Turkey’s May inflation data brings no major surprises

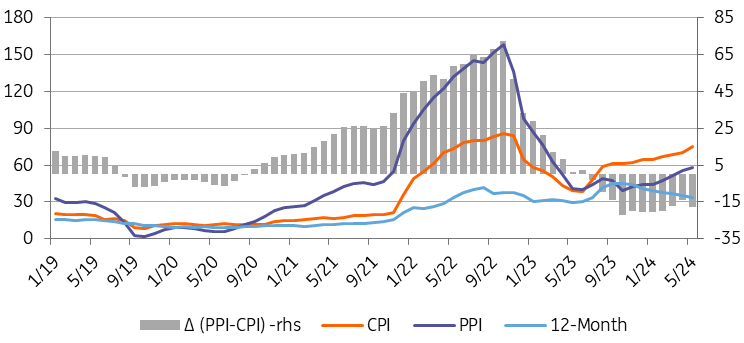

Turkey’s annual inflation reached its cyclical peak in May at 75.4% with price increases across the board in both food and non-food groups, in addition to one-off effects from the energy group

May CPI inflation turned out 3.37% month-on-month in Turkey, slightly higher than the consensus and our call. This pulled the annual figure to 75.4% year-on-year, in line with what the Central Bank of Turkey envisaged in its latest inflation report. While it was flat in May 2023 due to the one-year government subsidy for natural gas, the May average of the 2003-based index was 0.9%, indicating that the base effect was significantly unfavourable for this year. The turnout was the highest May reading in the current series. Accordingly, cumulative inflation in the first five months reached 22.7% vs the CBT's 38% forecast for this year.

PPI, on the other hand, stood at 1.96% MoM, showing an acceleration to 57.7% YoY, the highest since March 2023. The data implies building cost pressures due to food products, utilities and construction sector-related non-metallic mineral products in May. While exchange rate developments have been supportive lately, global commodity prices – which will likely remain the key determinant of the PPI trend ahead – have been on an increasing path since the beginning of this year.

Evolution of annual inflation (%)

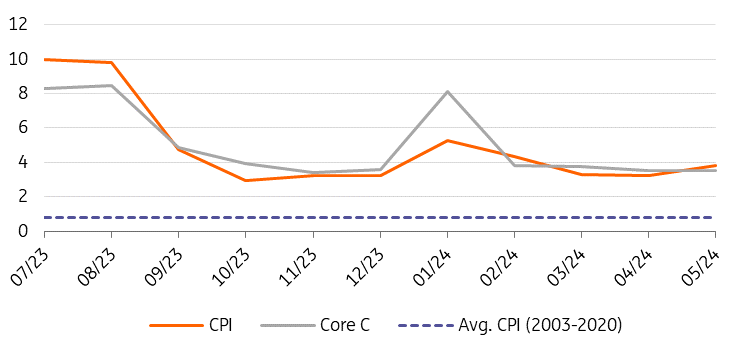

Core inflation (CPI-C) came in at 3.8% MoM, moving down to 75.0% on annual basis. This was supported by the relatively flat USD/TRY after the local elections, though pricing behaviour and inertia in services have been two factors keeping pressure on inflation. Accordingly, on a seasonally adjusted basis, it has remained elevated.

The seasonally adjusted headline figure, on the other hand, showed an increase in May thanks to the goods group – particularly energy. Meanwhile services, after their peak in January, are on a gradual improvement trend. But challenges remain in the disinflation process, with the underlying trend still significantly high. The CBT sees a decline in seasonally adjusted monthly inflation to around 2.5% on average in the third quarter, and slightly below 1.5% in the last quarter of the year. This implies that the drop in the underlying inflation should be more pronounced in the coming months.

Monthly trend CPI

Seasonally adjusted, month-on-month

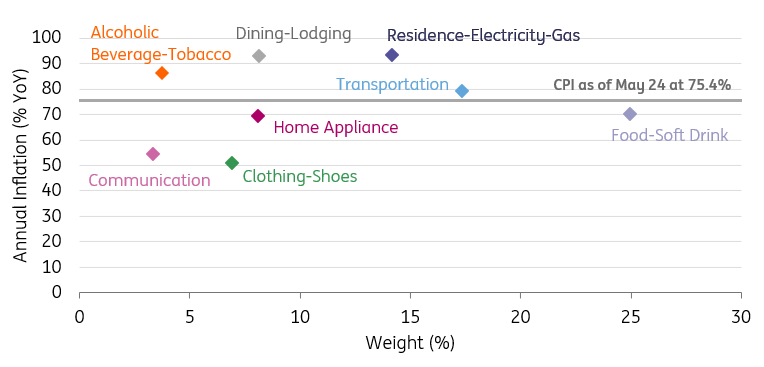

In the breakdown, all groups provided positive contributions. The subsidy that allowed consumers to use up to 25m3 of natural gas for free was removed in May. Accordingly, the housing group turned out to be the major contributor, with 0.99ppt. Clothing followed housing, with a 0.59ppt contribution due to seasonality. The closely linked catering services and food prices were the other major drivers, liftting the headline rate by 0.49ppt and 0.43ppt respectively.

As a result, goods inflation moved up to 67.6% YoY, while core goods inflation – a better indicator of the trend – inched down to 56.5% YoY. Services, which is an area less sensitive to currency movements but more impacted by domestic demand and minimum wage increases, recorded a slight decline to 95.9% YoY. This was mianly due to transportation services, while rent, the key component of this group, recorded another 5.5% MoM increase, exceeding 125% YoY.

Annual inflation in expenditure groups

Overall, annual inflation reached its cyclical peak in May with across-the-board price increases in both food and non-food groups, in addition to a one-off effect from the energy group. For the remainder of this year, annual inflation is expected to drop rapidly with the large base and is likely to be in the CBT’s forecast range (34-42%) at the end of 2024, but close to the upper band in our view.

Key determinants in the pace of disinflation will include: i) whether the stability in the exchange rate continues, and ii) whether or not the subsidies provided to consumers in electricity and natural gas prices remain in place and the government avoids inflationary tax adjustments. The deterioration in pricing behaviour and the rigidity in services inflation will remain as challenges in the period ahead, and the CBT will closely watch the inflation path and inflation expectations. The central bank will maintain its tight stance with the policy rate at 50%, while keeping the funding cost and ON repo rate high via liquidity policy, in our view.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap