- Quick take

- 16 January 2019

- Turkey

Turkey: The CBT keeps rates on hold again

At the January MPC the CBT kept the policy rate flat at 24%, while highlighting the prevailing risks on price stability.

| 24% |

1-week repo rate(Unchanged) |

| As expected | |

At the January rate-setting meeting, the CBT kept the policy rate (1-week repo rate) unchanged at 24%, in line with the Bloomberg median consensus and our call, and despite recent TRY stabilization and current disinflation dynamics. In an initial reaction USD/TRY dropped below 5.40, though it recovered partially later.

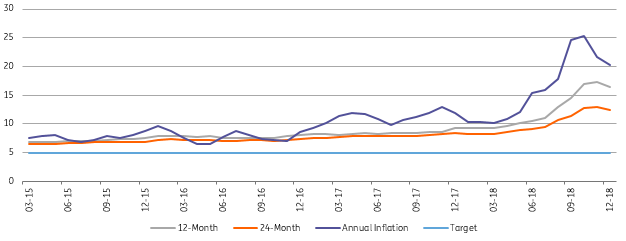

After its sharp uptrend until October inflation turned out to be 20.3% at end-2018, lower than previously envisaged. This was thanks to TRY strength, lower energy prices, weaker domestic demand and the government's tax cuts. However, despite market pricing showing a significant downward adjustment over the current effective funding rate, the CBT remained on hold again in January. The challenging inflation outlook is likely to be creating concerns for the bank. In other words, despite the current weakening in business activity leading to reduced pressure to keep rates elevated, unsupportive base effects and significant adjustments in minimum wage are unlikely to help the disinflationary trend in the near term. Risks for inflation remain tilted to the upside - with the marked deterioration in pricing behaviour, vulnerability to shifts in global risk appetite and the upcoming elections creating concerns for fiscal policy all keeping the CBT cautious in the near term.

Inflation Expectations (%)

The accompanying statement includes some minor changes from the previous month’s note. The CBT maintained the main policy guidance that highlights its determination to tighten further, if needed. One addition to the statement is related to the external outlook as the bank expects the current account balance “to maintain its improving trend”. This is hardly surprising, given weakening domestic demand and deleveraging in the banking sector.

The CBT remained on hold this month and maintained its tightening bias, with a promise to deliver further monetary tightening if needed. This was on the back of (1) a still fragile currency - evidenced by recent rapid moves with some recovery in oil, negative news flows regarding US relations and concerns about an early easing, and (2) continued dependence on external financing - showing signals of improvement in the latest capital account data, though remaining frail.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more