Renovation is taking centre stage in the construction sector

- 3 July 2023

- Manufacturing, Construction and Retail

Energy efficiency measures which aim to improve the quality of existing buildings are driving growth in the EU renovation sector. As a result, renovation now accounts for more than half of construction work. We expect that steady growth to continue due to sustainability regulations and high energy prices

The renovation and maintenance market is not glamorous, but it is huge

The renovation sector is experiencing a tailwind at the moment. Due to high energy prices last year, there has been a run on all kinds of energy-saving measures for houses.

The renovation and maintenance (R&M) market is often called the forgotten market of the construction sector. It is fragmented and therefore dominated by small (one-man) firms, less glamorous than new construction and with a lack of data. However, the EU total construction production volume consists of more than half (see below) of R&M activities. This means that the total annual revenue of this sector in the EU is approximately €850bn which makes it an important economic segment.

Important sales channel for building material suppliers

This means that a wide range of (large) building material suppliers are dependent on the R&M market, from manufacturers of insulation materials, wooden building products and chemical companies that produce paint, to suppliers of pipes and cables. Building materials that are not so commonly used in R&M are concrete, bricks and cement.

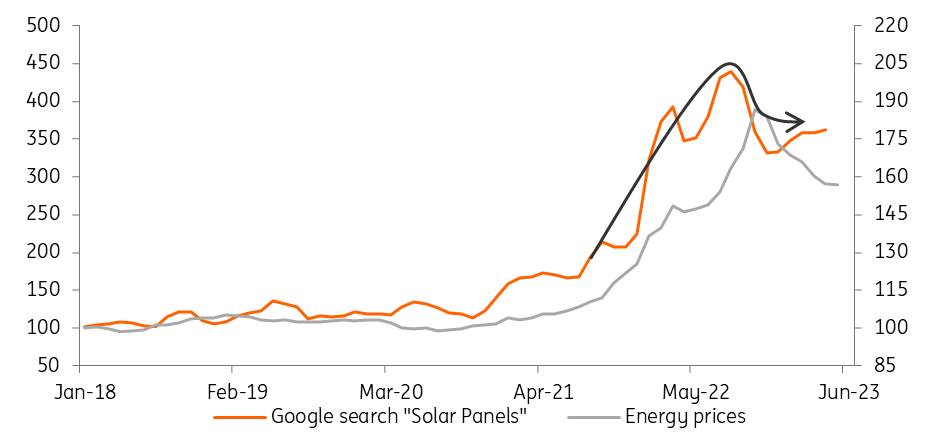

Interest in solar panels slows down after peak demand

Energy efficiency measures such as insulation, insulating glass as double glazing, heat pumps and solar panels are seen as integral parts of the renovation and maintenance market in the construction sector.

Interest in solar panels, in particular, has soared. In many European countries, Google searches for solar panels rose significantly, which suggests purchases did too. In the Netherlands, solar energy production increased by 46% in 2022. This tremendous growth rate benefited numerous installation companies operating in this business.

Since energy prices began to moderate this year, interest in solar panels has slowed although it remains at a high level. So, the craziness in the market has subsided but the price shock has still raised awareness about the importance of energy-saving measures.

Interest in solar panels has decreased but remains high

Development of monthly energy prices (electricity, gas, solid fuels and heat energy) in the eurozone and Google search development for "solar panels" (in local language*) in several EU countries (Index Jan 2018=100)

Source: Google trends & Eurostat, ING Research

">

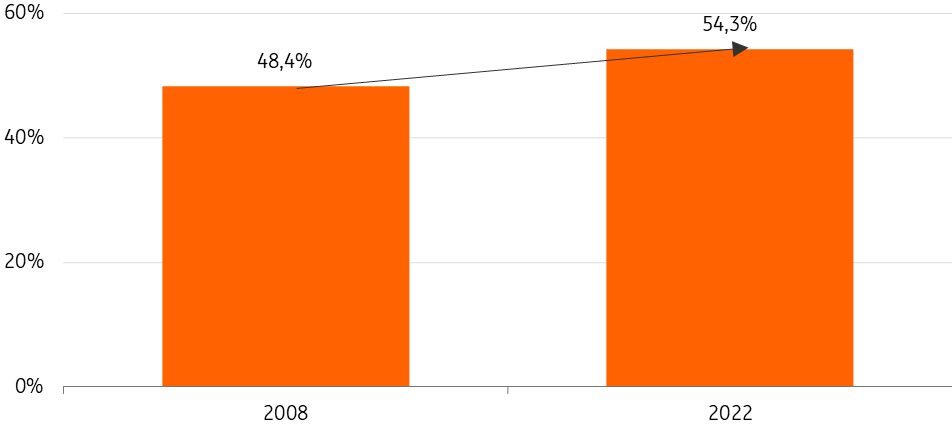

Share of home improvement market increases

The share of the R&M market has steadily increased over the past 15 years. In 2008, 48% of EU production volume consisted of R&M works. This has gradually increased to more than 54% in 2022. When we compare the different subsectors, renovation is the largest in the residential sector. We expect that the renovation share will increase further as the need for energy efficiency measures increases due to high energy prices and sustainability legislation, such as the Energy Performance of Buildings Directive (EPBD IV: see below) which aims to ensure a higher sustainability rate.

