Rationale: There's a considerable difference in key rates in Romania compared to its CEE3 peers (Poland, Czech Republic and Hungary). Given that the discussion about the transitory nature of inflation is well behind us, that suggests that growth concerns are a bigger factor behind this differential. However, the apparent gains of this policy stance could, in our view, be more than offset by the market perception that the NBR is too far behind the curve and will need to allow a swift adjustment higher at some point in time.

Risk to our call: Should the other CEE3 central banks continue the pace of rate hikes, the NBR will be forced to follow. On the other hand, eventual rate cuts in the CEE3 space are unlikely to be followed in Romania over the next couple of years.

Valentin Tataru

Central Bank of Turkey

Our call: Rates to remain on hold for the rest of the year.

Rationale: Given that the CBT’s policy framework relies mainly on an FX-protected deposit scheme, we have seen a two-pronged approach lately. Firstly, it tightened reserve requirements to curb commercial TRY loan growth. Secondly, and in line with the "liraisation" strategy which aims to encourage a higher take-up of FX-protected TRY deposits on the retail side and to strengthen its FX reserves, the CBT has also made adjustments in the FX-protected scheme to increase appetite. We expect the same policy line to continue for the remainder of this year.

Risk to our call: Risks are on the rise in the near term, due to:

- An acceleration in lending that can feed into local FX demand, increasing inflationary pressures via domestic demand and a weakening currency, further pressurising the current account despite currency depreciation if we see real lending growth.

- The war in Ukraine leads to significant problems via the trade channel, adverse effects on tourism, pressure on oil prices and a higher risk premium.

- A less supportive global backdrop adds challenges given Turkey’s high external financing requirements. This risk profile could lead to a rate response.

Muhammet Mercan

Asia (ex Japan): Our calls at a glance

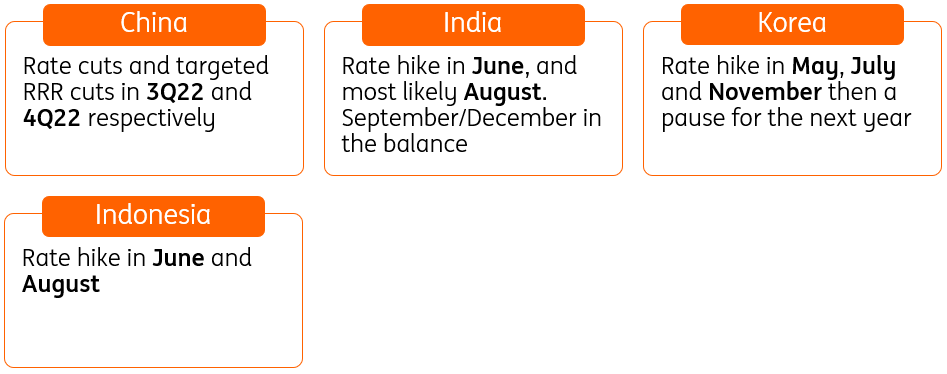

People's Bank of China

Our call: Rate cuts and targeted reserve requirement ratio (RRR) cuts in 3Q22 and 4Q22 respectively.

Rationale: The economy has suffered from disrupted demand due to social distancing measures. The wages of some consumers are affected, and their consumption demand is falling. But there is also a big pool of consumers that have stable incomes but cannot spend due to lockdowns. It is a similar story for producers. As such, we cannot expect monetary policy to do a lot to help the economy. Targeted RRR cuts that focus on small and medium-sized enterprises could be more relevant in this situation.

Risk to our call: Preventing inflation is mentioned repeatedly by the PBoC. The central bank may refrain from cutting rates if this is one of its top priorities.

Iris Pang

Reserve Bank of India

Our call: Rate hike in June, and most likely August. September and December hang in the balance.

Rationale: The RBI surprised markets with an unscheduled 40bp rate hike in June as March inflation data touched 7.0%. Inflation has almost certainly further to climb, and the 40bp increase in rates in May does little to close the gap between policy rates (4.4%) and headline inflation, so there is certainly more hiking to come. That said, the RBI’s statement shows that it is still fixated on supporting growth, and its goal is to remove accommodation rather than to tighten policy (an important semantic distinction) so we don’t anticipate that it will increase the pace of its tightening, or hike at every meeting until it closes the gap with inflation.

Risk to our call: The current RBI guidance may be misleading if inflation remains high, or accelerates, or if there is evidence of second-round effects, in which case, the pace and frequency of tightening could also accelerate.

Rob Carnell

Bank of Korea

Our call: Rate hike in May, July and November then a pause for the next year.

Rationale: We expect CPI to shoot up and stay higher than expected until 3Q22, while GDP growth is likely to slow only modestly and remain relatively healthy on the back of reopenings and supportive fiscal policy. We expect the Bank of Korea to frontload its hikes in the near future but as we approach year-end, it will slow down and try not to go beyond 2.25%. However, markets expect BoK hikes to continue next year and go beyond that level.

Risk to our call: If higher wage growth pushes up inflation by more than expected, then the BoK may deliver additional rate hikes this year.

Min Joo Kang

Bank Indonesia

Our call: Rate hikes in June and August.

Rationale: Perry Warjiyo, the governor of Bank Indonesia, has hinted at a potential move since January but has pointed to core inflation as the trigger point. Core inflation, now at 2.6%, should continue to accelerate in the near term. A sustained rise in core inflation coupled with a robust 1Q GDP report should prod an adjustment from BI by June followed up with a second adjustment by August.

Risk to our call: Concern about the stability of growth has been the main reason behind the reluctance to hike so far this year. Any signs that the recovery is faltering could force a pause or delay in the BI rate hike cycle.

Nicholas Mapa

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more