EMEA FX Talking: Hungarian love affair continues

- 15 June

- FX Talking Czech Republic Hungary

Investors' love affair with Hungarian assets continues as the new government talks of euro adoption. Expect the forint to hold gains even though the central bank will be cutting the policy rate. Also staying bid, but on the back of a hawkish central bank, will be the Czech koruna. The Polish zloty should lag, given our view of unchanged policy rates this year

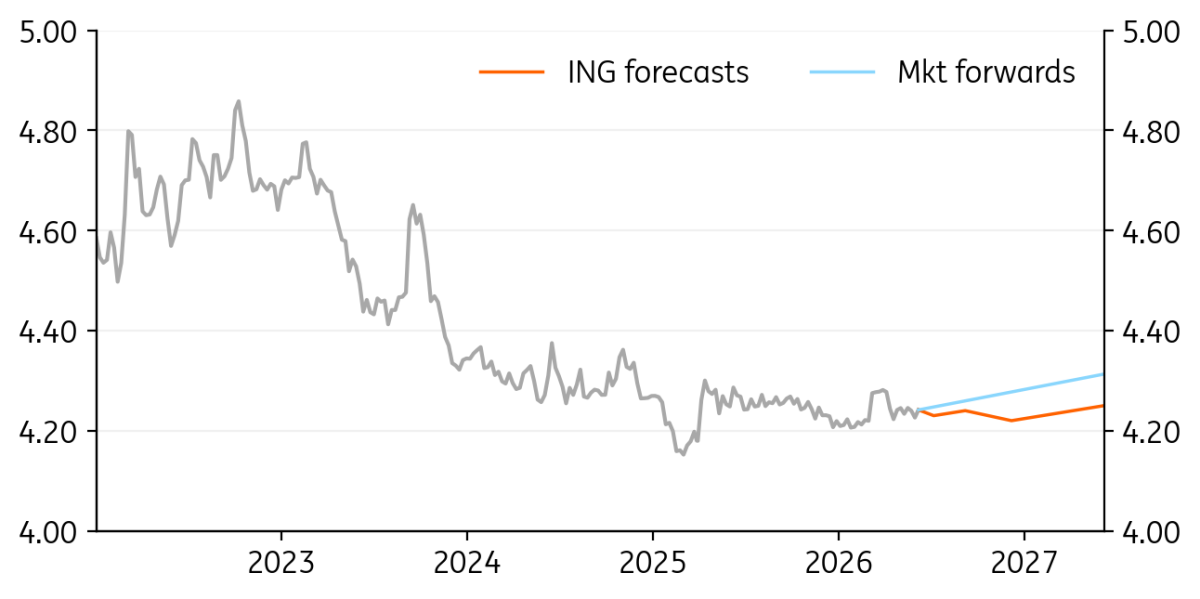

EUR/PLN: Zloty remains stable

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/PLN

4.25

|

Mildly Bearish | 4.23 | 4.24 | 4.22 | 4.25 |

- EUR/PLN maintains its narrow range (4.23 – 4.26) despite the turmoil in the Gulf, US dollar strength and a less hawkish approach by the central bank governor in June. The zloty remains relatively resilient to these factors.

- July was perceived as a live Monetary Policy Council meeting (due to the new projections), but recent dovish MPC comments and a low May CPI support our no-hike view for 2026, while markets still price 75bp in hikes. These expectations shield the zloty against risk-off waves.

- Our view on the zloty remains unchanged. We expect a limited rise in EUR/USD in the second half of 2026, sustainable GDP outperformance and expected inflows of EU funds to justify EUR/PLN hovering close to 4.24. Risks are still linked to geopolitical factors and a dovish MPC.

