US manufacturing and construction cool more than expected

The ISM manufacturing index posted a larger-than-expected contraction as orders dropped and production slowed. Construction also came in weaker than expected, which again indicates that monetary policy is restrictive and is acting as a brake on economic activity

| 48.7 |

ISM Manufacturing IndexFrom 49.2 in April |

| Worse than expected | |

ISM remains in contraction territory

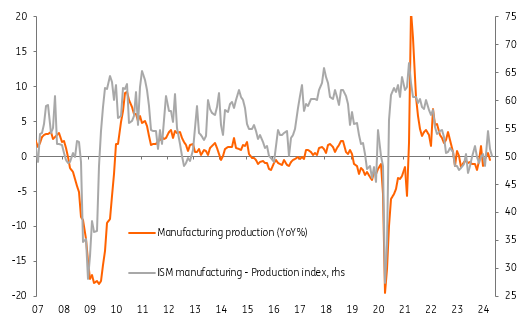

In Monday's US data flow we have a surprise drop in the May ISM manufacturing index to 48.7 from 49.2 (consensus 49.5) – remember that anything below 50 is a contraction. Regional surveys and the Chinese PMI, which we use as a guide for what may be happening on the West Coast in the absence of regional surveys for that part of the US, had suggested the prospect of a little changed outcome versus April. However, there was quite a sizeable drop in the new orders index (from 49.1 to 45.4) leaving it at its lowest level since May 2023. Production came in at 50.2 versus 51.3 in April (weakest since February) and the backlog of orders dropped to 42.4, the weakest level since November.

The prices paid component edged lower to 57.0 from 60.9 but remains above the 6M average of 54.1, so inflationary pressures linger on in the sector. The one bit of good news was the employment component, which moved above the beak-even 50 level to its highest level since March 2022, but with production slowing and orders looking weak, there are questions about how sustainable this will be. Instead, it may be that they are merely being able to fill a backlog of vacancies rather than actually increasing hiring plans.

Overall, the data is consistent with the view that the manufacturing sector is not going to add meaningfully to economic activity this year.

US ISM manufacturing and official output growth (YoY%)

Construction hurt by high borrowing costs and a lack of affordability

Separately, construction spending fell for a second month in a row and we expect to see an ongoing gradual moderation in the sector. High borrowing costs and tight lending conditions remain a constraint, and for residential in particular, where affordability is so stretched, this is prompting weakening housing starts and building permits, which should feed through into more softness in construction spending. Non-residential (outside of office construction) is also expected to slow, albeit from strong rates, as the initial surge of support from the Inflation Reduction and CHIPS Acts increasingly fades.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap