- Quick take

- 1 November 2019

- United States

US: ISM indicates a manufacturing recession

The US manufacturing sector is in recession due to weak global growth, trade tensions and a strong dollar. There is little reason to expect an imminent turnaround with more support from the Federal Reserve likely needed

Manufacturing ISM disappoints again

The US ISM manufacturing index may have risen for the first time in March, but it remains in contraction territory at 48.3 (50 is the break-even level). Moreover, it was weaker than the 48.9 consensus estimate and it has only been weaker twice in the past ten years.

Adding to the sense of gloom for the sector, the report shows that this is the third sub-50 reading in a row with the production component dropping to its lowest level since April 2009. Orders and employment continue to contract with the one bright spot being a remarkable surge in export orders – tariff truce related? – to 50.4 from 41.0.

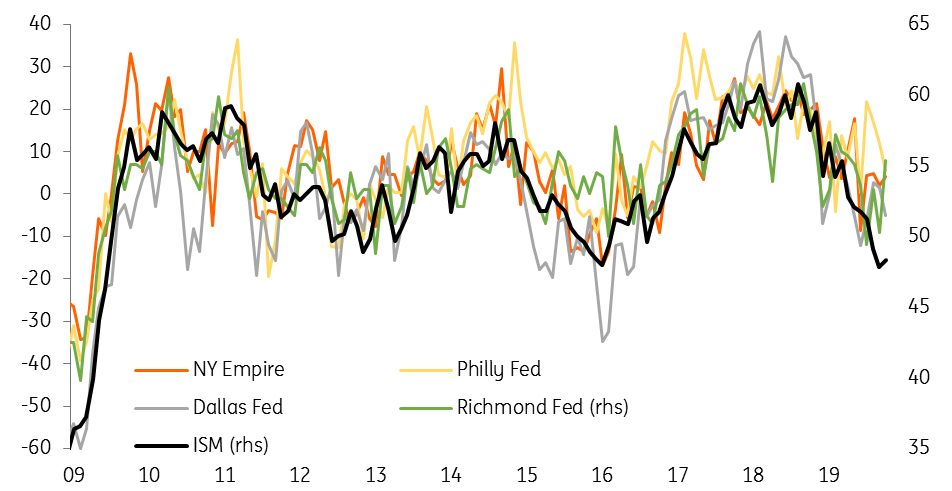

ISM weaker than the regional surveys

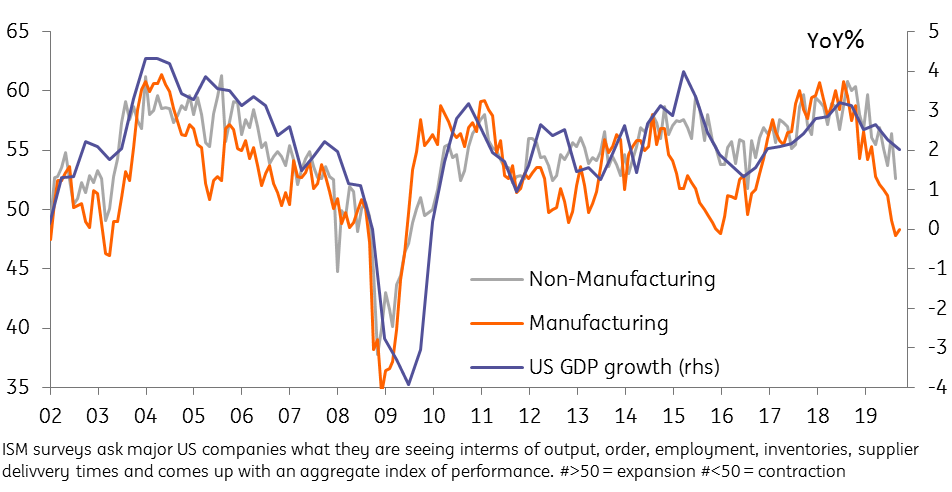

GDP growth set to slow further

Given the weakness in European and Asian indicators and the fact the dollar remains strong, it is difficult to see a sustainable improvement in export orders while there is broadening evidence that activity is decelerating domestically. There has been a truce called in the US-China trade tensions, but we see little scope for an imminent scaling back of the tariffs already enacted. As such this survey, together with the non-manufacturing ISM index which will be released next week (consensus looks for a small rise to 53.6 from 52.6), still suggests that GDP growth overall will trend lower. With inflation and inflation expectations remaining subdued, the Fed has scope to offer more support to the economy.

ISM business surveys signal weaker growth ahead

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more