Consolidation in Dutch IT services: Slowing but not stopping

- 15 June 2023

- TMT The Netherlands

M&A activity in the Dutch IT services sector has soared in recent years. Investment opportunities, financing conditions, and an increase in optimal scale have all been key drivers of this trend. As interest rates continue to rise, consolidation will slow but remain resilient

The Dutch IT services sector is consolidating quickly

M&A activity in the Dutch IT services sector has more than doubled in the past six years. This increase was driven by three main developments.

Client demand

An increase in optimal scale for both small and large companies. Client demand has increased the minimum viable scale for smaller companies and further incentivised larger corporations to become a one-stop shop for their customers.

Elevated growth

Second, the sector has shown high growth and is characterised by recurring business models which make it an attractive sector to investors.

Lower interest rates

Third, lower interest rates made it an attractive time for M&A due to relatively low financing costs and high multiples. As financing conditions tighten, M&A activity in the sector will not continue to grow at the same pace as the past years, but consolidation will continue.

The Dutch IT services sector has become increasingly engaged in M&A in recent years. From 2017 to 2022, the number of M&A deals in the sector increased from 290 to 620, resulting in an annual growth rate of roughly 16.5%. The Dutch economy as a whole experienced a 12.5% year-on-year growth rate of M&A in the same period.

Low interest rates caused high multiples, which made for interesting sales – and coupled with the fact that many IT entrepreneurs started their companies in the 1990s, many saw this period as a good time to sell. The increase in M&A activity within the sector is partially driven by lower interest rates, but also by the attractiveness of the sector to investors and increases in required scale. We delve into this in more detail below.

M&A deals in IT services increased significantly over the last 6 years

Number of M&A deals in the Dutch IT services sector

Attractive investment opportunities

The IT services sector is characterised by recurring business models and high levels of growth in recent years, both of which make it an appealing area for investment. After an initial dip in revenues, the Covid-19 pandemic accelerated the adoption of digital products and services. While these effects do appear to be fading, the sector is still reaping the benefits as the demand for the outsourcing of IT services, IT infrastructure and software subscriptions remains high.

The move to the cloud, data centres, and the development of new IT services such as data and cyber security have also led to extra demand for Dutch IT. As a result, the sector has shown sustained revenue growth, totalling 9% YoY in 2022. The recent contraction we've seen was mainly driven by a decline in investment in IT equipment, and therefore shouldn't deal too much of a blow to the bigger picture.

The IT services sector displays sustained revenue growth after the pandemic

Private equity contributions

Given its attractiveness to investors, it's no surprise that the sector is one in which private equity is very active. So much so that from 2020 to 2022, 52% of deals were backed by a private equity fund. Private equity-backed companies tend to follow one of two M&A strategies: integration and buy-and-build. The strategy followed partially depends on the investment horizon of the private equity fund in question.

In an integration strategy, not only are the back-end systems of the acquiring and target companies combined, but their processes and operations are also incorporated into one company following one strategic direction and brand. This strategy is followed by Arcus IT, Hallo and Rapid Circle. In the short term, integration takes more time and effort and consumes more resources from companies involved in the deal. However, in the long term, it makes it easier for companies to maximise their service proposition towards clients using cross and upselling.

In a buy-and-build strategy, only the back-end systems tend to be integrated while the different brands and company names are kept, bundling the knowledge and expertise from various companies under a business group. This is the case for Interstellar Group, Total Specific Hosting and Broad Horizon. Through this strategy, firms take advantage of the market tendency of assigning higher valuations to larger companies and benefit from multiple arbitrage*, without making many material changes.

*Multiple arbitrage means that multiples are higher for larger companies than for smaller ones when acquired. For instance, larger company A can acquire smaller company B at 5x EBITDA, but when A is then acquired by even larger company C, it is sold for 7x EBITDA. The EBITDA gained by A from the acquisition of B is an additional profit.

Simply managing digital workspaces is a thing of the past

Changing client demand, commoditisation, and labour shortages have all been important developments in the IT services sector. Clients now ask for a more diverse array of services from their IT providers. Simply managing digital workspaces is a thing of the past.

Customers also demand data and cyber security and the management of IT infrastructure, for example. This changing client demand means that larger companies actively engage in M&A to try to become a one-stop shop for their clients and a partner that helps customers with everything IT-related. This adds value for both the IT service provider and their clients. For smaller IT service providers, however, diverging client demand means that they need more manpower to accommodate their customers. To do so, they actively engage in M&A to meet the minimum viable scale.

Rob Verbeek, founder and CEO of Arcus IT, has seen this development up close in recent years. While he believes there will always be room for smaller companies in the market, he does see that client demand has forced smaller companies to grow.

