- Quick take

- 17 June

- Uzbekistan

Uzbekistan policy rate on hold, but cuts starting to look possible soon

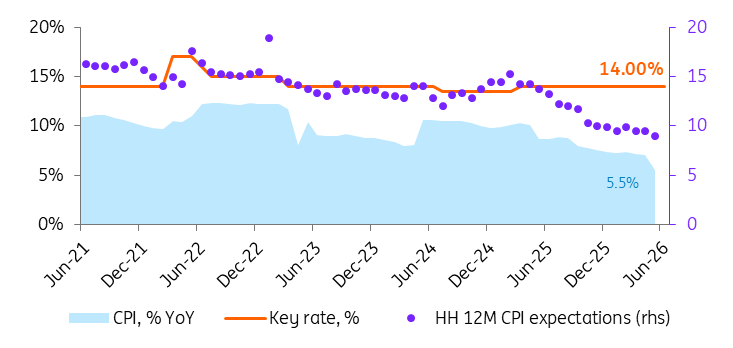

The Central Bank of Uzbekistan kept the policy rate at 14.00%, but the statement struck a softer tone: while acknowledging a number of risks, it shifted from a tightening bias to more conditional easing language. Given our views on the budget, banks, and FX, we see a good chance for a 50-100bp cut in July or September

| 14.00 |

CBRU policy rate, %unchanged |

Still on hold, but the tone softened

The Central Bank of Uzbekistan kept the policy rate unchanged at 14.00%, going against our off-consensus call for a cut. That said, the June statement reads softer than April’s. The CBRU still stressed caution, but the guidance shifted from warning that policy may need to remain sufficiently restrictive if risks materialise to explicitly saying that a sustained decline in inflation expectations, limited second-round tariff effects and a better core inflation outlook would create conditions for gradual easing.

In other words, the current hold should be read as a delay before a cut. The CBRU is not ready to ease into a period of domestic energy tariff hikes and external uncertainty, but it is now more openly describing what would allow cuts to start.

CBRU holds the rate, dismissing the drop in CPI

Why the CBRU chose to hold

The central bank played down the recent decline in headline inflation, arguing that the drop to 5.5% year-on-year in May was largely driven by base effects, especially the waning impact of last year’s energy tariff increase. The unchanged core CPI of 5.7% YoY was one of the key arguments against a cut, in our view. The central bank also warned that the June domestic energy tariff hike will push inflation higher in the near term and could generate second-round effects via transport and production costs.

In addition, the regulator emphasised the still-strong domestic demand, reflected earlier in 8.7% YoY GDP growth in 1Q26. Retail trade, services, tourism and investment were all cited as signs that activity remains robust, while the recent increase in fiscal spending was explicitly mentioned as additional support to demand in coming quarters. Finally, the CBRU reiterated concerns over the external backdrop, pointing to volatility in food and energy prices, higher logistics costs and tighter external financing conditions.

Taken together, this indicates that the central bank is focused on the near-term CPI risks.

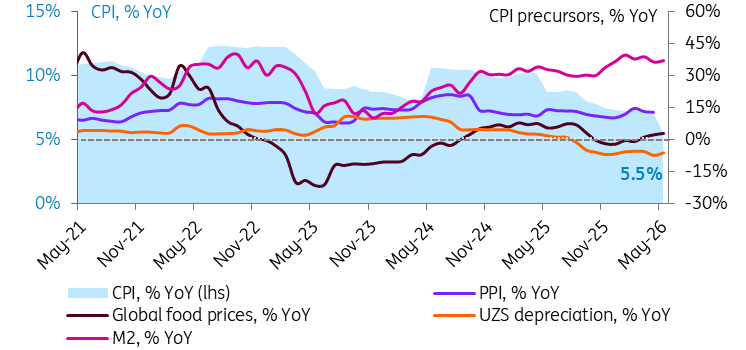

CPI precursors do not provide a strong directional signal

Why we still think a cut could be close

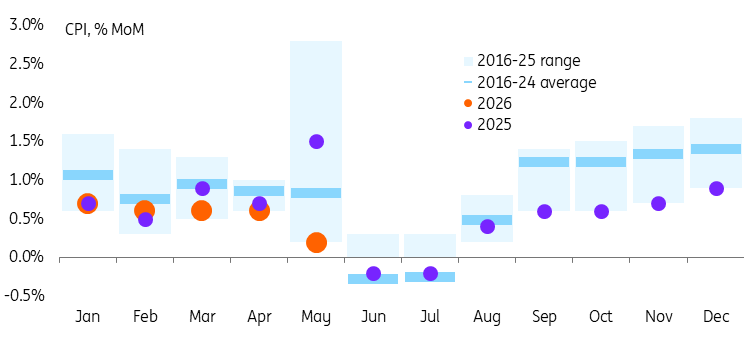

Even so, we continue to think a cut is plausible at one of the next meetings. The main reason is that the inflation picture looks softer than the CBRU’s cautious wording suggests. May CPI rose by just 0.2% month-on-month, the softest May print since 2016, suggesting there is more to the slowdown in the annual CPI than just a shift in the timing of domestic tariff hikes from May to June.