Share of renovation increases slowly in the building sector

Renovation share of total building production

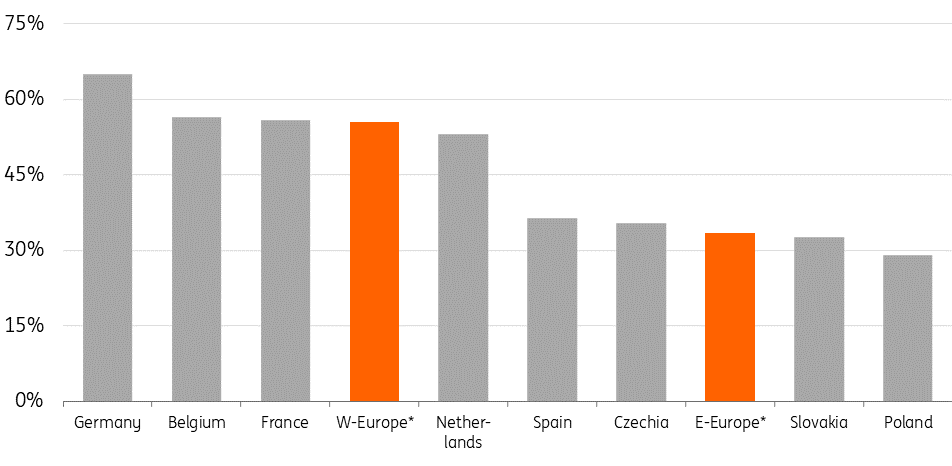

Share of R&M differs

The share of the R&M market varies among countries. Typically, countries with a higher GDP per capita have a relatively larger R&M market. There are several reasons for this:

- Less developed countries are often catching up and therefore they are investing heavily in new buildings and infrastructure. That results in a relatively lower share of R&M.

- Well-developed countries often have a larger stock of older buildings and infrastructure that requires regular maintenance and renovation. As structures age, they need repairs, upgrades and modernisation to ensure safety, functionality and efficiency.

- Developed countries typically have stricter building codes, safety regulations and environmental standards. Compliance with these regulations often requires periodic upgrades and renovations.

This narrative holds true for Europe, resulting in relatively higher renovation shares in Western European countries. There, the renovation market is approximately 55% of the total building volume. In Eastern Europe, where there is still a lot of catching up (new building) being done, the renovation sector has a smaller share of the total construction output (approximately 33%).

Share of renovation market is higher in Western Europe

Renovation share of total building production, 2022

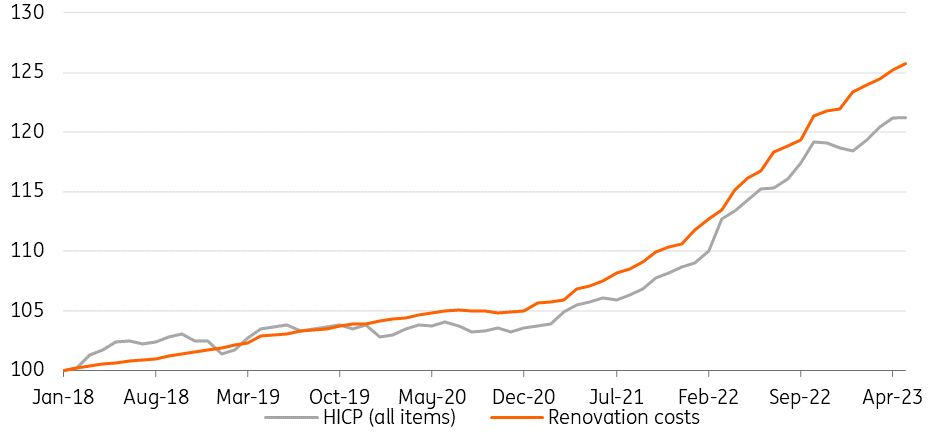

Renovation costs on the rise

In recent years, the cost of house improvements has increased, surpassing the inflation rate in the European Union. In addition, energy prices have seen an even greater increase, making energy efficiency measures still more financially beneficial than they were in the past.

