- Quick take

- 3 February 2023

- Turkey

Turkey: Second-highest January reading in current inflation series

While January inflation in Turkey significantly surprised on the upside, it is on a downward trend with large base effects that will likely contribute to further decline in the near term

January's inflation reading of 6.65% turned out to be the second-highest January reading in the current inflation series, which started in 2003, and was significantly higher than the market consensus of 3.8%. However, the annual figure maintained its downward trend, falling to 57.7% from 64.3% in December, attributable to large base effects. So, while pricing pressures showed some further strengthening, increases across all groups were lower than they were last year and therefore helped the drop in the headline figure. We will likely see further falls in the near term with the presence of large base effects if stability in the Lira continues.

The underlying trend (as measured by the three-month moving average, annualised percentage change, based on seasonally-adjusted series) for goods inflation remained broadly unchanged in comparison to the previous month. However, the services group recorded a significant increase in annual inflation compared to the previous month, contributing to the deterioration in underlying trends of core and headline inflation in January.

PPI inflation recorded another sharp drop to 86.5% year-on-year, the lowest reading since the end of 2021. While the base effects have been the main determinant, we also see support from price drops in oil and utilities. However, the monthly reading of 4.2% hints at an increase in cost-push pressures, also likely contributed by the adjustment in the minimum wage.

Annual inflation (%)

Core = CPI excluding energy, food & drinks, alcoholic beverages, tobacco, gold

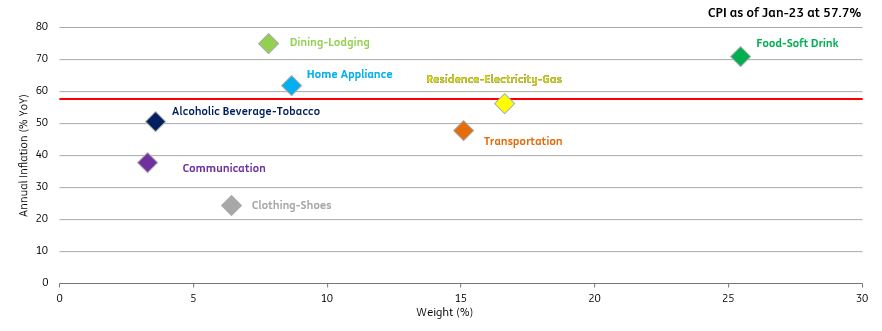

In the breakdown of the main expenditure groups, annual inflation in the heavy-weight food group declined driven by both processed and unprocessed food prices. However, the monthly figure almost doubled the long-term January average, pulling the headline up by 1.68ppt. Pressure in food prices and price adjustments at the start of the year caused a jump in catering prices, making it the second-biggest contributor with 1.00ppt. It is followed by transportation, given price adjustments in transportation services, automobiles and gasoline. However, the annual change in this group further declined to 47.7% from triple digits in November, showing the extent of base effects. With the exception of clothing and shoes, which recorded a price decline, all other groups showed strong increases, confirming the challenges to disinflation despite the Central Bank of Turkey's relatively optimistic forecast for this year of 22.3%. As a result, goods inflation moderated to 55.8% YoY, while annual inflation in services jumped to 62.4% YoY, which is the peak of the current inflation series driven in particular by rent and catering services.

Finally, the Turkish Statistical Institute made its usual revisions to the CPI basket by cutting the weights of transportation, alcoholic beverages and tobacco, communication, education and household equipment and adding housing, health and food. After these changes, the weight of the food group remained the highest at 25.43%, while housing stood at 16.6% followed by transportation at 15.1%, losing its place to housing this year.

Annual inflation in expenditure groups

Overall, annual inflation maintained its downtrend in January as expected, and is likely to decline further until May mainly due to strong base effects, albeit depending on the currency stability. However, given deeply negative real interest rates, further disinflation would be quite challenging, while risks to the outlook this year are on the upside given the significant deterioration in pricing behaviour, higher trend inflation and the still elevated level of cost-push pressures.

In the January Monetary Policy Committee (MPC) meeting, the removal of the forward guidance about “the current level of policy rate being adequate” attracted attention, while the central bank has recently introduced further macro-prudential moves with the objective of permanent “liraisation”. This week, President Erdogan’s statement that "...at the moment, we have an interest rate of 9% and we will lower it further..." will likely shift focus to the February MPC. In this environment, efforts to maintain TRY stability will continue.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more