Low CPI in May 2026 was not all about the high base of May 2025

It is noteworthy that the official forecast still points in the direction of lower inflation, with CPI expected to slow from 7.3% at end-2025 to 6.5% at end-2026. We also note that most of the risks highlighted by the CBRU are cost-push rather than demand-led, which does not require a strong monetary policy response.

Cost-side CPI risks could also be limited by the strong currency, which is now supported by renewed gold exports since April and portfolio inflows.

A couple of points on the demand-side CPI factors can also be made.

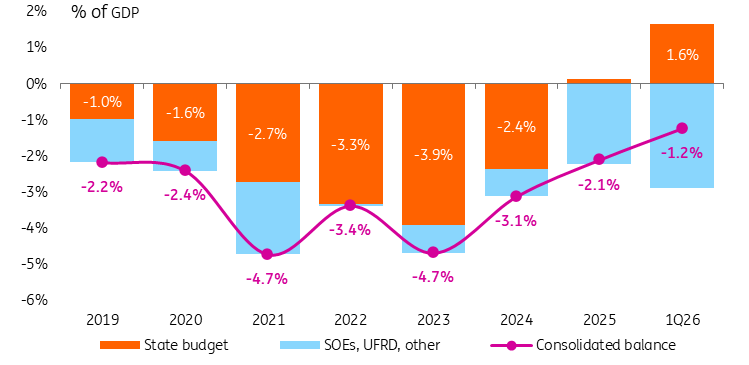

First, given the available fiscal data for the state and consolidated budget, spending growth did indeed accelerate to 27% YoY for the rolling 12 months ending Mar-26, but this growth was still outpaced by 34% YoY respective revenue growth, while the overall 12-month fiscal deficit narrowed materially to 1.2% of GDP, the lowest reading since 2018.

Fiscal balance continues to improve despite elevated spending

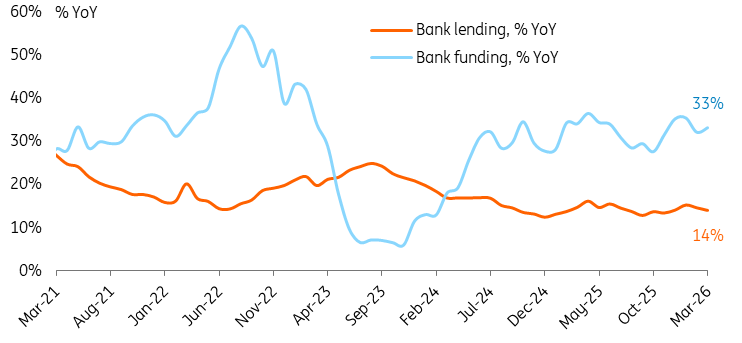

Second, bank lending growth of 14% YoY remained well below the 33% YoY funding growth, and the CBRU commentary suggests this has likely continued into 2Q26.

Sustainable outperformance of bank funding over lending points to a sufficiently tight monetary policy stance

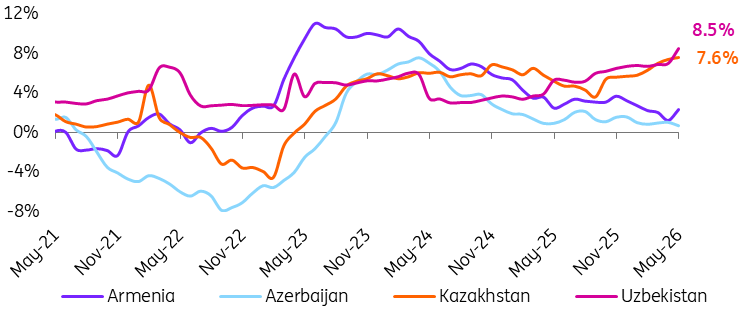

Based on the current CPI, Uzbekistan has the highest real policy rate in the CIS-4 space, at around 8.5%, leaving the CBRU with room to begin a cautious easing cycle without abandoning a clearly restrictive stance.

Uzbekistan has the highest real policy rate in CIS-4 now

What to watch next

Acknowledging domestic cost- and demand-related risks, as well as a somewhat hawkish global context, we now think a 50–100bp cut could be on the table for the July or September meetings. Meanwhile, continued fiscal consolidation and strength in the Uzbekistan som – enabling Uzbekistan's CPI to settle in the 6.5-7.0% YoY range – would be pre-requisites for this scenario.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more