Dutch maintenance contractors: The new darlings of the M&A market

- 8 December 2023

- Manufacturing, Construction and Retail The Netherlands

There is an increase in takeovers of Dutch maintenance contractors by private equity. They have recently discovered this segment to be a stable growth market. The larger merged contractors also have extra added value because they can better meet the needs of large clients, such as housing associations

Introduction

In this publication we look at the developments, opportunities and risks of mergers and acquisitions (M&A) in the Dutch construction sector. We also discuss the consequences for M&A activity of important trends such as digitalisation, industrialisation and the increasing importance of the renovation market.

Developments of mergers and acquisitions

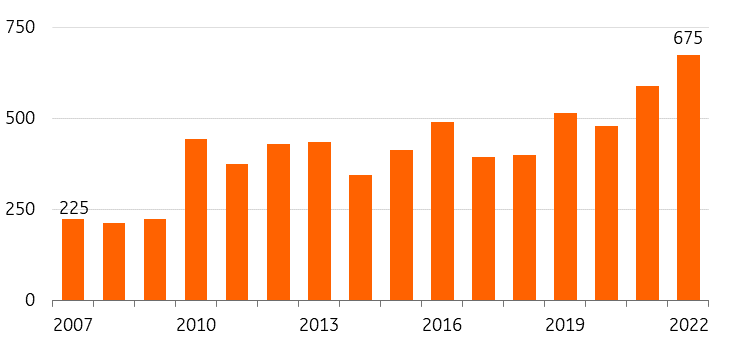

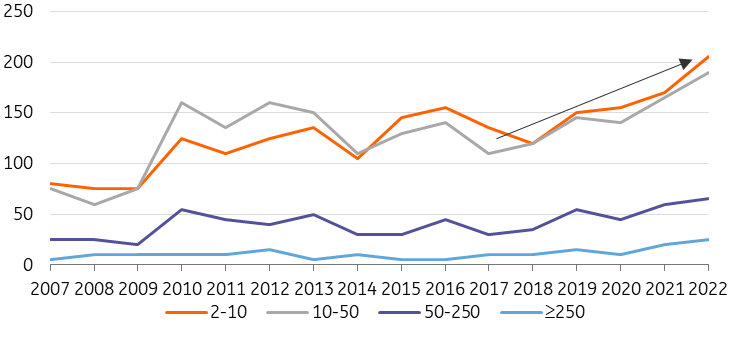

Number of mergers and acquisitions in Dutch construction increases

There has been a big increase in the number of mergers and acquisitions in Dutch construction in the last 15 years. This is in line with other sectors (e.g. accountancy, consultants and IT services sector. In 2022, Statistics Netherlands counted 675 mergers and acquisitions in the construction sector. This is three times as many as in 2007.

Strong growth in the number of mergers and acquisitions in Dutch construction

Development of mergers and acquisitions in construction in numbers

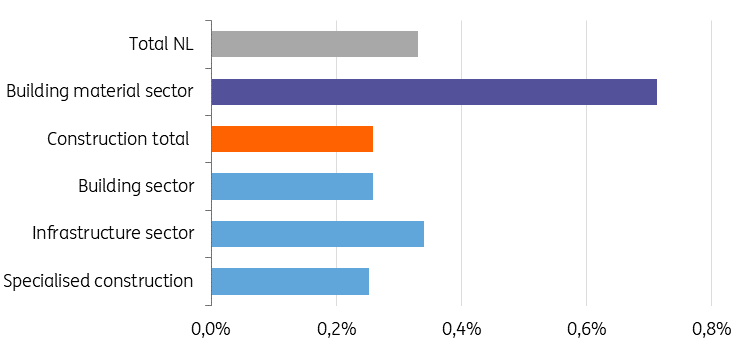

Relatively many mergers and acquisitions in the building material industry

Within the construction supply chain, there are relatively many mergers and acquisitions in the building material industry (= producers of concrete, cement and bricks and are not part of the construction sector). In the period 2007-2022, about 0.7% of all building material suppliers were taken over annually. For contractors, this is much lower, with 0.3% of construction companies per year on average. Because there are considerably fewer suppliers than construction companies, the number of acquisitions in the building material industry (only 20 in 2022) is much lower than among construction companies (675 in 2022).

