- Quick take

- 1 May 2019

- Commodities daily

The Commodities Feed: US oil imports plummet

Your daily roundup of commodity news and ING views

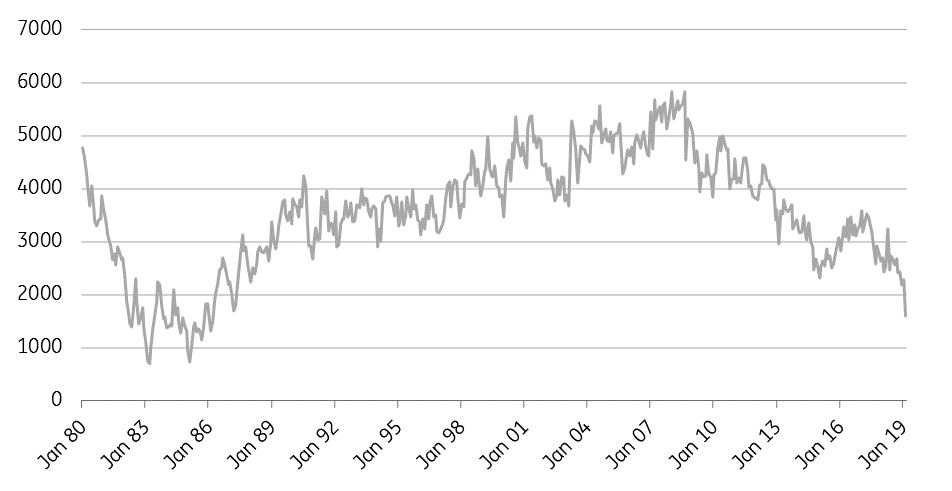

US oil imports from OPEC nations fall to more than a 30 year low (Mbbls/d)

Energy

US oil inventories: The API yesterday reported that the US crude oil inventories increased by 6.81MMbbls over the last week, significantly higher than the 1.75MMbbls that the market was expecting. The API reported drawdowns of 1.06MMbbls and 2.06MMbbls in gasoline and distillate fuel oil, respectively. The more widely followed EIA report will be released later today.

The bigger-than-expected stock build has weighed on the market, which saw a reversal of much of yesterday’s gains following comments from the Saudi oil minister that OPEC+ could continue with their deal through until the end of this year, whilst the market also largely ignored the growing unrest in Venezuela. While a change in regime could mean increased oil output in the longer term, it could also mean short- to medium-term disruptions, while we believe it will not be a quick fix to turn the state of the domestic oil industry around even with a new regime.

EIA monthly oil numbers: Latest monthly data from the EIA shows that US oil production in February averaged 11.68MMbbls/d over the month, a fall of 187Mbbls/d MoM, and the second consecutive decline in monthly production. We will likely have to see some production estimate revisions coming from the EIA, with output over February 71Mbbls/d lower than the EIA’s estimate in its Short Term Energy Outlook.

Interestingly, the monthly data also showed that US crude oil imports from OPEC nations averaged just 1.6MMbbls/d over February, down from 2.27MMbbls/d in January, and the lowest monthly import volume from OPEC nations seen since February 1986. This decline in imports flows reflects the impact of US sanctions on Venezuela oil imports, along with OPEC production cuts, and in particular, the Saudis reducing export volumes to the US.

Metals

Aluminium under pressure: LME aluminium remains under pressure, with prices briefly breaking below US$1,800/t at one stage yesterday. Weaker than expected Chinese manufacturing PMI numbers wouldn’t have helped, while a number of producers also revised lower their demand growth estimates for this year, which certainly did not help sentiment. Meanwhile, the persistent contango in the cash/3month spread, along with LME inventories edging higher suggests that there is no significant tightness in the spot aluminium market.

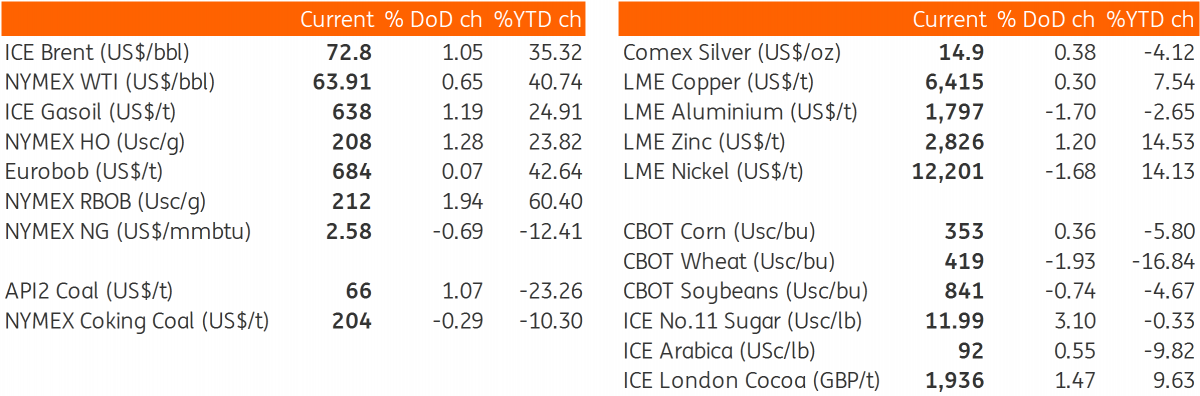

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more