- Quick take

- 5 June

- Kazakhstan

Kazakhstan makes a surprise rate cut, with next move to depend on the tenge

Kazakhstan’s central bank cut the base rate by 100bp to 17.00%, surprising the market with an earlier and bolder move than we expected. Softer CPI, lower inflation expectations and supportive portfolio flows opened room for easing. Follow-up cuts would require continued KZT strength and a drop in CPI to a single-digit level

| 17.00% |

NBK base ratea 100 basis point cut |

| Lower than expected | |

Kazakhstan cuts earlier and bigger than expected thanks to softer CPI trend

The National Bank of Kazakhstan (NBK) cut the base rate by 100bp to 17.00% today, delivering a dovish move relative to market expectations and our base case. We had expected the easing cycle to start later this year, but the latest changes in CPI and FX trends tipped the balance in favour of an earlier and more aggressive cut than we had previously expected.

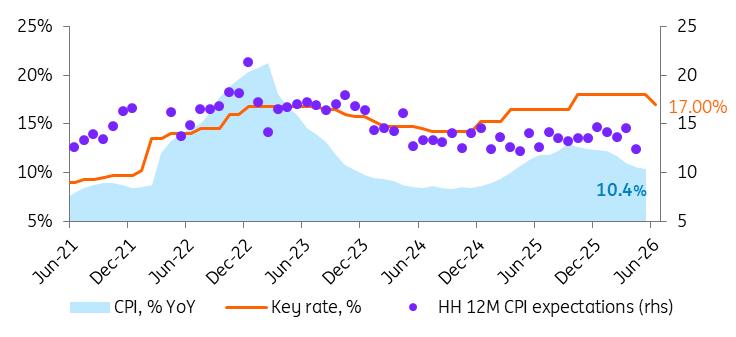

The main reason for the earlier move, in our view, was an improvement in the current inflation picture. May CPI slowed to 10.4% YoY, beating expectations and reinforcing the recent disinflation trend. At the same time, households’ inflation expectations fell materially, by 1.8 percentage points, reinforcing NBK's confidence. In addition, the tenge has strengthened by around 2% against the US dollar since the start of the Iran war, adding to disinflationary pressure.

NBK base rate cut on continued disinflation and improved household expectations

Kazakhstan CPI, households' 12M CPI expectations, and base rate

Real rate, portfolio flows, and KZT dynamics were likely taken into consideration too

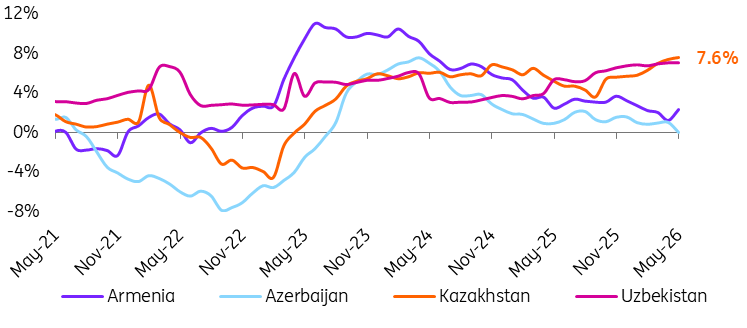

We do not exclude that part of the NBK’s motivation was to avoid excessive speculative portfolio capital inflows in the context of recent Euroclear access and issuance plans. Before today’s decision, Kazakhstan’s real policy rate, based on current (ex-post) CPI, had risen to around 7.6% by end-May, one of the highest levels in the CIS space. That created some room for a cut in the nominal rate.

The wording of today’s commentary also suggests that the tenge played a more visible role in the central bank’s assessment than at the previous meeting. The exchange rate was mentioned more frequently than in May – three times vs. one – and was presented as one of the reasons for the 0.5pp improvement in the NBK's year-end CPI forecast to 9.0-11.0% YoY.

In addition, the increase in the 2026 Brent assumption by $24/bbl to $90/bbl led the NBK to improve its current account forecast materially, from a deficit of 3.7% of GDP to a surplus of 0.1% of GDP. In our view, this points to a significantly more supportive implied FX backdrop through stronger export-flow fundamentals, which likely added to the central bank’s confidence in delivering today’s move.

Kazakhstan's real rates are high

CIS-4 policy rates, adjusted for current CPI (% YoY)

Our view: hold is the most likely next step

For the next meeting, a hold is the most likely scenario in our view, unless the tenge continues to appreciate and CPI falls below 10% YoY in the near term.

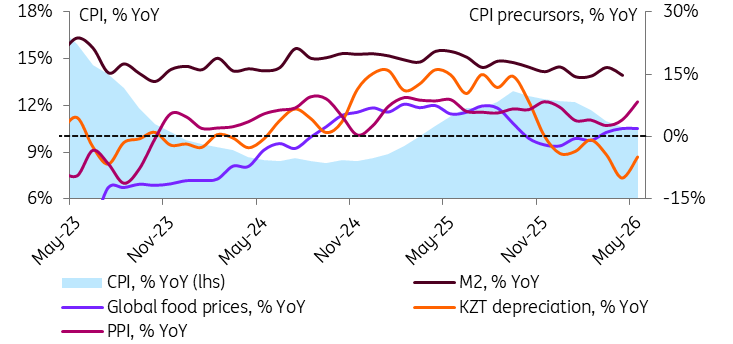

There are several reasons for caution. First, the pickup in global inflationary pressures has already started to feed into higher PPI in Kazakhstan, which could act as a precursor to firmer domestic CPI later on. Second, tenge dynamics remain volatile. This year's pattern has already shown that periods of appreciation can be followed by meaningful reversals, including a 5% weakening in May after an 8% rally in March-April. Third, domestic pro-inflationary risks remain in place, especially those linked to quasi-fiscal stimulus and the eventual unfreezing of utility tariffs, as reiterated by the NBK.

Finally, the current NBK guidance is explicitly more data-driven than last month’s wording, which had leaned more clearly in the direction of a possible cut. In practical terms, this means the central bank has delivered an earlier easing step, but has not committed itself to a sequence of rapid follow-up moves.

KZT and global CPI inputs to remain key for domestic inflation trend

Precursors of Kazakhstan's CPI (% YoY)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more