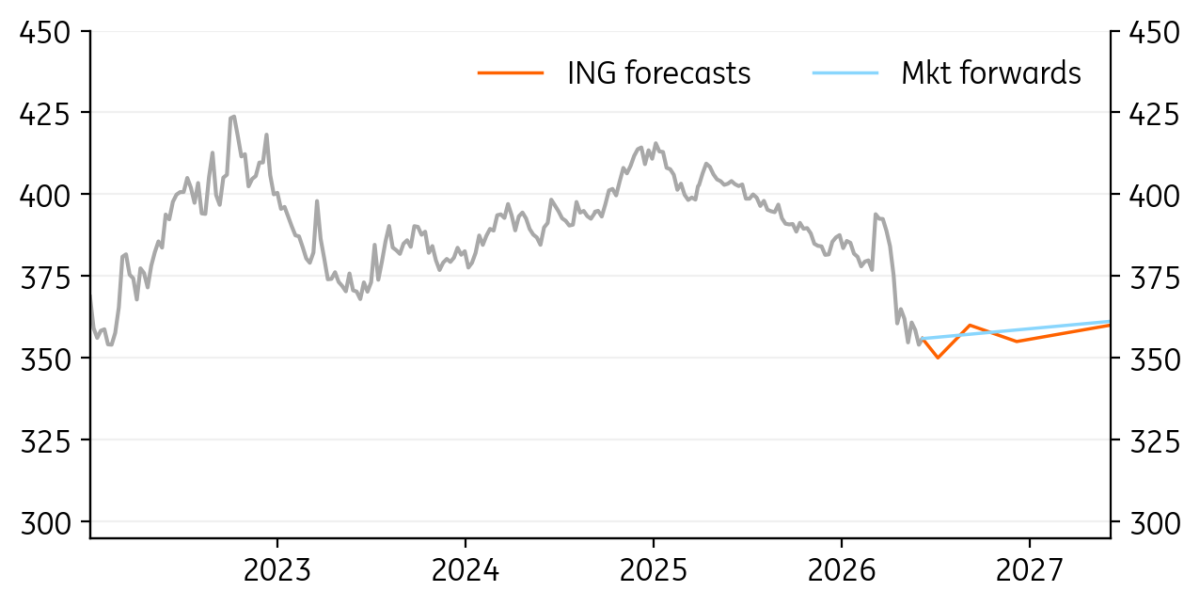

EUR/HUF: Positive factors to maintain the strength of the HUF

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/HUF

352.91

|

Mildly Bearish | 350.00 | 360.00 | 355.00 | 360.00 |

- We see the National Bank of Hungary cutting the base rate on 23 June. The extremely favourable May inflation print at 1.8% made us consider the possibility of a 50bp cut, though we still regard this as a remote option.

- With almost 100bp of easing priced in until end-2026, the easing cycle won’t derail the forint’s superstar status. Positive factors such as full access to EU funds, upgrades to ratings outlooks and a convergence programme should keep EUR/HUF at around 355 despite the lower interest rate premium.

- As policymakers prefer lower rates to a stronger forint, we see reactive policies sustaining a 350-360 range in the long term.

