Energy shock reshapes growth and policy outlook in CEE

- 15 May 2026

- Czech Republic Hungary

Poland remains relatively resilient, while the Czech Republic and Hungary face mounting pressure as the energy shock deepens. Growth is set to slow, inflation risks persist, and central banks remain cautious

Poland: Resilient to the energy shock, with rate hikes a remote scenario

The Polish economy continues to outperform the rest of the CEE region and the EU average, despite a weak manufacturing sector, with growth driven by services. Economic growth was subdued in the first two months of the year but rebounded strongly in March, due to companies and households stockpiling ahead of potential supply chain problems or price spikes. On an annual basis, GDP growth in the first quarter was only slightly below the 4.1% year-on-year rate recorded in the fourth quarter of 2025. We expect the negative impact of the Middle East conflict on activity to become more visible in the second quarter, but for the year as a whole, we still expect 3.4%, only marginally below our pre-war expectations of 3,7% YoY.

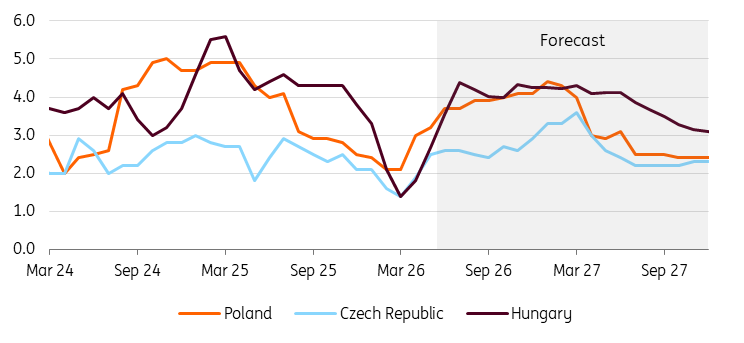

The National Bank of Poland left policy rates unchanged in May, maintaining a wait-and-see approach, but the bias has become more hawkish and President Adam Glapiński stated that monetary policy could be tightened if inflation rises above the upper bound of acceptable deviations from the target (3.5%) and if projections point to inflation remaining above this threshold over the medium term. This makes the July NBP staff projection an important milestone for future monetary policy decisions. We expect inflation to rise above 4% in the second half of this year, but to decline markedly in the second quarter of 2027. Accordingly, our baseline scenario assumes no change in interest rates this year.

The S&P held the rating outlook flat, despite previous downgrades by Moody’s and Fitch, as the GDP outperformance, the balanced current account (only 0.9% of GDP deficit) and low private debt offset rising public debt. That, together with the approaching inflow of the Recovery and Resilience Facility (RRF), which is nearly PLN100bn in grants and loans, and SAFE loans, is helping to stabilise the PLN exchange rate against the euro. At the same time, FI investors continue to price in possible monetary tightening ahead, reflecting inflation risks.

Headline inflation forecast (%)

Czech Republic: Keeping cool as the supply shock starts to bite

We are lowering our economic growth outlook to below 2% this year on the back of a soft 1Q26 GDP reading and the extension of the Middle Eastern conflict. Our base case scenario assumes that Brent crude prices will hover above US$100/bbl until the summer ends and then recede to reasonable levels just above $80/bbl only at the start of 2027. With no end in sight to both the blockade of Hormuz and the war in Ukraine, the elevated uncertainty will alter investment plans and ultimately weigh on the propensity to spend as energy bills are expected to rise. We take the position that negative effects on economic activity will emerge sooner or later, though it is hard to say when exactly things start to give in and crumble.

The Czech economy entered the negative external supply shock at a rather convenient point, and under our base case scenario, we do not expect headline inflation to move significantly higher for long, despite the impact of elevated energy prices and second-round effects.

We see inflation peaking early next year, violating the 3% upper bound threshold just for a couple of months before receding to the target. Deeming this price level surge as transitory and keeping in mind the risks to economic activity, which can be hard to assess ex ante, the appropriate reaction of monetary policy is to keep rates unchanged for as long as possible. This way, you can gauge how the negative effects ripple through the economy, you avoid the risk of pushing it over the cliff, and you don’t rush into a monetary policy mistake through premature rate hikes.

Hungary: A new chapter but the same challenges

About a month ago, Hungarian voters decided to open a new chapter in Hungary’s history book. The dust has settled somewhat since then, but the optimism remains. However, it seems that it is not just pure hope. We have seen a lot of positive data lately. GDP growth in the first quarter was relatively sound, especially compared to the stagnation seen in the past three years. While we are still waiting for the details, we suspect that consumption is behind the strong performance. Although the figure was in line with our expectations, we have revised our forecast GDP growth downward to 1.5% in 2026 due to higher energy prices. However, in all fairness, the toughest part of the energy and supply shock for the economy is yet to come.

Hungary’s inflation continued to accelerate in April. However, the latest figures are a clear positive surprise, given that we have now entered a third month of energy price shocks. Despite all the unknowns, we still anticipate an average inflation rate of around 3.0-3.5% this year. With price pressure peaking at around 5% at the end of this year and in the early part of next year, we can't see a clear path towards an interest rate cut by the National Bank of Hungary. Even if the strong investor appetite towards Hungarian assets remains in place, we struggle to see how the forint can emerge unscathed if the European Central Bank hikes rates and markets turn more hawkish on the Federal Reserve.

Nevertheless, the forint should continue to appreciate and yields should keep grinding lower if positive headlines about EU funds, institutional changes, fiscal policy or foreign policy emerge from time to time.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

ING Monthly: Two anniversaries, one uncomfortable mirror

- This bundle contains 13 Articles

Included in the following ING Monthly

Two anniversaries, one uncomfortable mirror