CCS growth is set to build as market struggles to kick off

- 29 January 2024

- Energy Sustainability

CCS is a key enabling technology for the transition towards a net zero economy, and we're expecting its growth to continue building momentum in 2024. At the same time, unrealistically high hopes of a rapid kick-off should start to cool down, and upcoming elections in key markets like the US and EU will only add to existing uncertainty

Renewables are not the only answer

Efforts to decarbonise the global economy are starting to reach a turning point as the COP28 climate conference reached agreements to ‘transition away from fossil fuels' and to triple investment in renewables.

But renewables are not the only answer to a net zero economy. Carbon capture and storage (CCS) helps to prevent CO2 from entering the atmosphere and contribute to global warming. Here's what we're expecting to happen with CCS in 2024.

Growth isn't proving as fast as hoped for – or as needed

CCS technologies will continue to gain momentum in 2024. More companies in hard-to-abate sectors are committed to decarbonisation and are aware of the fact that CCS currently is a cost-effective technology for reducing emissions, for example in steel or plastics production. And governments increasingly support CCS.

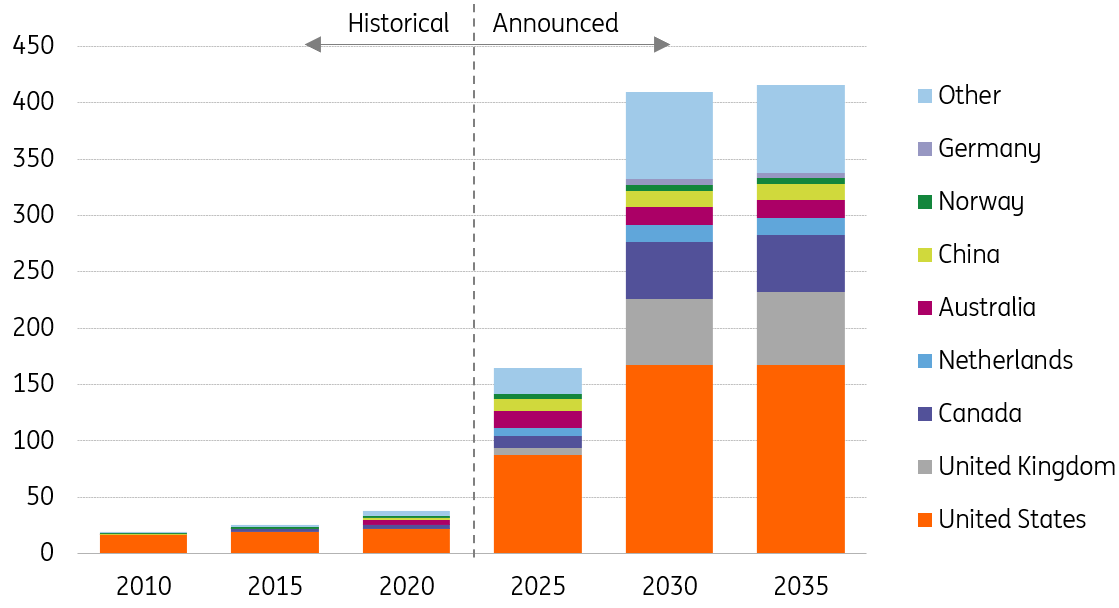

Bloomberg New Energy Finance tracks CCS projects globally and notices an eightfold increase in CCS capacity towards 2030 based on current project announcements. Operational capacity could grow globally from around 50 megatons of CO2 captured per annum (Mtpa) to 165 by 2025, and just over 400 by 2030 – provided that all announced projects follow through.

And that’s the pitfall of forecasting capacity growth in this early stage CCS market. Not every announcement has the same status. Many announcements are about ‘drawing board projects’, few are about ‘FID-projects’ for which the final investment decision has been made and where construction is already underway, or will start soon.

CCS could grow eightfold towards 2030 if market announcement follow through

Global CCS capacity based in mega tons of CO2 based on project announcements

Given the pitfalls of early-stage CCS market forecasting, it doesn’t make sense to forecast capacity numbers on a yearly basis. Projects take years to develop and their planning often moves back and forth. Therefore, we prefer to focus on the major market developments for 2024. This is what we see happening in the CCS market.

Most action happens in North America and Europe, but regions take different approaches

Countries have very different policy support schemes for CCS. The US provides tax credits, while CCS in Europe benefits from a combination of carbon pricing and direct subsidies. But things can differ greatly even between European countries. In the Netherlands, for example, the project owners take most of the risk with the government providing incentives. The UK, on the other hand, treats CCS projects more as infrastructure projects, with the government bearing most of the risk while offering a regulated return to project owners.