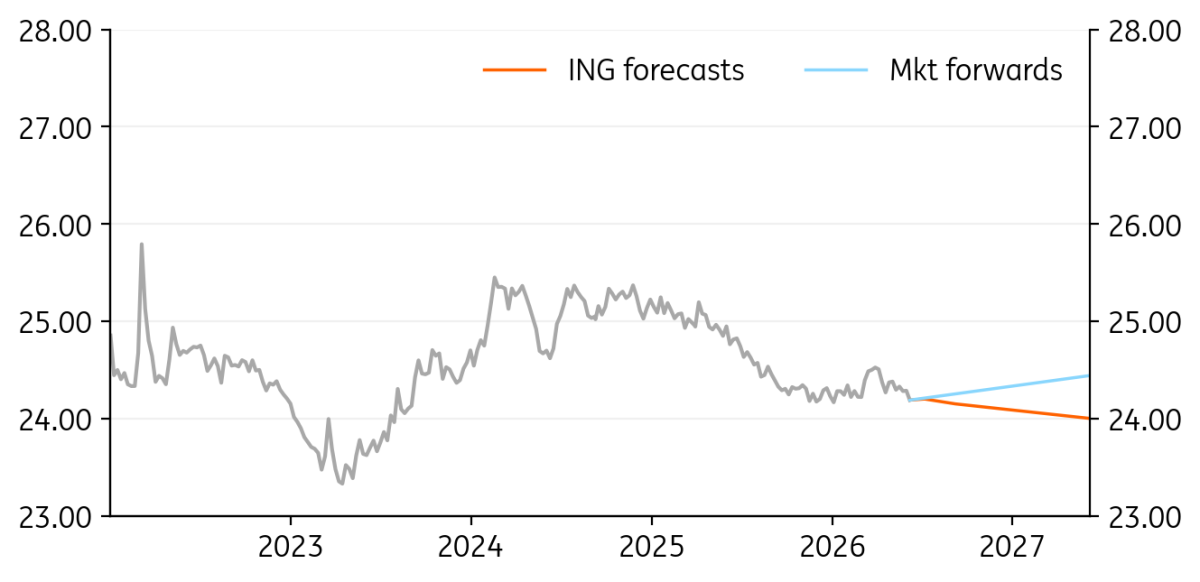

EUR/CZK: Czech rate hike on its way

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/CZK

24.18

|

Neutral | 24.20 | 24.15 | 24.10 | 24.00 |

- The Czech National Bank will likely proceed with one hike at its June meeting, which has been signalled by ample hawkish talk. However, we expect a split vote with a close call between a hike and flat base rate.

- In any case, the koruna will further be supported by the positive interest rate differential against the euro in both nominal and real terms. The recent ECB rate increase is not a substantial adjustment here.

- Should we see the impact of the Hormuz crisis on real growth in 2Q, the Czech and eurozone economies will both be affected. The economic support for the koruna should prevail and underscore its relative strength.

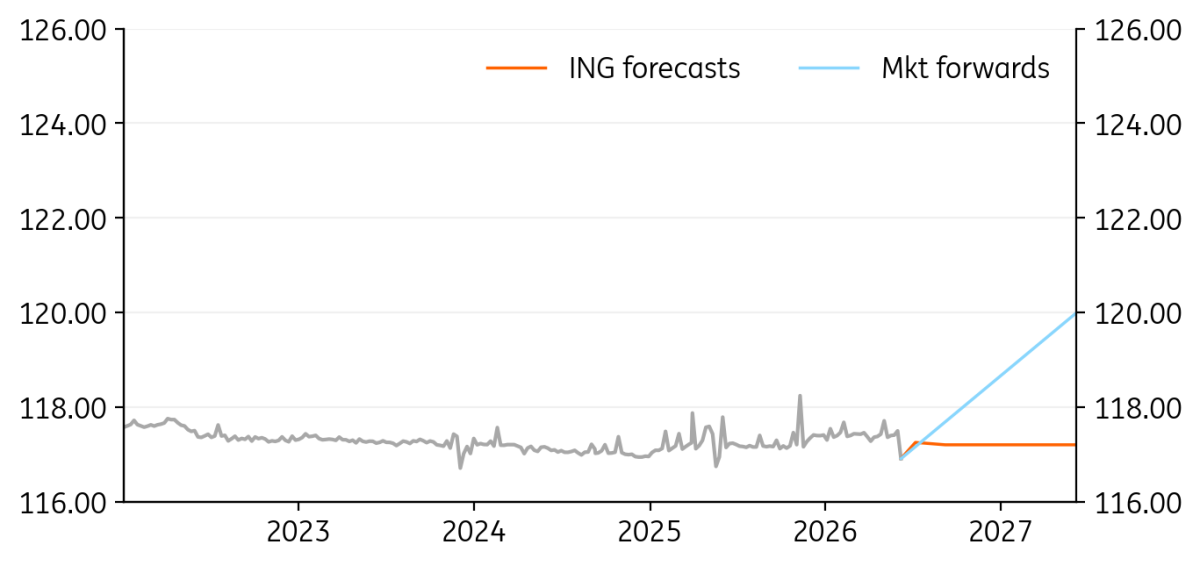

EUR/RSD: Investment trends keeping RSD supported

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RSD

117.36

|

Neutral | 117.25 | 117.20 | 117.20 | 117.20 |

- EUR/RSD has continued to trade mostly sideways, despite persistent political tensions. However, more positively, the shareholders’ agreement for the sale of the NIS refinery has concluded, after months of uncertainty. The pair sat mostly between the 117.30 – 117.50 range. Preparations and last-mile investments related to the EXPO 2027 event are also beginning to gather pace.

