- Quick take

- 4 November 2019

- Commodities daily

The Commodities Feed: Oil spec longs surge

Your daily roundup of commodity news and ING views

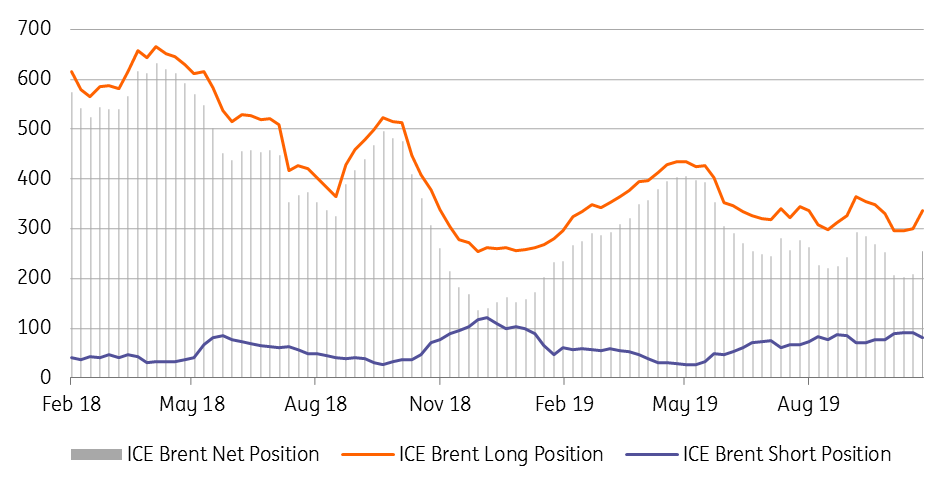

ICE Brent managed money position (000 lots)

Energy

Oil speculative positioning: Latest COT data shows that speculators increased their net long in ICE Brent by 45,648 lots over the last reporting week, leaving them with a net long of 253,999 lots as of last Tuesday. This is the largest weekly increase since early September, and also takes the net spec position back to levels seen in September. The increase was predominantly driven by fresh longs, rather than shorts coming in to cover. Looking at NYMEX WTI data, the increase in the speculative net long position was less impressive, rising by just 10,819 lots over the week, leaving speculators with net longs of 104,675 lots as of last Tuesday.

Canadian crude values: West Canada Select’s (WCS) differential to WTI widened further towards the end of last week, with WCS now trading at a discount of US$21.50/bbl to WTI. This compares to a discount of around US$16.75/bbl prior to news that the 590Mbbls/d Keystone pipeline would be shut due to a leak. On Friday, there were media reports that the pipeline could be shut for anywhere between 7-12 days in order to carry out repair work.

Metals

CFTC data: Latest data from the CFTC shows that money managers reduced their net short position in COMEX copper by 23,463 lots over the last week, with the total net short position falling to a six-month low of 20,365 lots as of 29 October. Speculators increased gross longs by 11,514 lots over the week, and covered 11,949 shorts, with sentiment slight more positive, as the US and China continue to work towards phase one of their trade deal. However, manufacturing data released more recently from both China and the US has been somewhat downbeat, and raises doubts for copper demand in 4Q19. Meanwhile, speculative net longs in gold increased by 7,171 lots over the week with speculators holding a net long of 233,101 lots as of 29 October.

Iron ore supplies: Vale announced on Friday that it will restart the 8mtpa Alegria iron ore mine in Brazil after the National Mining Agency in the country allowed the company to resume operations partially at the mine. While Vale has maintained its production and sales guidance for the current year, the restart of the Alegria mine supports the production outlook for 2020. From the more than 90mt pa of capacity suspended following the dam incident in January, only 42mt pa of capacity remains suspended as of now. Recovering iron ore supplies from Brazil, combined with healthy flows from Australia, have weighed on iron ore in China, with prices down around 30% from the peak in July.

Agriculture

Coffee prices: Arabica coffee prices have strengthened to a three-month high of US$1.04/lb as supplies from major exporting countries remained soft in October following a 3% drop in global coffee exports in September. Data released up until now shows that coffee shipments from Brazil dropped 4% year-on-year to 3.15m bags in October, while coffee exports from Honduras were down 12% YoY to 88.7k bags for the month. There are concerns over dryness in some parts of Brazil, whilst producers have reportedly been holding onto inventories in the low price environment.

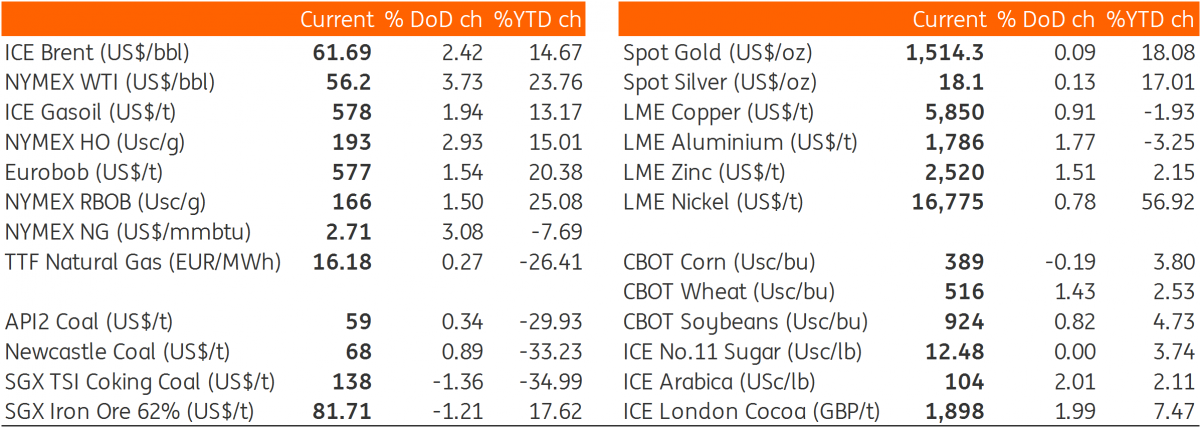

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more