Relatively many mergers and acquisitions in the building materials industry

Total average number of mergers & acquisitions as a percentage of all companies in the period 2007-2022

More economies of scale for construction suppliers

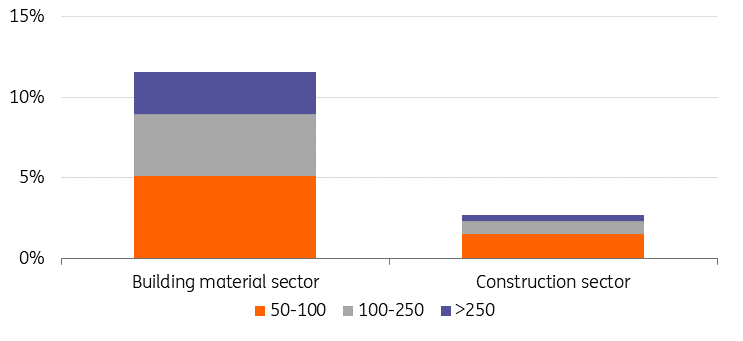

One of the important reasons for more acquisitions in the building material industry is that there are more economies of scale to be achieved in the production of construction materials than in the construction sector. This is because the production of building materials can be industrialised much more easily. Industrialisation also means more investments in factories, robots and machines and that can be done more easily by large companies (see below). This is also evident from the relatively large number of large producers of construction materials. More than 10% of these companies have 50 employees or more. In construction, this is less than 3%.

Many large building materials companies, few large builders

Distribution of large Dutch companies by number of employees, 2022 (excluding self-employed persons)

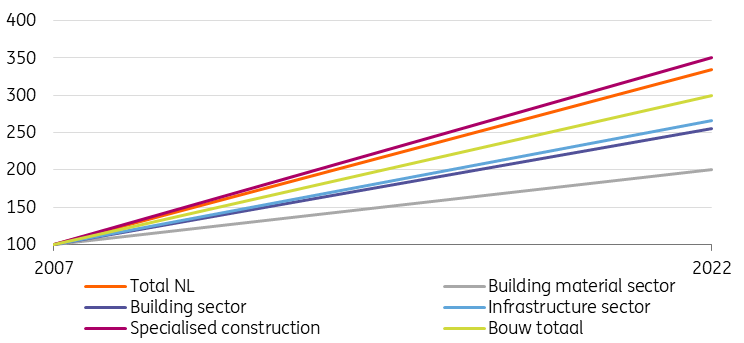

Mainly growth of mergers and acquisitions in specialised construction

In the construction sector, the number of mergers and acquisitions has increased mainly among specialised construction companies, including installers, maintenance companies, earthmoving companies, painters and plasterers. Within this sub-sector, the number of acquisitions in the installation sector seems to have increased considerably. For example, we had the recent takeover of HIG from Bodegraven by installation group VDK. In addition, maintenance companies are also becoming an increasingly popular target for acquisitions (see below). The increase in the number of mergers and acquisitions in the building material industry was relatively limited in the period 2007-2022, but was already relatively high (as we saw in the previous paragraph).

Tremendous increase in mergers & acquisitions in specialised construction

Development of Dutch mergers and acquisitions (Index 2007=100)

More mergers and acquisitions, especially among medium-sized and small construction companies

In the construction sector, the number of mergers and acquisitions has increased among all company sizes in recent years. There were especially many M&A transactions of companies with fewer than 50 employees. These are often maintenance companies that are bought by private equity or other investors.. The number of mergers and acquisitions among larger companies also increased. Due to the lower numbers, because there are simply fewer larger companies, this is still at a lower level.

Many mergers & acquisitions of medium-sized and small companies

Number of mergers & acquisitions in Dutch construction companies by company size in employed persons per year

Opportunities and risks of mergers and acquisitions

A merger or acquisition is an important financial and strategic decision for a company. The decision must, therefore, be well-considered. A merger or acquisition must strengthen the performance, profitability and continuity of a company. However, it does not only have advantages. There are also risks. Each sector, and therefore also the construction sector, has its own specific characteristics that make mergers and acquisitions more or less successful. We discuss the opportunities and risks for construction companies below.