- As such, investments are still set to continue to fuel the tailwinds in activity ahead, while the country’s external position remains in check. The still-high, double-digit wage growth acted as a cushion through most of the recent uncertainties and has allowed demand to remain robust.

- At its June meeting, the National Bank of Serbia kept the key rate in place at 5.75% - highlighting the short-run inflationary pressures expected. We continue to believe that FX stability should remain a key focus ahead – in January-April, the Bank sold EUR 1205mn to keep the pair stable.

USD/UAH: Hryvnia at record low level

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/UAH

44.82

|

Mildly Bearish | 44.00 | 44.20 | 44.40 | 44.50 |

- As the US dollar strengthened on the back of solid data, USD/UAH rose towards 44.8, a record high level. The National Bank of Ukraine’s efforts to stabilise the hryvnia are insufficient to fully offset the global financial markets impact. Thus, the outlook for the hryvnia remains cloudy.

- May was another month in which international reserves of the NBU decreased (by 5.2% after 7.3% in April), mainly due to FX interventions and FX debt repayments. Nevertheless, the NBU see them as sufficient to maintain FX market stability.

- Still, the macroeconomic environment remains challenging due to the ongoing war. However, the latest business outlook survey shows further signs of an improvement with construction and industrial companies maintaining the most optimistic outlook.

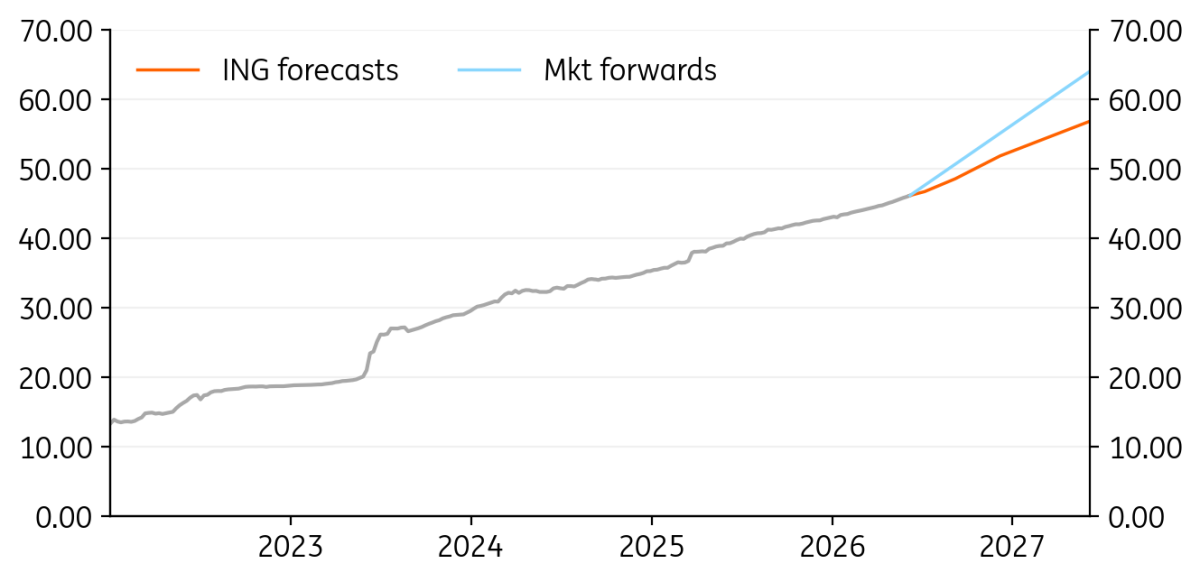

USD/KZT: Real rates remain high despite the surprise rate cut

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

489.43

|

Bearish | 480.00 | 480.00 | 490.00 | 500.00 |

- The tenge lost around 5% over the last month, following the correction in the oil prices. Meanwhile, the updated house view suggests upside.

