- Quick take

- 16 March 2020

- Romania

Romania: Pandemic hits growth at the worst time

Romania's economy needs growth more than ever. Instead, it will take a serious hit, and every sector will suffer to some degree from the fallout of the coronavirus. The mix of lower growth and increased fiscal spending could easily send the budget deficit way above 5.0% of GDP

Things are moving fast and have taken an unexpected turn due to the Covid-19 pandemic. Under the important assumption that the disruption will start to dissipate by the end of the second quarter, we have downgraded our GDP growth forecast from 3.6% to 2.1%, with risks noticeably skewed to the downside.

The background

In recent years, Romania has been rapidly burning through its fiscal buffers but managed to overcome its fiscal problems by posting impressive growth rates each year. It was growth that kept most debt metrics within acceptable limits, despite the ballooning wage envelope, social assistance spending, current account deficit and nominal debt.

In 2019, one of these metrics cracked big time: the budget deficit reached -4.64% of GDP, revealing a fiscal position on the skids. Hence for 2020, nominal growth is needed more than ever in order to accommodate the gradual fiscal consolidation that the government is targeting.

A sector review

The disruption caused by the Covid-19 pandemic in the Romanian economy will most likely be visible starting with macro data for March. In general, there is a one-to-two month delay between the availability of the data and the month the data refers to. Hence, at this moment we don’t have any macro/sector data to reflect the developments that took place in the past few days. Until we have the first hard numbers, we will have to rely on surveys for another month or so. The best we’ll have is probably the Economic Sentiment Index (ESI), due 30 March.

2019 GDP structure

1.1. Services

Unarguably, the current “social distancing” recommended by authorities is going to have a dramatic impact on most categories of services. Tourism will be severely affected as most people have either cancelled or not booked a trip for the next few months. Local media reports that, as of 14 March, bookings for the traditional Easter holiday are down almost 80% versus 2019. Restaurants and hotels are reporting 80-90% lower sales, the aviation industry is hugging the ground as we speak, and the list goes on to real estate, transportation and financial services. Except for a temporary boost in retail sales activity due to the fear factor (even here it will be interesting to see how much booming food sales make up for the falling non-food sales), there is just nothing good that we can expect from the private service sector. And with a share of c.45% of GDP, private services are certain to be a serious drag on both second and third quarter GDP.

Public services, on the other hand, will most likely increase their contribution, but due to their lower share (c.14% of GDP) and lower multiplier effect, we don’t expect them to come even close to offsetting the impact from the private sector.

1.2. Industry

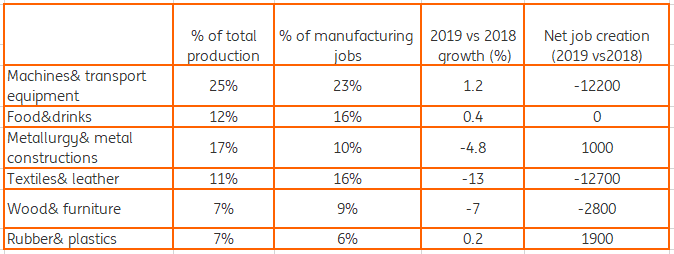

The industrial sector has already been in contraction mode and a drag on growth since last year, when it subtracted 0.3 percentage points from GDP. When we say industry, we really mean manufacturing, as this forms about 80% of industrial production. And the trend here was already quite worrying, with the manufacturing sector losing about 25,000 jobs last year, mainly textile and automotive related.

Top manufacturing sectors

What’s even more disquieting, in our view, is that manufacturing production relies mostly on external demand. Hence, whatever the already-announced stimulus package accomplishes, it is unlikely to have a significant impact on the industrial production side. Given the falling demand, and the natural inertia of this sector, we expect that the contraction could reach double digits this year and subtract more than 1ppt from 2020 GDP.