Costs of house improvement slightly higher than inflation

Monthly price development of all consumer goods (HICP) and renovation (maintenance and repair of dwellings) eurozone, (Index Jan 2018=100)

Optimism remains

The R&M market is likely to show future growth driven by sustainable and energy-related factors. Many governments support sustainability measures, and high energy prices act as an extra trigger.

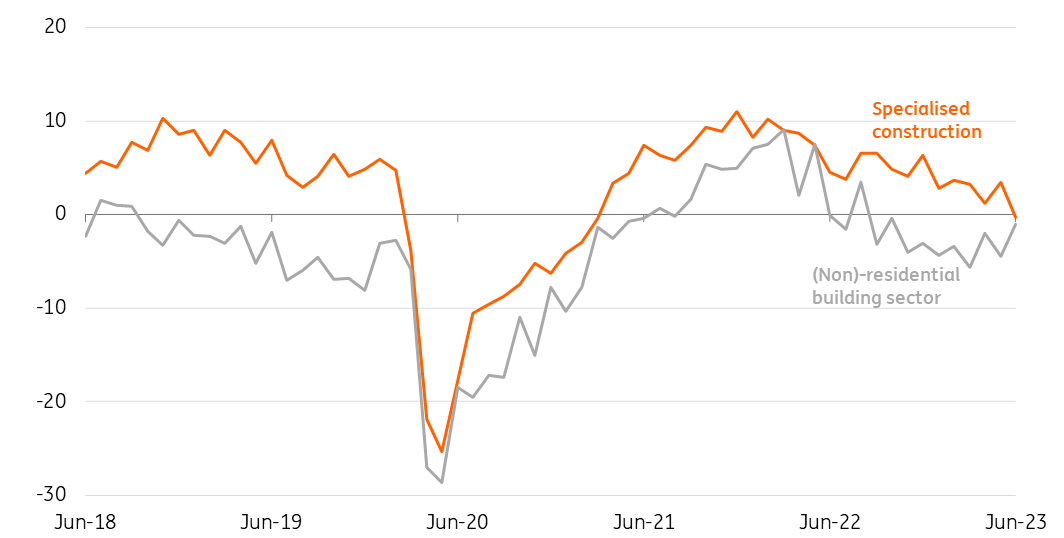

As mentioned above, R&M data are often scarce. However, we can look at the specialised construction sector to know how the R&M market is currently doing. This subsector consists of many construction branches that are active in R&M, such as installation, plasterers, carpenters, painters and glaziers. The data are a bit blurred as many of these companies are likewise also active in the construction of new buildings. Nevertheless, if we consult the EU construction confidence indicator, we see that specialised construction companies have been optimistic for a long time. In June it was a bit lower, but still neutral and not negative. Whereas the confidence of companies in the building sector as a whole has been in negative territory for almost a year.

Confidence indicator neutral in specialised construction

Development EU confidence indicator

New EU regulation EPBD IV will be a structural growth driver

The European Union has set a goal of achieving climate neutrality by 2050. To reach this target, particular attention is being given to buildings. Buildings currently contribute to 40% of energy consumption and 36% of greenhouse gas emissions in the EU. However, the current rate of building renovation in Europe is inadequate to meet the required targets.

To address this, the European Parliament passed a comprehensive revision of the 2010 Energy Performance of Buildings Directive (EPBD IV) in March. This proposal aims to increase the renovation rate by introducing significant changes. One key change involves replacing the existing energy performance certification system with a more comprehensive assessment of a building's environmental performance.

The proposal places a strong emphasis on ambitious targets for renovating existing buildings, including the establishment of minimum energy performance requirements that all buildings must meet within a specified timeframe. However, the scope of the proposal extends beyond merely improving energy efficiency. It also introduces a new certification system for evaluating the environmental performance of buildings throughout their entire life cycle. This certification considers emissions generated during the production of construction and insulation materials, the construction process itself, as well as the renovation and operation of buildings.

These regulations will stimulate the renovation market in the EU, as they will trigger a wave of renovations and create a greater demand for energy-efficient upgrades.