- The National Bank of Kazakhstan made a surprise cut in the base rate by 100bp to 17.00%, without any commitment to further easing. With CPI of around 10% year-on-year, Kazakhstan’s real rates remain high.

- We expect the tenge to continue to benefit from portfolio capital inflows thanks to the future Euroclear connection, issuance plans, and hopes of an improved position in global bond indices. Meanwhile, the effect of higher oil prices should be muted by the accompanying dividend outflow.

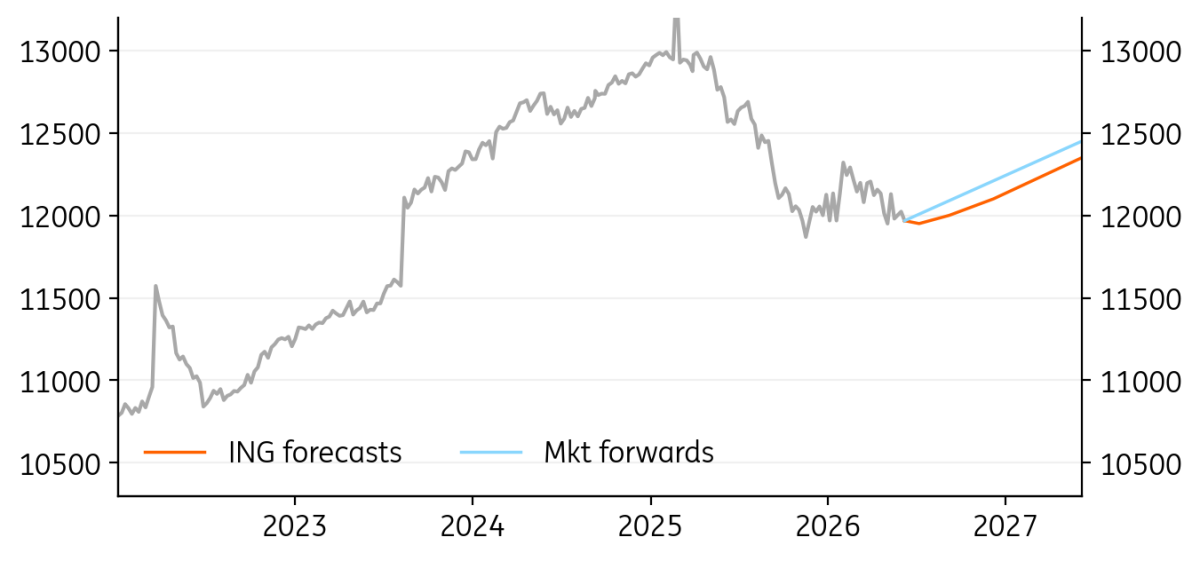

USD/UZS: Long-awaited restart of gold exports lifts UZS

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

11977.00

|

Neutral | 11950.00 | 12000.00 | 12100.00 | 12350.00 |

- The soum appreciated against the US dollar by around 1% over the last month, in line with our constructive view. The long-awaited restart of the gold exports was the main support factor.

- Portfolio inflows, likely supported by the privatisation pipeline and improved sovereign rating prospects should serve as additional reinforcement for the FX market

- A stronger soum combined with apparent ongoing fiscal consolidation have contributed to a material drop in CPI growth to 5.5% year-on-year as of May, creating room for a cut in the policy rate from the current high level of 14.00%.

