- Quick take

- 16 March 2020

- Commodities daily

The Commodities Feed: Fed easing offers little support

Your daily roundup of commodity news and ING views

Energy

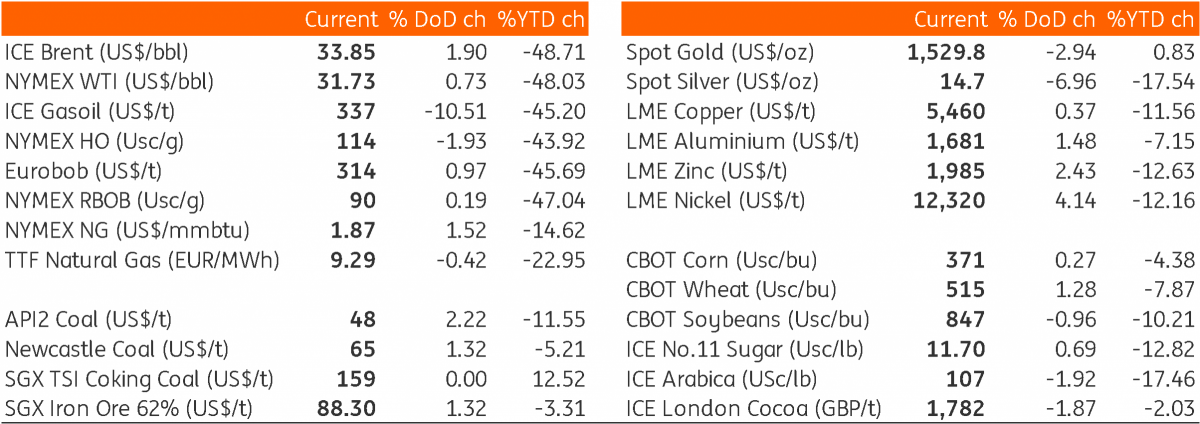

The outlook for markets continues to look increasingly gloomy, with more countries going into lockdown over the weekend and further travel restrictions. ICE Brent is down by around 3% at time of writing, moving ever closer towards the US$30/bbl level. Clearly the oil market has ignored the emergency rate cut from the US Fed over the weekend. The breakdown in the OPEC+ deal could not have come at a worse time, with the market already having to deal with a demand shock. The surge in supply expected from April, along with the demand hit, does mean that the global oil market is set to see a significant surplus over 2Q20, suggesting that this current weakness is likely to persist through 2Q20. Time spreads also reflect the surplus environment, moving deeper into contango, with the ICE Brent May/Jun spread trading to more than a US$2/bbl discount late last week.

Another spread where we have seen a big move is WTI/Brent, trading at around a US$1.30/bbl discount at the moment, compared to a more than US$5/bbl discount at the start of March. The relative weakness in Brent shouldn’t come as too much of a surprise, given the severity of the breakout across Europe, along with the action taken by governments in order to try contain the virus. Another factor offering relatively more support to WTI is news that President Trump has ordered Strategic Petroleum Reserves to be filled up at these lower price levels. This theoretically means that around 92MMbbls could be bought up but logistical constraints would mean that this number is likely to be lower.

Finally, latest Commitment of Traders data shows significant liquidation in ICE Brent from speculators, with them reducing their net long by 74,430 lots over the last reporting week. This leaves them with a net long of just 153,355 lots as of last Tuesday - approaching levels last seen in late 2018.

Metals

Metal markets have largely ignored the emergency action taken by the US Fed over the weekend, with it cutting its benchmark rate by a full percentage point, and the restart of quantitative easing. All but one of the LME metals are trading in the red this morning. Meanwhile poor industrial production numbers out of China over the first two months of the year has certainly not helped.

Meanwhile, latest data from the Shanghai Futures Exchange (SHFE) showed that copper stocks rose for a fifth consecutive week, with inventories climbing by 35kt last week to take total inventories to 380kt – the highest level since March 2016. Copper inflows so far over March stand at 69kt, more than half the total inflows of 105kt seen in February. YTD inflows for copper now stand at 239kt versus 156kt over the same period last year. Looking at other metals, SHFE aluminum stocks saw an increase of 40kt over the week to total 520kt, whilst SHFE zinc stocks grew marginally by 8kt to 170kt. YTD inflows for aluminium total 332kt, compared to inflows of 67kt over the same period last year. The constant rise in inventories appears to be directly attached to to China’s continued struggle with overall sluggish demand.

In ferrous metals, latest Steelhome data shows that Chinese iron ore port inventories remained flat, with total socks standing at 126mt as of 13 March, compared to a marginal outflow of 70kt a week earlier. The slowing outflows of raw materials highlight the constant pressure in the downstream industry.

Daily price update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more