CIS-4: fundamentals and sentiment remain largely positive

- 11 September 2025

- Armenia Azerbaijan

CIS-4 economies remain resilient amid global headwinds. Armenia and Azerbaijan benefit from expected easing in regional foreign policy risks, while Kazakhstan and Uzbekistan enjoy above-expected growth in activity. Monetary policy easing is paused everywhere except Azerbaijan, as inflation risks persist

Armenia: peace process remains key

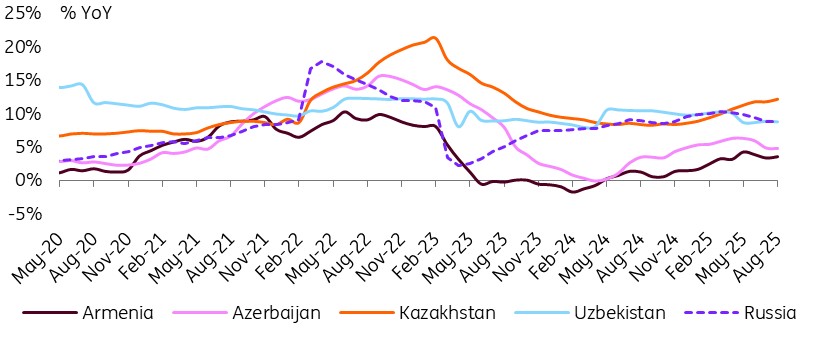

Armenia’s economy is normalising after the 2023-24 surge, with first half 2025 GDP growth at 5.6% year-on-year. However, growth is gradually decelerating despite robust lending and a widening fiscal deficit (4.0% of GDP as of mid-2025), highlighting underlying fragility. The central bank has held the policy rate at 6.75% since February as CPI remains above the 3% target and is trending higher, even with a strong dram.

The peace declaration with Azerbaijan could become a major positive for sentiment, but its economic impact depends on implementation. Optimism around the peace process may unlock investment inflows and support the dram, but fundamentals point to vulnerability: the 12-month rolling trade deficit is around 15% of GDP as of mid-year, while net remittances have dropped below 5% of GDP.

Azerbaijan: focus on a shrinking trade balance

Azerbaijan’s economy is under pressure in 2025, with GDP dropping by 2.3% in July after showing a modest 1.5% YoY increase between January and June, as momentum weakens after a strong 2024 despite a supportive fiscal and credit stance. The budget surplus narrowed to 2.6% of GDP, while retail lending remains high. The central bank cut its policy rate to 7.00% in July and maintained it in September, focusing recent communication on FX market flows.

The manat remains pegged at 1.70/USD and is expected to hold throughout 2025. Moody’s upgraded Azerbaijan to investment grade in July, citing improved buffers and normalised Armenian relations. However, the shrinking trade surplus ($1.8bn vs $5.5bn in 2024) is a key risk if oil prices remain weak.

CPI risks persist in the region, especially in Kazakhstan

CPI growth by country (% YoY)

Kazakhstan: activity and inflation are looking up

Kazakhstan’s economy is outperforming, with GDP growth accelerating to 6.2% YoY in the first half of 2025, led by construction and domestic trade. However, inflation is rising sharply, reaching 12.2% YoY in August from 8.6% at the end of 2024. The central bank kept the base rate at 16.5% in August but signalled a higher likelihood of a rate hike due to persistent demand-driven pressures, recent tenge weakness, higher tariffs, and a planned VAT hike in 2026. Fiscal consolidation credibility remains a key watch factor.

The tenge has stabilised after summer weakness, with expected government FX sales in September providing near-term support. Still, a widening current account deficit ($2.8bn in the second quarter) and increased net capital outflows pose medium-term risks.

Uzbekistan: keeps benefitting from global uncertainties

Uzbekistan remains the region’s growth leader, with GDP growth rising to 7.5% YoY in the second quarter, driven by robust domestic demand and strong exports. However, it is uncertain if this momentum will persist in the second half of the year. Inflation stayed elevated at 8.8% YoY in August but appears manageable for now, helped by recent gold-driven appreciation of the soum and ongoing fiscal consolidation efforts.

The central bank has held the refinancing rate at 14.00% since March. Upcoming policy decisions will weigh on whether to hold versus cut rates, with much depending on how quickly inflation trends toward the long-term 5% target – a goal that still looks distant given current dynamics and persistent price pressures.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Europe’s summer of disillusionment

- This bundle contains 16 Articles