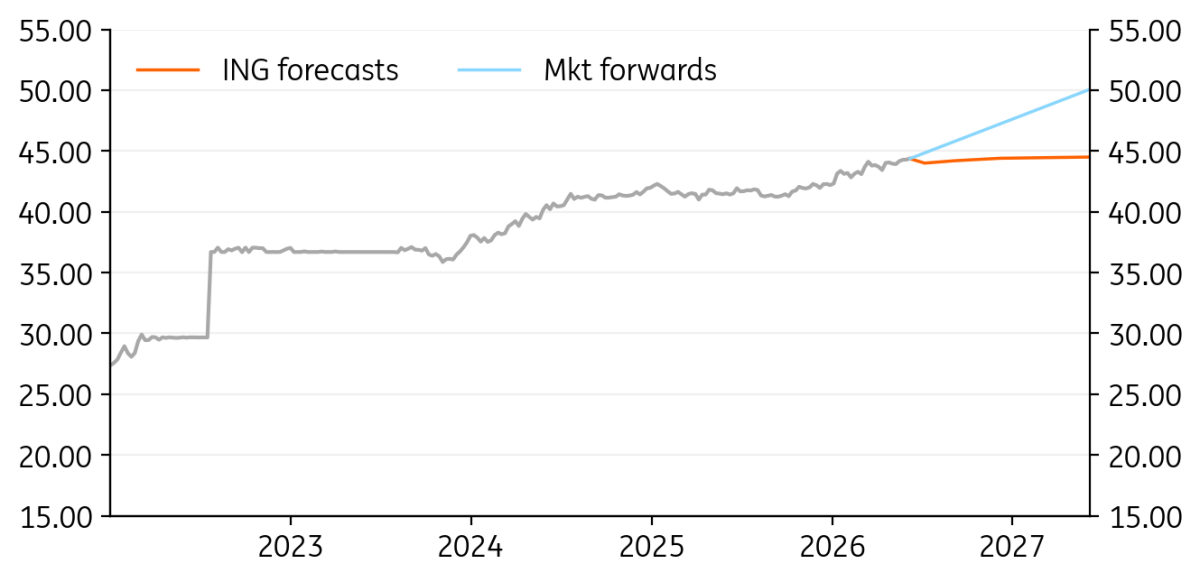

USD/TRY: A clear intention to preserve flexibility in policymaking

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/TRY

46.26

|

Mildly Bullish | 46.65 | 48.50 | 51.80 | 56.80 |

- May inflation has not yet shown a clear return to a disinflation trend, indicating a still challenging outlook. Uncertainty around oil prices, and the spillover into other commodities, continues to pose risks. Food inflation remains uncertain, shaped by agricultural supply expectations and potential fertiliser cost pressures. Annual inflation is expected slightly below 30%.

- The Middle East conflict has required a prolonged period of tight monetary policy, accompanied by stricter credit growth caps. These measures reflect a widening current account deficit and increased financial stability concerns after the court decision. Despite stable lending trends, the central bank has lowered TRY loan growth limits for the retail and corporate segments.

- Given this backdrop, all policy options continue to be available for the Central Bank of Turkey. This approach signals a clear intention to preserve flexibility in policymaking depending on changing geopolitical conditions. In the near term, we think the CBT will remain in a wait-and-see approach before deciding whether to reduce the effective cost of funding back toward the policy rate.

