CIS-4: Domestic resilience leads to softer rates outlook

- 11 June

- Armenia Azerbaijan

A firmer commodity price outlook adds to the global inflation story, but CIS-4 remains mainly driven by domestic themes. Commodity exporters benefit from stronger buffers, while FX resilience and softer CPI in Kazakhstan and Uzbekistan leave room for a more accommodative rates outlook

Armenia: Election results suggest continuity

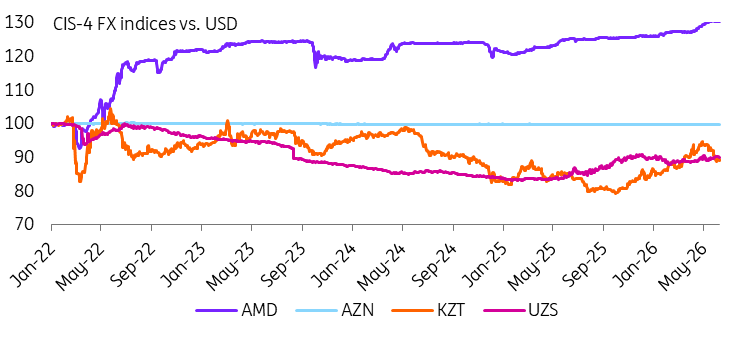

The recent win for the ruling party in Armenia secures policy continuity. Still, the lack of a supermajority potentially complicates any constitutional changes needed to resolve tensions with Azerbaijan or ensure accession to the EU. On the one hand, the risk of unresolved frictions with Azerbaijan remains a reason for caution on the dram after strengthening supported by portfolio inflows and the pickup in annualised net remittances inflow to around 7% of GDP. On the other hand, slower Armenia-EU progress lowers the near-term risk of Russian economic retaliation. Russia is responsible for at least 80% of Armenia’s gas imports, one-third of external trade and two-thirds of gross remittances inflows. For now, it remains unclear whether the political narrative of Armenia-EU-Russia is actionable for markets.

Against the backdrop of inconclusive foreign policy signals, strong currency performance so far, and benign CPI within the 4-5% year-on-year range, we expect the Central Bank of Armenia to keep the policy rate unchanged at 6.50% next week with a balanced medium-term outlook.

Azerbaijan: Trade remains the key strength

Azerbaijan remains the main beneficiary of elevated fuel prices, in line with our long-standing view. For now, higher fuel income and broader energy diplomacy remain the key story. The recent news flow points to a continued focus on developing trade channels, as international investments into the country’s ACG field are being considered, a 15-year Absheron gas supply deal with Turkey has been signed, and the country’s Baku-Supsa route is gauged as Kazakhstan’s alternative export channel.

We see our updated global view as a direct boost to Azerbaijan’s external and fiscal buffers, with the budget surplus now expected to reach 5% of GDP and the current account to total 11% of GDP in 2026. Meanwhile, a relatively high exposure to CPI contagion from trading partners and lagging GDP activity growth remain factors to watch.

Even fuel importing CIS countries have shown FX resilience to Middle East tensions

Kazakhstan: Real rates remain high despite recent cut

Higher oil prices are supportive of Kazakhstan’s current account and budget as well, but the more important story is domestic. Despite the recent correction, the outlook for the tenge still appears to be supported by non-oil export proceeds and portfolio inflows, which should help cushion imported inflation risks. This matters because stronger FX, combined with still-high real rates, lowers the need to turn more hawkish even as the global inflation backdrop worsens.

After last week’s surprising 100bp cut, the next decision is more likely to be a hold, but the scope for further easing still exists in the medium term, in our view, especially if KZT remains supported by trade and capital flows.

Uzbekistan: Constructive view on UZS reaffirmed, rate outlook improved

Uzbekistan’s domestic story continues to improve. The restart of gold exports since April, together with portfolio inflows linked to the privatisation pipeline and improved sovereign rating prospects, is supporting the soum again. UZS has strengthened by around 1% since the outbreak of the Iran war despite a 15-20% correction in the gold price. Combined with apparent fiscal consolidation, this has helped push the inflation rate down by 1.8ppt since the start of the year to 5.5% year-on-year in May.

In our view, there is room for the Central Bank of Uzbekistan to cut the policy rate from 14.00% at next week’s meeting, contrary to global trends.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Already playing into extra time

- This bundle contains 14 Articles