Asia week ahead: Rate decision in Korea and key data from Japan, China, Taiwan

- 22 May

- Asia week ahead China Japan

South Korea will announce a rate decision as global inflation pressures intensify. Key data releases include Japan's inflation and unemployment, China's industrial profits and Taiwan's output

Asia Research highlights of the week

Bank Indonesia’s big hike to steady Rupiah, not reverse weakening trend

Japan’s inflation slowed unexpectedly, but BoJ still likely to hike rates in June

Japan’s stronger-than-expected exports support a June BoJ hike

Japan’s stronger-than-expected GDP supports June BoJ rate hike

Asia FX Talking: Renminbi remains beacon of stability

China’s April slowdown highlights dilemma between growth and inflation

China-US relations: what to expect from ‘constructive strategic stability’?

Stronger growth and reflation ease pressure for stimulus in China

South Korea: Bank of Korea may signal hawkish tilt

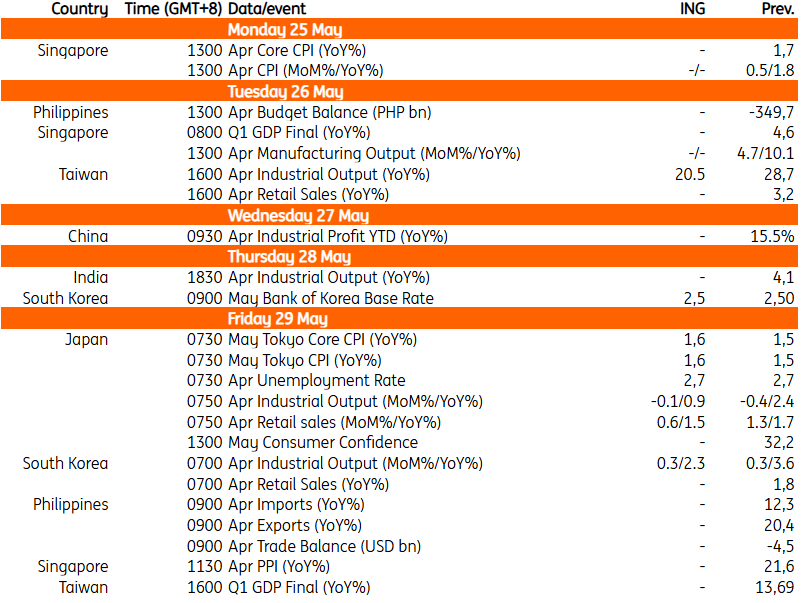

We expect the Bank of Korea to keep rates unchanged on Thursday, but signal a hawkish stance. Dot plots should indicate one or two rate hikes within six months, with the BoK upgrading its own GDP and CPI forecasts. At least one board member may vote for a rate hike at the meeting. Prices are likely to rise soon despite government measures, though the economy appears resilient to energy shocks. The April monthly activity data should support our view. We expect robust chip production to boost overall industrial production, even with lower refinery and petrochemical output.

Japan: CPI to rise modestly amid increasing pressures

Japan’s April CPI data came in surprisingly soft. This is likely due to government measures and one-off fee reductions on education and social welfare programmes. We believe that underlying price pressures continue to build, with the Tokyo CPI expected to rise modestly. At the same time, industrial production is expected to decrease in April due to more proactive inventory management. The latest manufacturing purchasing managers’ index declined but remained above the neutral level. Thus, production should only decline modestly. Meanwhile, retail sales are expected to rise as government subsidies reduce the burden from rising energy and utility prices. Also, a steady rise in wages should work favourably to increase spending.

China: Industrial profits to offer peak at enterprise health

It’s a quiet week ahead for China in terms of macro data. Industrial profits are the only significant data release, scheduled for Wednesday. The April data will be particularly illuminating as enterprises grapple with higher energy prices. Anti-involution measures may have helped support 15.5% year-on-year profit growth in the first quarter. But higher input prices could affect profitability in the months ahead. South Korean media reports that Chinese President Xi could be visiting North Korea next week.

Taiwan: Divergence in growth between sectors

Taiwan publishes its April industrial production data on Tuesday. We are looking for production to moderate slightly from a very strong March reading to 20.5% YoY in April. IP strength has been heavily concentrated in the information & electronic industry, which includes semiconductors and computers. Most other categories have exhibited significantly weaker growth.

Key events in Asia next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more