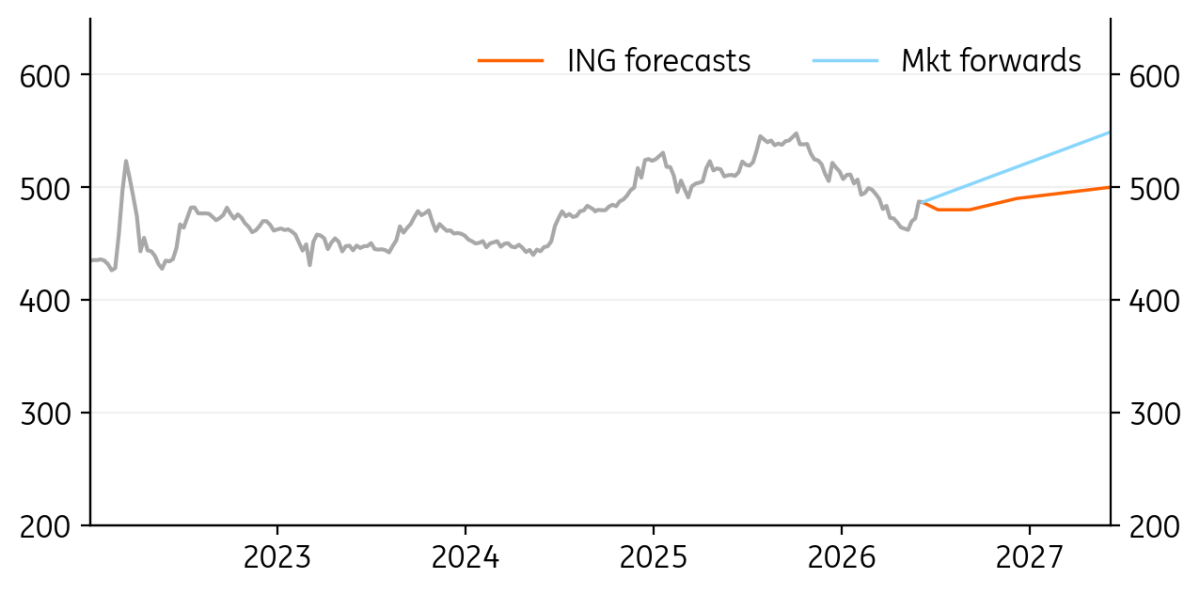

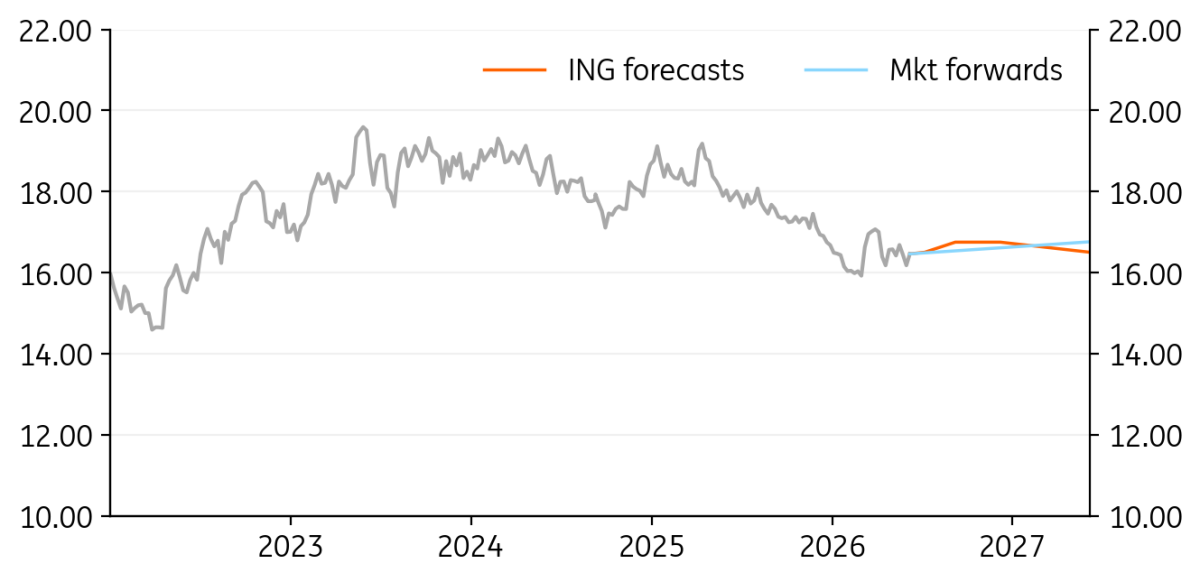

USD/ZAR: Headwinds growing, including El Nino

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ZAR

16.26

|

Mildly Bullish | 16.50 | 16.75 | 16.75 | 16.50 |

- Higher US rates and a tech-led sell-off in risk assets have started to weigh on the rand. But last month, the South African Reserve Bank pre-emptively hiked to 7%, leaving the rand with real rate protection of nearly 3%. The SARB has presented a worst-case scenario for rate hikes if the Strait of Hormuz remains closed for longer and El Nino hits hard. This could see SARB hike to 7.75%.

