- Quick take

- 11 October 2019

- Commodities daily

The Commodities Feed: OPEC+ hints deeper cuts

Your daily roundup of commodity news and ING views

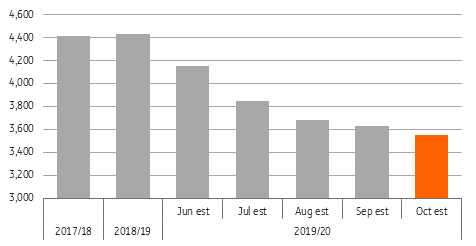

US soybean production estimates (m bushels)

Energy

OPEC+ hints deeper cuts: ICE Brent moved higher on Thursday after OPEC’s general secretary Mohammad Barkindo said that the OPEC+ group will do ‘whatever it takes’ to support oil prices amid the ongoing economic turbulence. The reassurance by OPEC raised hopes of the current output cuts being extended into 2020 or even deepened, if required, to balance the market. Optimism for a partial trade agreement among China and the US and ongoing geopolitical tensions, including a reported attack on an Iranian oil tanker in the Red Sea today, continue to support crude oil prices.

In the meantime, the OPEC has released its monthly oil market report and estimated that the world oil market witnessed a large deficit of around 1.5MMbbls/d in 3Q19, the largest supply shortfall for a quarter since 2007, mainly due to supply outages in Saudi Arabia. Moving forward, OPEC has lowered its supply growth estimates for 2019 and 2020 from 1.99MMbbls/d to 1.82MMbbls/d and from 2.25MMbbls/d to 2.2MMbbls/d, respectively. On the other hand, demand growth estimates are largely left unchanged at 0.98MMbbls/d for 2019 (marginally down from 1.02MMbbls/d) and 1.08MMbbls/d for 2020 (same as previous estimates). IEA’s monthly oil market will be released later today and will be watched closely for any revision in demand growth expectations.

Metals

Zinc outperform: The LME metals index gained around 1.5% on Thursday and has been trading positively in the morning session on optimism over the trade talks between China and the US. LME zinc has outperformed the metals complex and was up 4.2% yesterday on better demand prospects if a deal is agreed as well as output disruptions. News reports about the temporary closure of Vedanta’s Skorpion zinc refinery in Namibia for four months from November (Reuters news) due to the ore shortages have helped zinc to push higher. The zinc market could see around 25kt of output losses, an estimate based on previous production, adding to the existing deficit in this year’s global market balance.

Copper mining protests: MMG reported that its Las Bambas copper mine in Peru is witnessing fresh local protests around the mine site and some operations are closed due to roadblocks. The mine’s access to ports for copper concentrate shipment is severely affected due to the current protests and the company may have to declare force majeure on supplies if the issue is not resolved soon. The mine produced around 186kt of copper in 1H19 and output disruptions at the mine could create short-term supply issues for the global market.

Agriculture

USDA WASDE report: The monthly WASDE report from USDA has been fairly constructive for soybean prices with CBOT soybean trading at a one-year high of US$9.3/lb as of this writing. The USDA lowered the estimates for soybean acreage from 75.9m acres to 75.6m acres while soybean yield was also revised down from 47.9bu/acre to 46.9bu/acre. As a result, soybean production estimates are revised down from 3,633m bushels to 3,550m bushels, which will push down the soybean ending stocks to 460m bushels compared to its earlier estimates of 640m bushels. The USDA has kept corn supply-demand estimates largely unchanged for the US market; however, ending stocks are revised down from 2,190m bushels to 1,929m bushels mainly due to the downside revision in the beginning stocks.

Globally, ending stocks of soybean and corn were revised down from 99.2mt to 95.2mt and 306.3m to 302.6mt, respectively, mainly due to a downside revision in beginning stocks and lower production estimates from the US. Global demand for soybean was revised down by 1mt to total 352.3mt mainly on lower crushing demand in Argentina. Global demand for corn was lowered by around 2.7mt to total 1,125mt.

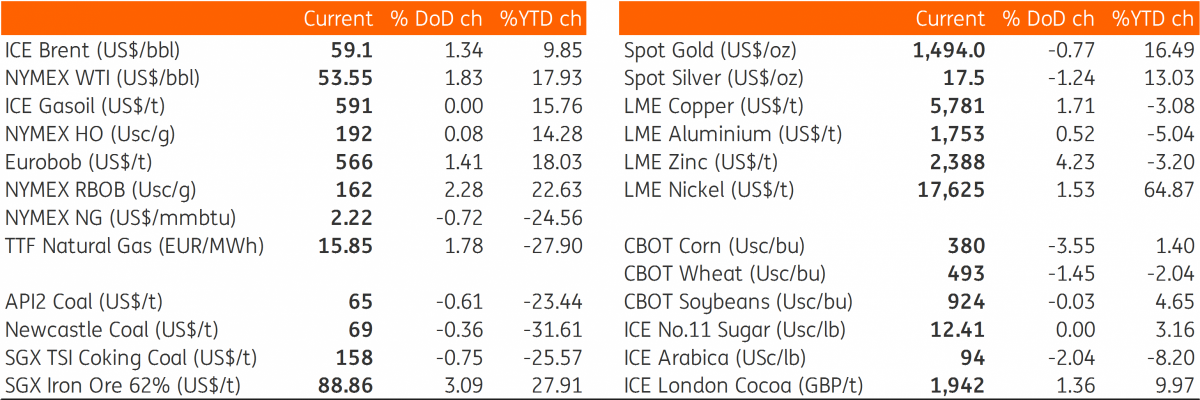

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more