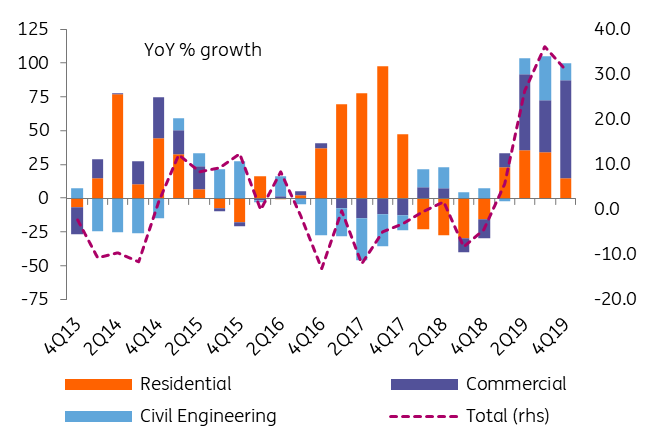

1.3. Construction

The construction sector boomed in 2019, expanding by almost 25%, helped by fiscal measures enacted on 1 January 2019. The trend in the last few quarters was pointing towards a mild moderation, as residential construction slowed down, leaving commercial construction to keep the bar high.

Commercial construction leading the way

In 2019, construction added 0.9ppt to GDP, the highest contribution since 2008. We acknowledge that the sector has a specific inertia to it and that the huge fiscal spending from the end of 2019 will be visible in 1Q20 data, hence we are not yet calling for an outright contraction of construction activity. That’s not to say that we don’t expect bad news, but it’s unlikely to be the hardest hit sector.

1.4. Others

For the purpose of our forecast, we have considered as constant the contribution of agriculture to 2020 GDP and halved the net taxes item. This means a neutral impact from agriculture and a 0.4ppt positive impact from net taxes.

Fiscal impact

As already mentioned, the current epidemic will damage growth just when it was needed the most. The -3.6% of GDP budget deficit for this year was already an overly ambitious target, even with the official GDP growth forecast of 4.1%. The combination of lower growth and higher spending will – in our view – push the budget deficit above 5.0% of GDP, even in a scenario where the 40% pension hike is postponed. At this level, financing the deficit will probably require a degree of cooperation between institutions, similar to what we saw in December 2019. Fortunately, the first two months of 2020 have been extremely successful for the Ministry of Finance in terms of issuance, and we don’t believe there are immediate funding pressures.

On the other hand, the European Commission has given clear signs that it will take a flexible approach to spending generated by measures to contain the coronavirus outbreak and its socio-economic effects. Although one can be reasonably certain that fiscal deficits going from say -1% to -2% or even -3% of GDP will fall within the definition of “full flexibility”, we are not so confident about deficits going from -4.6% to -5.0% or more.

Markets and the monetary policy

We believe that the National Bank of Romania's monetary policy will remain FX-focused. To the extent the NBR is comfortable with the fiscal backdrop, we envisage the central bank doing a little bit of everything: leaving the EUR/RON to shift higher earlier in the year rather than later (we maintain our 4.85 year-end forecast), leaving some carefully monitored surplus liquidity in the market, further cuts in minimum reserve requirements and even one or two 25bp key rate cut(s) if the economic downturn deepens and/or other Central and Eastern European central banks start to cut. Above all however, we believe that the NBR will work with the banks and the MinFin to support lending schemes for the businesses most severely impacted. A RON10bn state guaranteed interest-free lending package for SMEs has already been announced by the Ministry of Finance and we think there is more of the same to come.

We maintain our 4.85 forecast for the year-end EUR/RON. On the money market, we expect choppier liquidity conditions and volatility in FX swap implied yields, but not necessarily in Robor rates. The fixed income market might be the one most severely hit as offloading (or even onloading) positions in this market context could generate extreme volatility.

Whatever policy mix is put on the table, we believe that fundamentally it will be the consumer behaviour that will steer things one way or another. The situation has – in our view already passed beyond the level of supply-chain disruption and production bottlenecks. It has spread to the consumer sector and it was mainly the consumers who kept the growth momentum high when industry was contracting last year. Hence, once the quarantine ends and the virus spread is under control, boosting consumer confidence will be of utmost importance in order to restart growth.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more