Business succession through a merger or acquisition

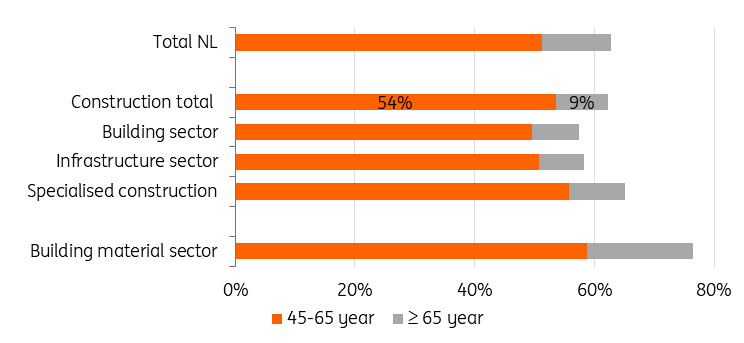

Older entrepreneurs often sell out and use the proceeds as a pension provision. A higher age of entrepreneurs can, therefore, be a stimulus for more mergers and acquisitions. 9% of construction entrepreneurs are 65 years or older and 54% are between 45 and 65 years old. This is roughly equal to the average entrepreneurial age in the Netherlands. A relatively large wave of sales of construction companies due to ageing and business succession is, therefore, likely to be limited in the coming years. The building material industry is an exception. There, entrepreneurs are relatively older than the average in the Netherlands and, as we saw above, relatively many companies are sold there.

Age of Dutch construction entrepreneurs on average

Share of entrepreneurs by age (excluding self-employed persons), 2021

Buying scarce resources such as building land and/or staff

To secure critical resources such as building land or (specialised) personnel, construction companies can buy other construction companies. For example, construction company Heijmans took over the construction and family business Van Wanrooij this summer. For Heijmans, this deal is attractive because of, among other things, the large land portfolio of Van Wanrooij, which guarantees their construction activities and housing production (more). For Van Wanrooij, business succession also played a role.

Private equity often brings more financial discipline

Acquisitions by private equity parties not only bring capital to invest, but often also extra financial discipline. As a result, more financial indicators are used and less quickly chosen for specific construction technical prestige projects that are often risky. This can reduce the risks within the company, improve the financial performance and better safeguard the continuity.

Risks of a merger or acquisition

To fill the staff shortage, construction companies choose sometimes to buy an installer so that they are assured of a certain required installation capacity. However, in addition to the benefits of capacity assurance, there are also risks:

-Companies that merge sometimes have (clashing) cultural differences.

-Integration of two companies often leads to time-consuming and complex processes.

-Buying a well-running company with highly qualified staff often comes with an expensive price tag. When deciding to buy another company, it must be clear what additional added value the acquisition offers for the buying party compared to the (market) price to be paid. Synergy benefits should not be overestimated.

-Customers are not always loyal when a company changes due to an acquisition. Clients were used to a certain service and working method and if that changes, then some (regular) clients can walk away because their wishes no longer match the services provided.

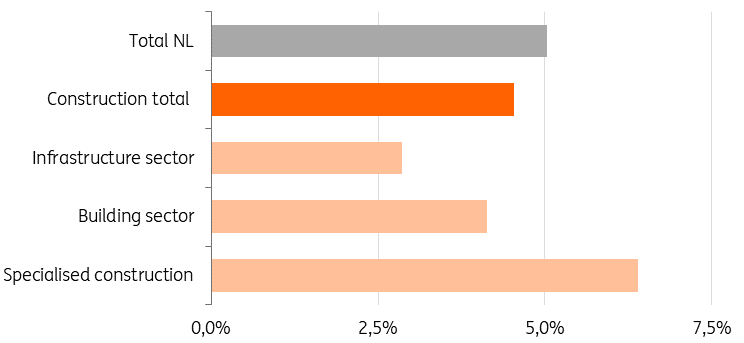

Low profit and cyclical sensitivity

The profit margins of construction companies are relatively low and the demand for new construction is very volatile and dependent on economic developments. The margins are low, especially in the infrastructure sector. In the specialised construction sector, the profits are on average higher and the prospects better. Acquisitions therefore also occur more often in the specialised construction sector.