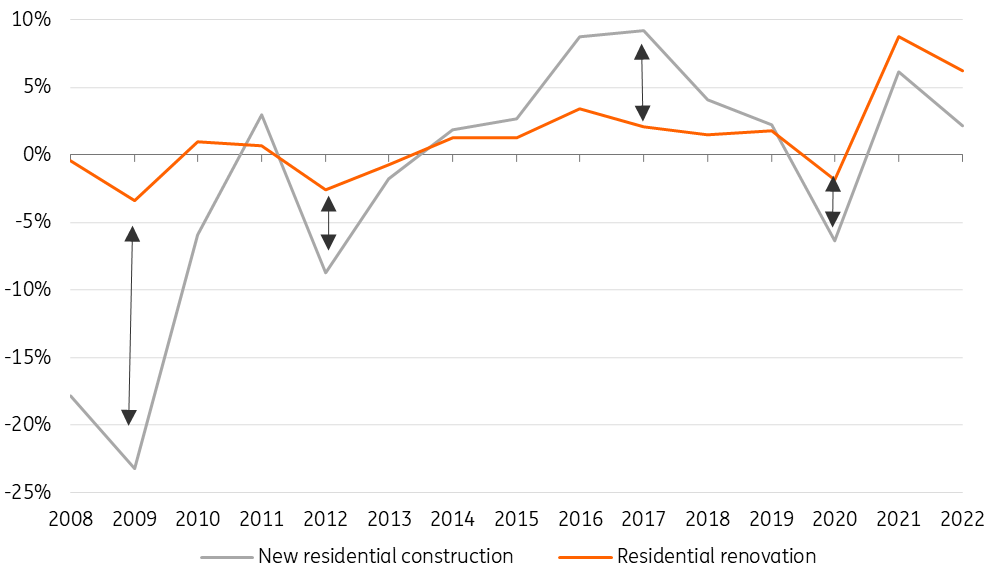

R&M usually less volatile than new construction

The R&M market is less volatile compared to the new construction sector. The market for new construction is highly susceptible to economic fluctuations. For instance, during the financial crisis, the contrast between new residential volumes and renovation volumes became evident. In 2009, new construction projects experienced a significant decline of more than 20%. In contrast, renovation volumes witnessed a much smaller decrease, declining less than 5%.

The demand for R&M is less affected by economic cycles. It is easier to postpone a new building project than the renovation of a leaking roof. Interestingly, during an economic crisis, the demand for R&M may even increase. Homeowners who are unable to sell their houses opt to enhance their existing living spaces to meet their changing housing needs. Consequently, this leads to an increase or can at least sustain the demand for R&M.

Renovation less vulnerable to economic sentiment

Development of production volumes in Western Europe (EC-15), % YoY

Choppy periods for R&M market

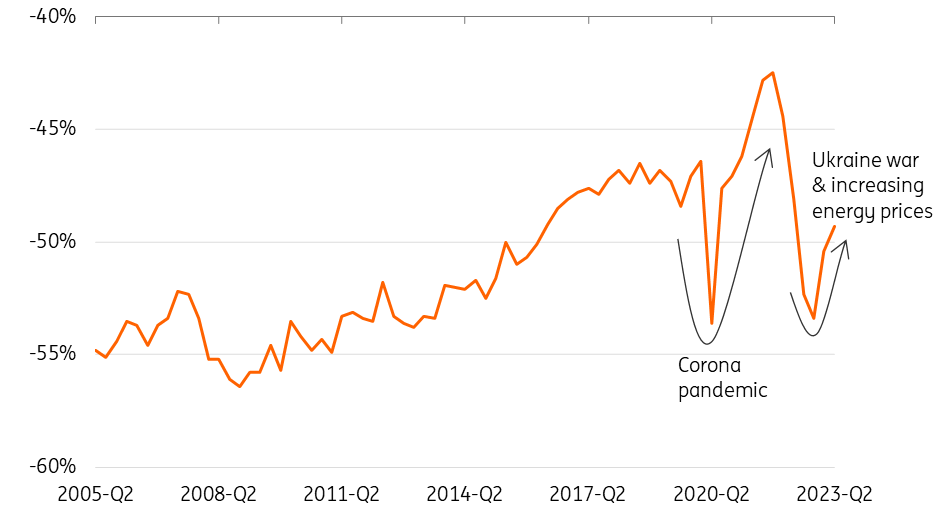

From a historic perspective, demand for renovation and maintenance has recently been remarkably volatile. During the first Covid-19 lockdown, people were reluctant to have handymen in their homes. This gradually changed and demand for improvement grew rapidly in 2021 as many people suddenly required a “home office” as remote work became the norm. In addition, consumers had spare money to invest in their homes as they couldn’t spend their savings on holidays during the pandemic.

In 2022, skyrocketing energy prices (caused by the Ukraine War) decreased consumers’ purchasing power. This resulted in a downturn in the number of people that wanted to refurbish their homes. In contrast, the demand for energy-efficient investments (eg. solar panels, insulation and heat pumps) has grown as the payback period for these refurbishments has dropped enormously. Many governments also offer subsidies for energy-related renovation projects.

Demand for home improvements has been volatile lately

Balance of EU consumers that expect to improve their home over the next 12 months

Stable growth will return in the renovation sector

All in all, despite the temporary circumstances caused by the Covid-19 pandemic and the energy crisis, the trajectory for residential energy efficiency upgrades remains promising. Looking ahead, we expect gradual growth in the renovation market due to sustained government regulations and the structural impact of higher energy prices. Therefore, the demand for residential energy efficiency upgrades is likely to continue its upward trend.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more