- Quick take

- 28 August 2020

- Commodities daily

The Commodities feed: US Gulf refiners come out largely unscathed

Your daily roundup of commodity news and ING views

Energy

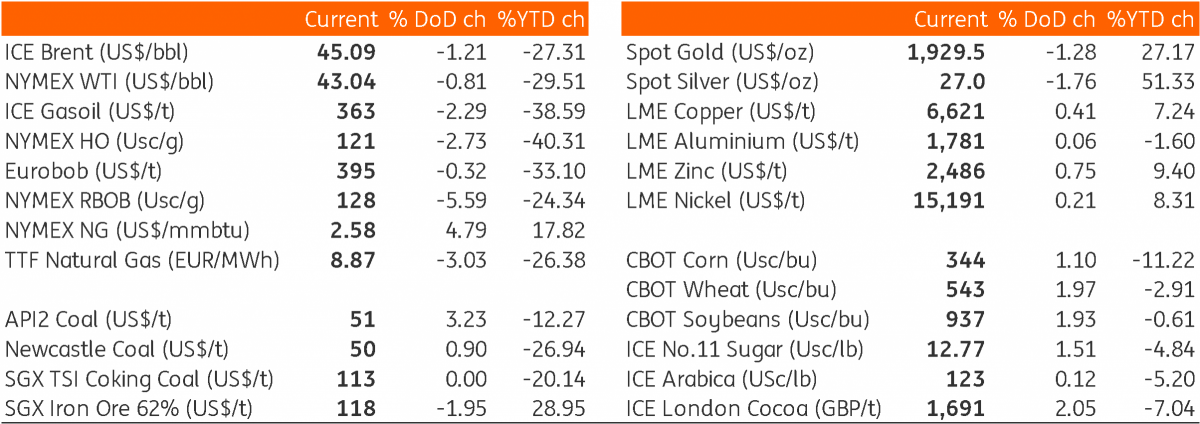

Hurricane Laura made landfall yesterday, and in doing so lost power which saw it downgraded to a tropical storm. Offshore oil and gas production in the US Gulf of Mexico remains largely shut, with oil shuts-ins as of yesterday still standing at 1.56MMbbls/d according to the Bureau of Safety and Environmental Enforcement (BSEE). With the storm now passed, this production should start coming back online. Refineries along the US Gulf Coast seem to have suffered minimal damage due to the storm, with most of those who shut expected to come back online over the course of the next week. Refineries in Lake Charles seem to have been the worst hit, with reports that Citgo’s 418Mbbls/d Lake Charles refinery could be shut for 4-6 weeks in order to repair the damage. There is little detail on when Phillips 66’s refinery in Lake Charles will restart. Limited refinery damage and the quick resumption of capacity is good news for crude oil demand, although for now that is not reflected in the market, with crude trading marginally lower in Asia this morning.

Metals

Precious metals fell while base metals recovered slightly soon after the Federal Reserve said that it would come up with an aggressive new strategy that aims to boost employment and allow inflation to run faster than in the past. LME copper prices traded marginally higher, whilst spot gold prices closed almost 1.3% lower on the day. Meanwhile, Indonesia’s Grasberg gold and copper mine said yesterday that it would ease the lockdown at its mine, in an effort to end ongoing labour protests at the site. The company confirmed that it has reached an agreement with the local government to ease Covid-19 restrictions and allow workers to travel to a nearby town.

In Aluminium, at least three Japanese aluminium buyers were offered a premium of US$95/t for 4Q20 shipments yesterday, up 20% from the previous quarter. The recovering premium indicates an improvement in demand, following Covid-19 related lockdowns. For copper, Chinese Yangshan copper premiums further declined to US$68.5/t (the lowest level since April) yesterday, compared to US$83.5/t at the start of the month. Falling premiums could be due to sluggish activity in the spot market in China and the rising backwardation in the LME cash/3m spread.

Agriculture

The International Grains Council (IGC) released its latest monthly update yesterday, with the biggest revisions seen in the soybean market. The IGC revised higher its global soybean production estimate for the 2020/21 season to a record 373mt (+34mt YoY), which is up from the previous estimate of 365mt. The increase is largely on the back of expectations for a larger crop from the US. Despite larger global production, carryover stocks will only increase marginally, due to expectations of stronger demand. For wheat and corn, there were few changes to the global balance for 2020/21.

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more