Profit low in infrastructure sector but high in specialised construction

Profit indication: Average net result as % of the balance sheet total, 2011-2021

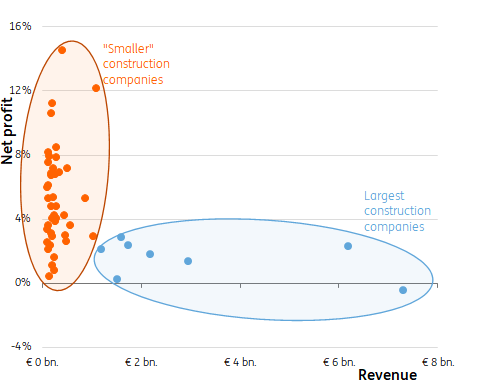

Limited value creation via buy-and-build strategy due to few scale advantages

Private equity investors often create value by a buy-and-build strategy, whereby several companies are acquired. The larger the newly merged company becomes, the higher the acquisition factor (multiple arbitrage) often is that another company or investor is willing to pay. Scale advantages play a role in many sectors. Due to the (so far) limited industrialisation in construction, scale advantages are limited for many contractors. The largest Dutch construction companies therefore also do not have higher profit margins on average. Among the 50 largest construction companies, there even seems to be a slight negative correlation between the size of a company and the net profit.

Largest Dutch builders do not make relatively more profit

Ratio of net profit (average 2019-2021) and 2021 turnover of 50 largest construction companies

But buy-and-build can be profitable

Despite the fact that scale advantages are often limited in construction, some investors still often like to buy large construction companies. We see this especially happening in the maintenance market (see below). Keeping one relatively large construction company in their portfolio saves them a lot of monitoring costs. Private equity parties can provide this by merging different construction companies and bringing them under one holding and then (after a few years) selling them on for a higher multiple. Despite the fact that there are few synergy benefits in the business operations, value is created in this way (for the ultimate buyer).

An acquisition can be an investment impulse

An acquisition by a capital-rich private equity party can provide an investment impulse in the construction company. For example, HAL Investments took over the Dutch construction company Van Wijnen in 2020. HAL can provide extra capital for further investments in efficiency. It steps in with a real long-term plan. Investments can, therefore, be made in trends such as digitalisation, industrialisation and sustainability. This can lower the (variable) costs of the construction company and make it more profitable. Especially industrialisation requires considerable up-front investments. We will also discuss this in the next part of this publication.

Consequences of trends in digitalisation, industrialisation and more renovation

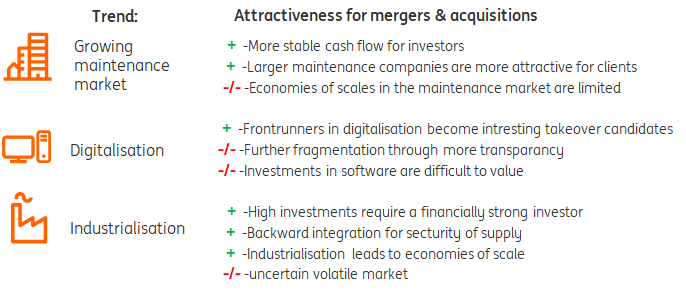

Trends and developments in the construction industry can lead to more or less mergers and acquisitions. We discuss here three important trends in the construction industry and the consequences that these trends can have for mergers and acquisitions. There are also trends that can be both positive and negative for the development of the takeover market in the construction sector. We will see that especially the growing maintenance market is currently interesting for acquisitions.

Impact of construction trends on mergers and acquisitions:

More maintenance

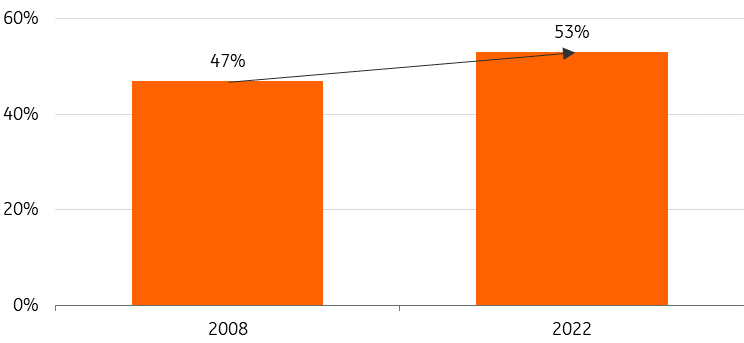

The maintenance market is growing

The share of the renovation and maintenance market in the construction industry has steadily increased in recent years. In 2008, 47% of the building sector consisted of renovation. This share rose to 53% in 2022. We expect the renovation share to increase slowly as the need for energy-efficiency measures increases.