The introduction of the Inflation Reduction Act (IRA) in August 2022 caused a lot of excitement for CCS in the US. Now, almost one and a half years later, optimism has cooled as most of the nitty gritty details still need to be worked out by understaffed government bodies. As a result, application processes are long and cumbersome, and that makes project owners wary about making final investment decisions.

Furthermore, the IRA is not very popular among Republicans, even in red states like Texas that benefit most from it. Tangible success in terms of smoother application processes and more FID-decisions would help prop up its popularity, but are unlikely to come soon – at least not before the start of this year’s elections.

CCS costs differ significantly

Projects differ widely in the cost to capture, transport and store CO2. This can range from €80 to €150 or more per ton of CO2 depending on how easy it is to capture (pre-combustion versus end of pipe solutions), where it is stored (onshore versus offshore), how it is transported (pipelines or ships) and what storage facility is used (depleted gas field or aquifer).

Still, even the higher cost range for CCS is relatively cheap compared to other technologies designed to reduce CO2 emissions, such as substituting fossil fuels with hydrogen or electricity. And it provides the opportunity to quickly reduce emissions from large emitters, which benefits the climate in the short term. Demand for CCS storage is therefore growing and outpacing storage supply at the moment. Storage capacity is likely to continue to be a scarce resource for large emitters in 2024 and beyond.

Hubs are reducing costs, but do not benefit every company equally

Most of the activity centres around CCS hubs are built to create economies of scale and reduce costs. CCS hubs are located around established industrial clusters. Prime examples are the Porthos and Aramis projects in the Netherlands, the East Coast Cluster and Acorn Cluster in the UK and the Alberta Carbon Trunkline in Canada. Oil companies in the US – primarily in Illinois and the Gulf Coast – are building offshore CO2 storage hubs. Indonesia and Australia are doing similar things in their region. These hubs involve multiple stakeholders and industries, and sometimes several countries or states.

While these hubs are important enablers of sizeable emission reduction from industrial clusters, awareness is increasing that not every industry benefits from these clusters. Cement and waste incineration plants, for example, are often much more dispersed over the country and many cannot easily be connected to a CCS hub – but CCS is often the only technology available for reducing emissions from these activities. It takes more time to connect these remote sites through pipelines. Alternatively, more expensive CO2 transport modes need to be developed (for example, by truck) for these sites to reduce emissions soon in order to reach national reduction targets.

Not a large banking market yet

Finance mostly comes from capital rich project sponsors like oil and gas majors (Chevron, ExxonMobil, Shell, PB, Equinor, TotalEnergies, AirLiquide), utilities (Gasunie, Ørsted), technology providers (Honeywell, GE) and off takers (ArcelorMittal, Nippon Steel, Baosteel, Ineos, BASF, Linde). They mostly finance CCS projects from their own balance sheets, so there is relatively little debt finance involved in this early stage of the market.

The banking industry is working to increase the bankability of CCS projects, so that these sponsors might be able to refinance in a couple of years and new projects can be financed with bank loans from the start. But a lot of things need to happen to improve the risk return profile of CCS projects.

In the Netherlands, for example, project sponsors remain responsible for carbon leakage to up to 20 years after the closing of the storage facility, which is a significant amount of time even for long term investors.

Second, knowledge on seismic, leakage, and regulatory and permitting risks need to increase in order to improve the public perception on CCS. More success stories need to enter the market to increase confidence and take away concerns from underperforming projects.

Finally, the whole CCS value chain needs to be in place – not only the capturing, transport and storage, but also the policy support and long-term CO2 offtake agreements. And the merchant risk that kicks in the project when the policy support ends after, for example, 15 years, needs to be acceptable for debt financers.

The current CCS players, together with private equity companies, are also active in the M&A market to acquire CCS knowledge or projects, a trend we expect to continue in 2024.

Key developments to watch in 2024

Overall, we expect more activity in the CCS market in 2024, but the market will likely struggle to kick off and show its full potential. But it has to if politicians and corporate leaders are serious about reaching the Paris Goals. Currently only 0.1% of global emissions are captured and stored, so they don’t contribute to global warming. That number needs to increase to about 15% by 2050, according to respected scenarios for a net zero economy by both the International Energy Agency and Bloomberg New Energy Finance. To put it more vividly, the European Union alone will need to capture emissions equivalent to those of Poland and Denmark combined to reach its ambitious 2050 climate targets.

And in the second half of this century, we need a lot of CCS globally to create negative emissions in order to undo the overshoot of global warming that is likely to happen. So, in the long run, the future for CCS could be bright. In the meantime, this is what we’ll be watching in 2024.

Key developments to watch in 2024

Developments that can spur (+) or delay (-) progress in the CCS market

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Energy Outlook 2024: High ambitions, steadier speeds

- This bundle contains 6 Articles