Labour shortages remain a key challenge

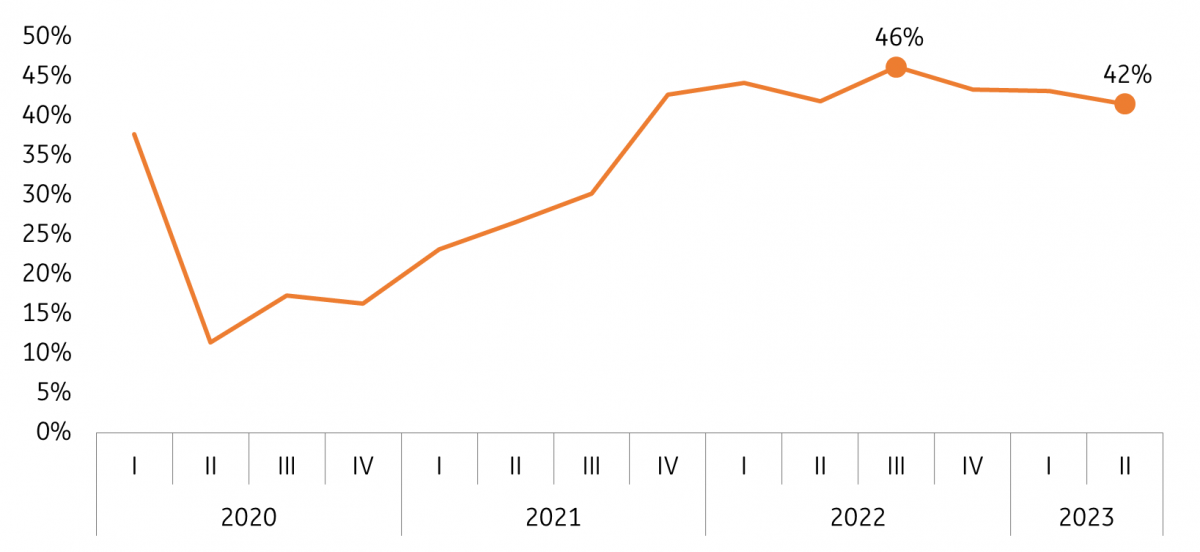

Finding good staff is the main challenge currently facing the IT services sector. The share of Dutch IT service entrepreneurs that believe the labour shortage is the biggest impediment to growth is currently at 42%. This is slightly down from the peak of 46% in the third quarter of 2022, but still very high. The labour shortage further incentivises M&A as it allows companies to obtain skilled IT workers. Arcus IT and Accent Automatisering merged in 2022, naming the scarcity of talented IT employees as an important driver for the transaction.

42% of entrepreneurs see labour shortages as a drag on growth

Percentage of companies that sees the labor shortage as biggest obstacle to growth

M&A activity in the Dutch IT services sector has increased across the board. Engagement from companies of all sizes has risen – but medium-sized companies increased their M&A involvement at a faster pace than their smaller counterparts. Larger companies (of more than 250 employees) tripled their acquisitions from 10 in 2017, and to 30 in 2022. Medium-sized companies (50 to 250 employees) more than doubled their involvement in M&A activity, from 25 in 2017 to 60 in 2022. M&A participation from larger companies has increased by 157% in total over the last six years.

Large and medium size companies more than doubled their M&A involvement

Number of M&A deals in the Dutch IT services, per company size

It's therefore no surprise that the share of large and medium-sized companies in the market is growing at a faster pace than smaller ones. From 2017 until 2022, the number of bigger corporations grew by 67% – nearly three times more than the number of small companies with 10 to 50 employees. This evolution emphasises the consolidation that is taking place in the IT services landscape.

The number of big companies is growing faster than smaller companies

Number of companies in the Dutch IT services, by size

Driving forces

Two other factors that are driving consolidation are commoditisation and margin pressure. IT products have been commoditised in recent decades, as large IT services providers such as Microsoft, Amazon, Google, and SAP have gained a bigger share of the pie in some areas (e.g. office software applications and cloud setups). This in turn has incentivised diversification by IT service providers in the mid-market segment. As a result, many of them have moved into areas such as cyber security and off-premises data centres. This can further drive M&A as companies strive to acquire additional skills and technology, and aim to become more efficient and better equipped to serve their clients.

Further consolidation expected, but the pace will slow

Overall, there is enough space in the sector for consolidation to continue in the coming years. The IT services sector is dynamic and still relatively young, and new value propositions occur often. It's set to remain in high demand as a vital element in the functioning of the economy, as is that for services such as cyber security, data analysis, software integration and automation. Given increasing interest rates and declining multiples, however, consolidation will continue at a slower pace than in the past six years.

Special thanks to

- John Horeman

- Abe Bakker

- Rob Verbeek

- Ludo Baauw

- Marc Visser

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more