- Quick take

Japan’s stronger-than-expected exports support a June BoJ hike

- 11 minutes ago

- United States

Japan is displaying some resilience despite energy shocks. Its trade balance remained in the surplus zone, driven by stronger-than-expected exports. Machinery orders were also stable in the first quarter. Recent data, and hawkish remarks from a top BoJ official, raise the odds of a June rate hike

| 14.8% |

Exports (%YoY)Imports rose 9.7% |

| Higher than expected | |

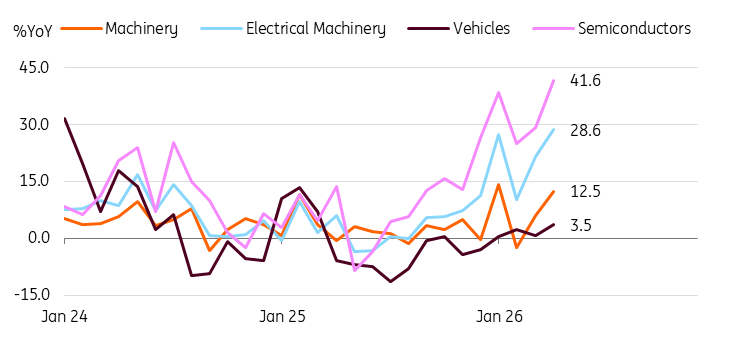

Exports increased for major products and markets, especially to the EU and China

Japan’s exports rose a stronger than expected 14.8% year-on-year in April (vs 11.7% in March, 9.2% market consensus, 11% ING). Major product items such as machinery (12.5%), electrical machinery (28.6%), and transport equipment (6%) recorded increases. By destination, exports to the US (9.5%), China (15.5%), the EU (26.9%), and Taiwan (27.6%) all rose firmly.

The global AI boom and the expansion of power generation facilities are among the main drivers of these strong outcomes. Although Japan is not a leading chip manufacturer, it benefits from strong demand and supply shortages, with exports up 41.6%. Chip exports remained strong throughout Asia, especially to Taiwan and China (88.6%). We expect Asian countries involved in global chip supply chains to continue benefiting from the AI boom.

It’s worth noting that exports to the EU have remained robust throughout the year. There was a significant increase in exports of power-generating machines (up 113.5%) and continued strength in vehicle exports (up 48.2%). We think this is related to the US tariffs on autos. Following the implementation of US tariffs on cars, Japanese exports to the EU grew steadily, while those to the US (-2.3%) stayed weak.

Exports firmly rose in May with notable growth in semiconductors and machineries

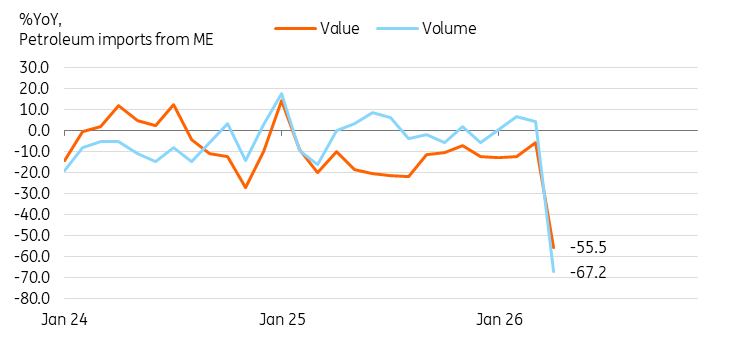

Japan increased US energy imports quite sharply, but only partially replaced Middle East supply shortages

Imports also rose 9.7% YoY in April (vs 10.9% in March, 8.5% market consensus), but the rise was modest. We found that despite the higher global commodity prices, the drop in import volumes should lead to a limited rise in imports.

Mineral fuels imports dropped sharply by 19.3%. Within the category, petroleum and LNG imports fall both in value and volume terms. Meanwhile, petroleum spirits and nonferrous metals imports rose 2.0% and 8.4%, respectively, in value terms. Imports of these two products in volume terms dropped by 37.7% and 19.2%. We found that Japan replaced the shortage of Middle Eastern oil supplies partially by US products, with petroleum and petroleum product imports rising 118.2% and 356.5%, respectively.

The overall decline in imports of essential materials, coupled with rising prices, is expected to adversely affect production levels in the coming months and to increase inflationary pressures.

Energy imports from the Middle East plunged in May

Machinery orders grew in 1Q26, suggesting a steady capex investment in 2Q26

Core machinery orders dropped 9.4% month-on-month, seasonally adjusted (vs 13.6% in February, -8.4% market consensus), only partially offsetting the strong gain in the previous month. Despite the highly volatile monthly movement, machinery orders grew 6.4% quarter-on-quarter in 1Q26, and 6.6% in 4Q26. We expect the uncertainty surrounding the Middle East to dent the businesses’ investment plans to some extent, but they’re expected to increase capex, mostly in semiconductors and machinery. Also, the Flash purchasing managers’ index remained above the neutral level, suggesting businesses still hold a positive outlook in the near term.

BoJ watch

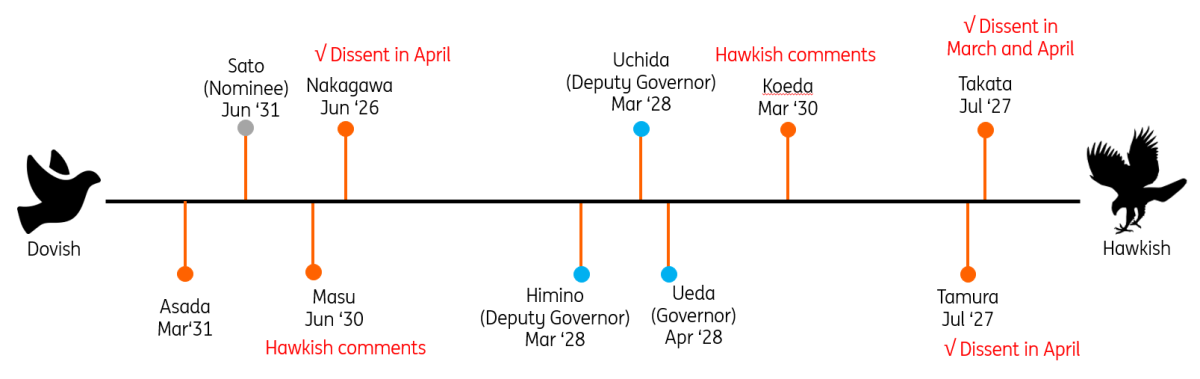

Summing up today’s data, we expect GDP to remain on a recovery path, though the pace of growth should moderate in the current quarter amid energy supply disruptions. We think today’s data support a Bank of Japan rate hike in June. Separate from the data, the BoJ’s board member, Junko Koeda, signalled support for raising policy rates, citing the possibility that underlying inflation may exceed 2%. She is considered a hawkish-to-neutral policymaker. Koeda didn’t cast a dissenting vote in April, but she may do so in favour of a rate hike in June.

Given three dissenting votes by board members at the previous meeting, robust activity data, rising inflationary pressures, and some hawkish comments from BoJ officials, we expect the BoJ to deliver a 25 bp hike in June.

Also, the BoJ will hold a consultation session this week with market participants on the pace of its Japanese government bond purchase operations. The feedback from the session will inform the BoJ’s review of its bond purchase plans at its June meeting. Given the recent sell-off in JGBs, we expect the pace of reduction to slow further. This may give temporary relief to the JGB markets, but it wouldn’t stop long-term JGB yields from moving higher.

Stronger hawkish voices from BoJ officials

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more