- Quick take

Rising foreign reserves gives room for a weaker yuan

- 9 July 2018

- FX China

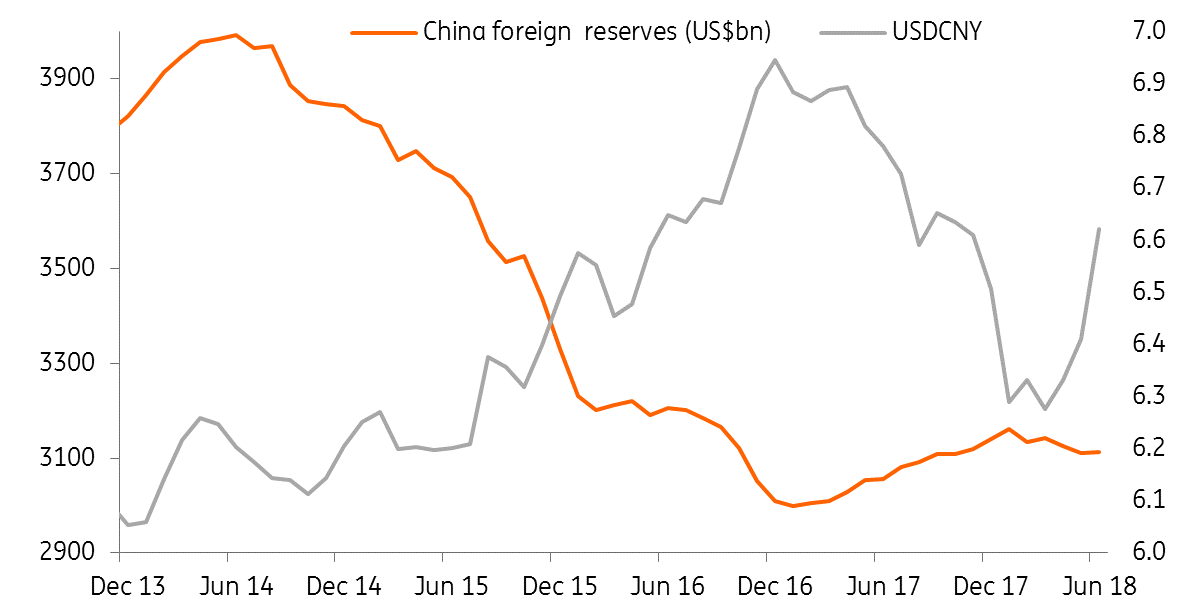

Foreign exchange reserves in China rose $1.51 billion in June from May, stopping the falling trend. A-share's inclusion in the MSCI from 1 June helped, and wider inflow channels give more room for yuan weakening

No depletion of foreign exchange reserves

Inflows have more than offset outflows in June.

On 1 June 2018, A-shares inclusion in the MSCI brought $22 billion capital inflows into China. We also expect a trade surplus of near $25 billion in June.

But as the dollar index rose by 0.5%, the valuation effect on non-USD dollar assets in China's foreign exchange reserves was negative. This was the main reason for the drop in foreign reserves in April and May.

Yuan depreciation of more than 3% in the month should have resulted in some capital outflows.

| +$1.5 billion |

Foreign exchange reservesJune 2018 at $3.1121 trillion |

| Higher than expected | |

Yuan can weaken further as persistent net outflows is no longer a concern

In the future, we expect inflow channels to continue to widen further. This is the main reason that we have revised our yuan forecast to 7.0.

Inflows include investments in financial assets onshore (more A-share inclusion in the MSCI on 3 September 2018), and the opening up of business markets for foreign investors interested in financial sectors and transport manufacturing (the opening up of different sectors has a different timeframe from now to 2020).

If foreign exchange reserves fall only slowly or even rise due to inflows when the yuan weakens, then the concern about net capital outflows that would deplete fx reserves shouldn't be a concern.

We believe that a weaker yuan in the middle of a trade war between China and US is reasonable because a currency would depreciate to adjust for slower export growth. It would be strange if the yuan appreciates against the dollar when the trade war continues.

We, therefore, confirm our yuan forecast at 7.0 by the end of 2018.

Foreign reserves rose in June even though the yuan weakened

Trade war's impact on asset market

The trade war started officially at the beginning of July, and we expect another $16 billion of goods will be subject to a 25% tariff from the US and then from China as soon as before August.

All of this should have been priced in in asset markets.

But the extra $200 billion worth of goods subject to a 10% tariff from the US after China retaliates is still to be fully priced in. When the $200 billion tariff becomes more imminent then the market should be more volatile than the current environment.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 10 July 2018

- This bundle contains 3 Articles