Share of renovation increases slowly in the building sector

Renovation share of total Dutch building production

Few economies of scale but size still important

The maintenance market is very fragmented because there are few economies of scale to be achieved. Projects are often relatively small (especially for consumers) and each project is often different, making industrialisation difficult. Mergers and acquisitions therefore do not or hardly increase efficiency. However, a minimum company size is more and more important because large customers such as housing corporations are increasingly looking for larger solvent parties with whom they can enter into long-term maintenance and sustainability contracts. Private equity can link different maintenance companies (with specific disciplines) together by buy-and-build.

A more certain cash flow for investors

The advantage of the maintenance market is also that it is less volatile than new construction. An increase in the share of the maintenance market makes the construction sector more attractive for investors because it provides a more stable and predictable cash flow.

Digitalisation

Digitalisation makes the construction sector more transparent

Further digitalisation can make it easier for construction companies to exchange data with each other and this increases the transparency. Digital marketplaces ensure that construction companies, subcontractors and suppliers can easily find each other and exchange data quickly. This can lead to further fragmentation of the sector due to the increasing transparency in the market. It is then less necessary to have certain processes 'in house' if they can also be easily purchased externally.

Investments in digitalisation difficult to value

Business investments in digitalisation can increase the efficiency of the company, but these intangible assets are often also difficult to value during an acquisition. Self-developed software of a company can often not be sold because it is often very company specific. This makes acquisitions of digitalised contractors also more difficult and complex, although it can also be an interesting acquisition candidate because they are frontrunners.

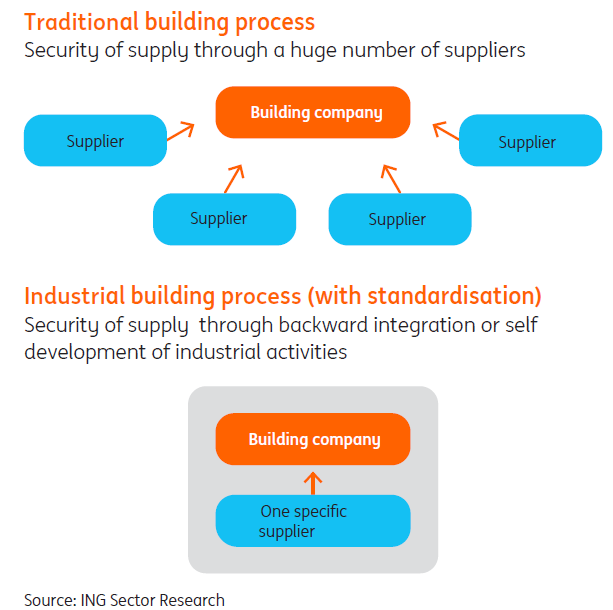

Industrialisation leads to backward integration

Supply security through backward integration

Industrialisation can speed up the construction process, especially for new construction, at lower construction costs and with less staff. However, there are also disadvantages that mainly limit the flexibility of construction companies. With traditional construction, supply security is achieved by choosing from different suppliers. However, if contractors switch to industrial construction and work with fixed (company) standards (standardisation), construction companies also become more dependent on specific suppliers. Supply security of these specific products is then essential and to achieve this, construction companies quickly start producing these (prefab) building materials themselves or take over a supplier (or vice versa). For example, think of car companies that also want to produce batteries themselves because that is a very essential part of the business process of electric cars. For houses, this could be the technical installation, for example. With industrialisation, this is often put in one specific essential module. Industrialised builders therefore often want to have this process in their own hands or set up a form of far-reaching cooperation for this.

Changes of supply change due to industrialisation

Scale enlargement through industrialisation

Industrialisation pays off especially with large numbers in new construction, because efficiency advantages are achieved, putting smaller construction companies under pressure. Large industrialised construction companies build cheaper and thus attract an increasingly larger market share at the expense of the smaller construction companies. Further industrialisation in construction can therefore result in scale enlargement.

Construction trends continue to stimulate takeovers

All in all, it seems that especially the growing maintenance market but also industrialisation continue to stimulate mergers and acquisitions. Since these are long-term trends, we also expect that they will remain driving forces behind the number of mergers and acquisitions of construction companies in the coming years.

With thanks to:

Mirjam Anderson, IRIS Corporate Finance, Dominique Baltussen, IRIS Corporate Finance, Nick de Man, Marktlink, Michiel van der Meij, AXECO Participaties, Jeroen Beets, ING Wholesale Banking, Jan van der Doelen, ING Sector Banking, Bart de Klerk, ING Wholesale Banking, Marcus Looijestijn, ING Business Banking

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more