- Quick take

- 16 July

- United States

US retail sales point to a second-quarter consumer rebound

After a disappointing first quarter for consumer spending, retail sales data suggests we saw a rebound in the second quarter despite weak sentiment readings. Internet sales continue to outperform, with physical stores losing ever greater market share

Retail sales boosted by strong autos and internet sales

June US retail sales matched market expectations, rising 0.2% month-on-month at the headline level with the control group, which excludes volatile items (gasoline, food service, autos, building materials), and better tracks broader consumer spending trends, rising 0.5% MoM. Remember these are dollar value figures and lower gasoline prices meant gasoline station sales fell 5.3% MoM.

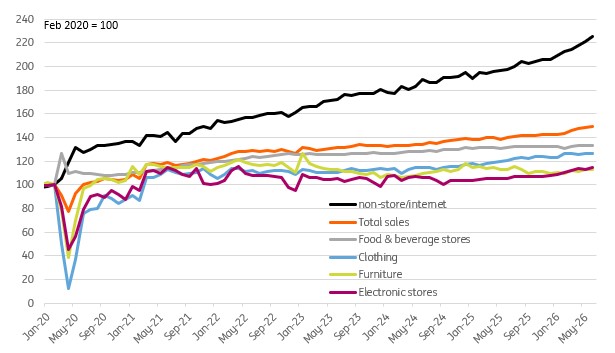

Non-store (internet) sales continue to be the main source of growth, rising 1.9% MoM, likely boosted by Amazon Prime Day. In year-on-year terms, sales are up 18% for this component versus 8.4% YoY for total sales. Sporting goods also saw robust gains in June, rising 1.3% MoM, but that component also saw quite significant inflation within the CPI report. Motor vehicle sales rose 1.9% and electronics rose 0.8%, but clothing (-0.3%), miscellaneous (-0.3%), grocery (-0.2%) and health/personal care (-0.8%) all saw weakness. The chart shows the relative performance of selected sectors since the pandemic and highlights how internet sales are so significantly outperforming physical stores in terms of sales values.

US retail sales levels

Retail sales set to continue underperforming broader spending trends

The chart above indicates a fairly mixed picture, but the overall retail sales number appears consistent with 2Q GDP real consumer spending growth of a touch above 2%, which is a marked improvement on the 0.5% annualised rate from 1Q.

Remember that we have experienced a 12-month period where real household disposable incomes have flat-lined – a highly unusual situation. This has most impacted medium- and lower-income households, with the combination of weak nominal income and employment growth plus elevated inflation prints constricting spending power and leading to a decline in the household savings ratio. Higher income households have been under less financial pressure and have been boosted by significant post-pandemic wealth gains – Federal Reserve data suggests that the top 20% of households by income hold 70% of the household wealth. These households tend to spend more of their income on services and experiences than middle- and lower-income households, who spend a greater proportion of their income on physical goods – as reflected within retail sales. The chart below shows that retail sales account for a declining trend overall of total consumer spending and suggests overall spending trends are likely to continue outperforming retail sales growth.

Retail sales as a proportion of total consumer spending

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more