- We are raising our USD/ZAR profile because of the Fed story but still see it lower through 2027 on high yields, strong commodity prices and eventually lower rates in the US.

- But a heavy El Nino this November-February, causing drought in Asia and Africa, could be a major rand negative.

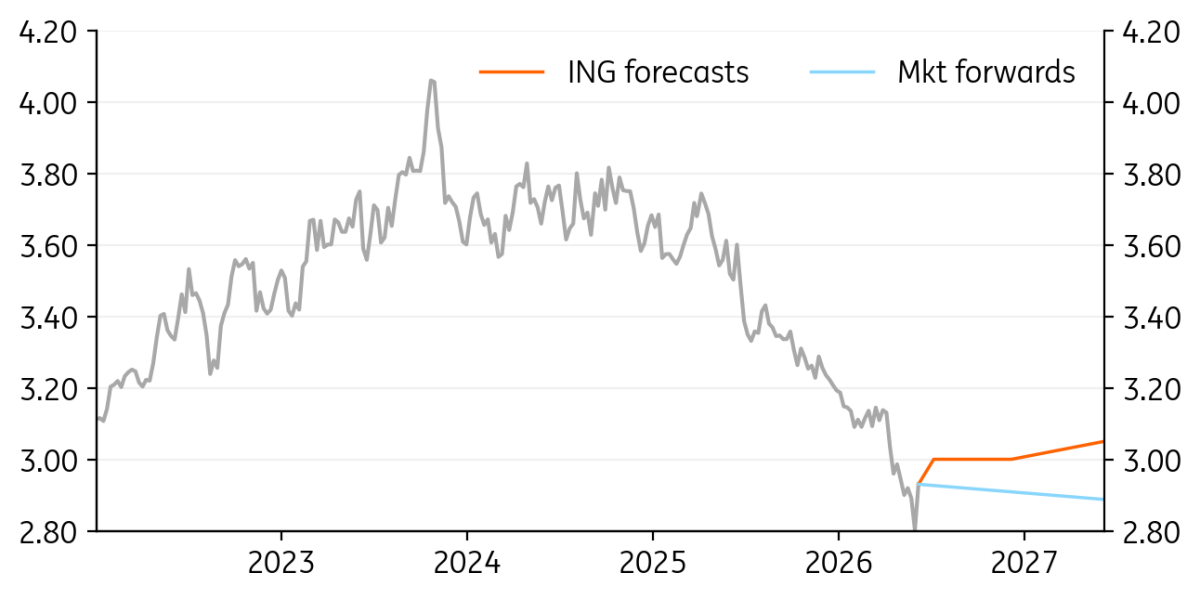

USD/ILS: Bank of Israel intervenes for first time since 2022

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ILS

2.92

|

Bullish | 3.00 | 3.00 | 3.00 | 3.05 |

- We had felt that the Bank of Israel did not want USD/ILS to be trading under 3.00. Over the last month it intervened to the tune of $800m and also cut rates by 25bp to 3.75%. Unlike elsewhere in the world, inflation is on target and the BoI is seen as having plenty of room to cut. The market has probably got ahead of itself, however, in pricing a further 150bp of easing.

- The FX intervention is the first since 2022 and quite a big deal. Previously it had been thought Washington had warned Israel away from intervention – that policy may have changed now.

- A stronger dollar and a tech world moving into frothy valuations leave the tech-sensitive shekel a little fragile this year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Bundle

15 June

FX Talking: Dollar downturn delayed

- This bundle contains 6 Articles